Related Blogs

May 30, 2018 | Michael Reilly

Your 401(k), 403(b), or 457 plan might be the biggest, most important asset you have. The one that could have the greatest impact on your family’s future wealth.

It’s an asset that has the highest growth potential. That’s because these accounts grow on a tax deferred basis, so you’re not paying taxes on the growth of the account each year – leaving more money available to grow for years to come…

But, thanks to the passage of the new DOL Fiduciary Rule, investors are more on their own than ever before!

These new rules were designed to protect investors from brokers charging high fees and commissions by requiring brokers and financial advisors to adhere to a strict “Fiduciary Standard”.

In response, many brokers no longer want to get involved in giving clients advice about their retirement plan assets. And in some cases, brokers are even prohibited from doing so by their brokerage firm.

Of course, RWM is a Registered Investment Advisor. This means we’re already a Fiduciary.

So, we’ve always been held to the strict rules the DOL is now forcing brokers to adhere to if they want to manage your retirement assets.

If you want to make sure your retirement assets are being properly handled, you can click here now to schedule a consultation. These are available for free to qualified investors.

(For more on the DOL rule click Here)

The bottom line is this – investors have limited choices… Go it alone and hope for the best, or find someone who can show them how to invest their family’s most important asset.

Most investors have no idea how easy it can be to add tens of thousands of dollars to their retirement savings with just four simple moves a year.

That’s because, when investors go it alone, they often get so frustrated or intimidated by the websites they’re expected to navigate (just to see their accounts), that they don’t ever get a chance to follow the strategy I’m referring to.

Instead, they throw up their hands out of frustration or fear of making a mistake, and leave their retirement accounts to languish in mediocrity for years.

You see, most people are either too busy or can’t be bothered to go onto the website and figure out how to manage this incredibly important asset.

And with the new broker requirements, investors can’t count on most advisors for help.

Does this describe you?

What you might not realize, is that you could be leaving a huge amount of money on the table. This might be because trying to figure out which fund choices within your retirement plan are best, isn’t your idea of a good time.

I’ve heard it a hundred times, “I know I should look at my 401k. But I don’t really know what I’m doing and we don’t get much help.”

Here’s the reality…

1. Most individual investors usually have a career that doesn’t involve financial market analysis. Therefore, they don’t feel confident deciding how to position themselves without help.

2. Many investment professionals aren’t great at managing money and don’t want to be bothered with these types of accounts. So they make up a legit-sounding story on why they don’t get involved.

3. It’s too easy to just leave it alone and focus on something… anything else.

Some of the safest, strongest and best performing investment strategies require investors to get involved – to adapt and rebalance investments based on market conditions.

But the headache of navigating a website that you rarely visit and aren’t comfortable with, to make regular changes (rebalancing) to your account, keeps most investors from doing the work.

The end result is that one of the easiest and most impactful strategies available to investors, is rarely used.

Instead, investors are missing the chance to protect and grow their most important money.

By “important money”, I mean retirement money.

This is the money that you’ll need for medical expenses. It’s the money that will help you to live comfortably.

It’s the money that may send you on vacations, let you see your family, get you the home you want, or just get you out to the nicer restaurants.

Some folks reading this are already in their 70’s – or close to it, but it’s never too late to go for better, risk adjusted returns. Re balancing regularly can significantly reduce your risk of decline.

And if you don’t have the patience to do it yourself, we’d be more than happy to do it for you.

Do you want to be the person who looks back and says, “Had I only paid just a little bit of attention to this account, it could be several times bigger than it is today”?

Two Potential Solutions

The first way to fix this is to take charge and get more involved. Find and invest in the resources that may give you the best chance for market beating returns in your retirement plan accounts.

All you’d need to do is take the time to learn a few of the investment strategies available to you, including the simple rebalancing strategy I mentioned already that only requires you to look at your account four times a year.

It’s not that hard. But most people just can’t do it.

Because it requires time. And let’s face it, sometimes there just aren’t enough hours in the day.

You need discipline – and managing one’s emotions can be a full-time job, especially when financial markets are in chaos.

And it takes more than just a basic understanding of the markets. Some people enjoy studying market behavior, while others don’t.

I refer to this as the three T’s of investing: Time, Temperament, and Talent.

Do you have time to manage the investments?

Do you have the temperament to keep your emotions in check when markets get scary?

And do you have the talent, the resources and know-how to manage what may be the biggest, most important asset you own?

So, maybe you have the time and the talent, but understand yourself enough to know you don’t have the right temperament to manage money through a variety of market conditions.

And that’s okay, I’ve been investing money professionally for nearly 30 years and I can tell you… sometimes, it’s tough even for guys like me.

But if you can’t bring all three T’s together, you’re not helping yourself.

It’s going to feel like you’re driving over endless potholes.. Everything is going along smooth, until Kerplunk!… you drive over a pothole. Then it’s smooth again .. and Kerplunk!… you hit the next one… and the one after that…

You have a choice.

If you qualify, Rowe Wealth Management can rebalance your retirement accounts for you.

We have very sophisticated tools that can analyze all of the funds available to you (the mutual funds or ETFs listed in your qualified plans), 401(k), 403 (b), or 457.

We use these algorithms to identify the strongest funds available within your retirement plan, ranking the funds from strongest to weakest.

The algorithm creates scores for the funds based on chart patterns, Moving Averages, Momentum, and rankings for the funds versus several important Market and Peer Groups over several time periods.

The Score uses proprietary weightings. These weightings are designed to score a fund based on certain trends (this makes up one third of the fund score) while Relative Strength scores represent the remaining two thirds..

The end result is a matrix of all the available funds within your retirement account, ranked according to their relative strength when compared to each other.

Selecting from only the funds on the very top of the matrix list may give investors the best chance to outperform current markets.

Just How Much Could You Stand To Gain?

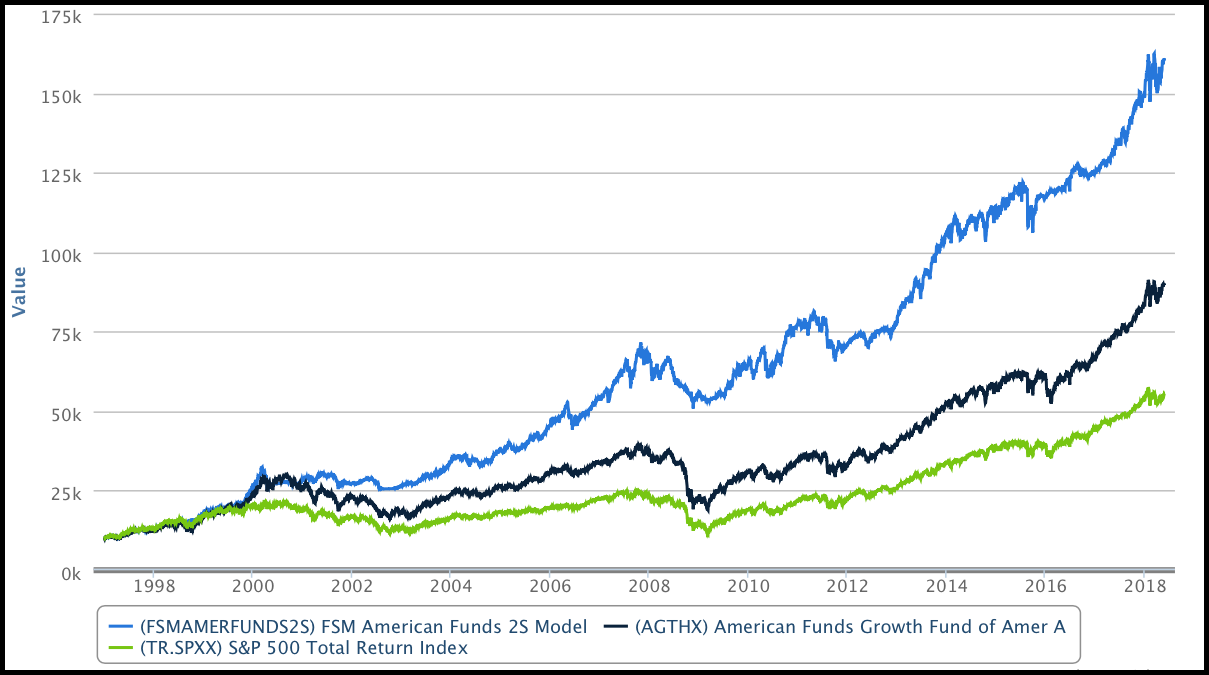

To see just how significant this difference can be, take a look at this model by Nasdaq that uses fund score rankings. It ranks mutual funds managed by The American Funds Group.

The model stays invested in the top two ranked funds, rebalancing just once-per-quarter, based on matrix results. Sometimes growth funds are on top, other times it may be Income funds or even money market funds.

Below is a partial list of the 26 American Funds included in the matrix.

And below are the two American Funds Mutual Funds with the highest current scores.

These are the two funds that comprise the model during the second quarter 2018.

We’ll have to wait until the end of the quarter (June 30, 2018) to see if these two funds remain or one or both are replaced by another of the available 26 funds.

Check out the line chart below, the results of following this easy to implement strategy can be staggering….

(Note: While RWM offers similar models, this model is not a RWM model. The returns do not include dividends, taxes, fees, or other trading costs.)

Following the line chart above, the hypothetical returns from an investment into the S&P 500 Total Return Index (green line) on December 31,1996 and held thru May 25, 2018 would have been 450.29% – or $54,906 from a $10,000 investment.

The hypothetical returns from the same investment in a single fund – in this case the Growth Fund of America (black line), a mutual fund that has been around since 1973, are significantly higer, at 797.32%. A similar $10,000 investment would increase in value to $89,731.

Now here’s where things get really interesting…

The hypothetical returns from the Nasdaq /American Funds model described above, the one that re-allocates on just 4 specific dates throughout the year, nearly tripled the value (blue line) of the investment in the S&P 500 Total Return Index – gaining 1505.43%. A $10,000 investment in a similar model over that period of time could hypothetically increase to $160,542.

That means the model outperformed both the Growth Mutual Fund and The S&P 500 T/R Index by 708.11% and 1055.13% respectively.

Those are not typos. The model nearly tripled the return following the Index and doubled the very successful Growth Fund of America.

See table below for annual and total returns of the Nasdaq model, the S&P 500 Total Return Index, and The Growth Fund of America.

What’s really amazing is that, in our example above, the model only required rebalancing less than 4 times a year (3.43) over the last 21.5 years.

If you have any questions or you’d like to talk more about how we may be able to help you strengthen your 401K, please don’t hesitate to schedule a consultation.

A consultation carries no commitment, if you’d simply like to ask a few questions we’d still love to talk with you. Click here now to pick an appointment time.

Tags

Get Our FREE Guide

How to Find the Best Advisor for You

Learn how to choose an advisor that has your best interests in mind. You'll also be subscribed to ADAPT, Avalon’s free newsletter with updates on our strongest performing investment models and market insights from a responsible money management perspective.