Related Blogs

March 10, 2022 | Avalon Team

It’s no secret that passive index funds and ETFs have been gathering the bulk of asset flows for several years. In 2021 alone, passive funds assets increased by 35.9% and reached $20.87 trillion (as of June 30). Blackrock, Vanguard, and State Street hold the bulk of these assets.

Passive funds are, by definition, designed to mimic a selected market – the stocks in the S&P 500 for example – and always hold every stock within that market.

It’s important to realize that passive investing is not just a retail phenomenon, but also very embedded in institutional investors. Endowments, for example, often hold very large positions in passive investments.

According to Bloomberg, passive’s share of U.S. fund assets has grown about 2.3% a year.

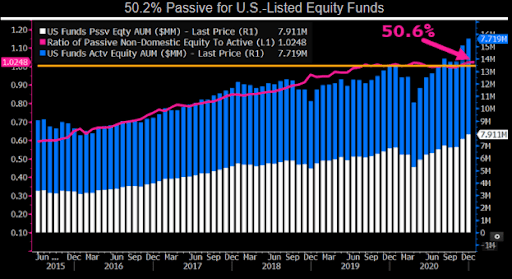

Among U.S. equity funds, passive vehicles hold 50.2% of U.S. publicly traded equity fund assets.

There are several forces driving the rise in popularity of passive investment…

One has been regulatory events that have reinforced the trend, like the Pension Protection Act of 2006. It encourages participation in products like 401(k)s by switching the framework from an “opt-in” to an “opt-out” decision for new employees.

The Act also made a change in the qualified default investment alternative.

Prior to the Act, the default investment choice was a money market mutual fund. After the Act, it became the responsibility of the human resource manager to select the default choice.

After further refinement of the Act in 2012, Target Date funds became the default investment choice, and are by design, passive.

As a result, Target Date funds have exploded in popularity and now gather 85 cents of every $1.00 invested in 401(k)s.

Now, all of this combined has had a dramatic impact on the flow of funds into the market because active managers who attempt to define the value of a stock, have experienced an outflow of funds, while passive investment products have experienced a steady inflow.

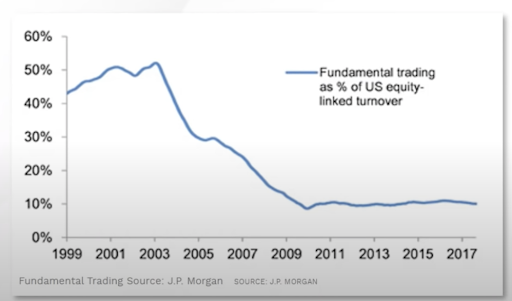

As a result, only about 10% of activity has a fundamental signal attached to it (by fundamental signal, I am referring to an earnings report, a manager deciding a stock is “cheap”, etc.).

This means that almost all of the money coming into the market has become systematic.

The impacts of this are profound and important for investors to understand. Here’s why…

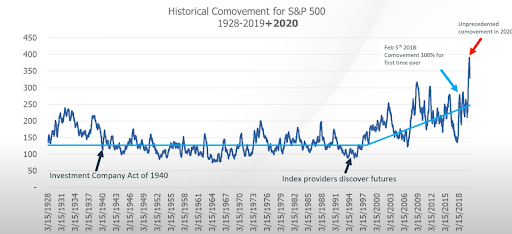

Increased Correlation Between Securities

It has become more difficult to decrease risk by diversification. Correlations are now at all-time highs because all securities are being bought and sold together, based purely on fund flows.

Increase In Valuations, Regardless of Fundamentals

It’s important to realize that an index fund manager has only one job which is to put every dollar to work in the underlying index. Never is asked, “Is this a good time to buy?” or “Is is this a reasonable valuation to pay?”

An active manager would typically have a propensity to buy at low valuations and to sell at high valuations. This results in some cyclicality to the P/E ratio.

However, a passive manager has a 100% propensity to buy if he has been given money to invest, regardless of valuations. The result of this, as passive funds have gained dominance, is that valuations have increased.

Increased Concentration as the Largest Companies Become Even Larger

The leading stocks represent the greatest concentration in history because the largest companies are being pushed up at an increasing rate.

A trillion-dollar company that goes up 10% will increase by $100B, whereas a company with a $10B market cap will only increase by $1B, which means the largest companies represent an ever-increasing percentage of the underlying index.

In fact, this resulted in the SEC granting index funds an exemptive relief in 2018 when funds no longer meet the diversified status of the 1940s Mutual Fund Act.

And the effect of this is not felt in just stock funds, but also in bond funds.

Passive bond fund flows reward the bonds that have increased the most in price. The example below shows a bond with a guaranteed negative yield that is the top holding.

How does this happen?

At one time the bond was a positive yielding bond that has run up so much in price that it now has a negative yield. But that doesn’t stop the index funds from buying it. Remember, they have to.

The Hidden Trap Door of Index Funds

The final impact of mention is perhaps the most important for investors because of reduced market elasticity and the risks of extraordinary price movements.

Because there are fewer active investors in the market, and because more shares are in the hands of passive index funds, this effectively removes some liquidity around events.

When a company reports earnings, it has no impact on the passive index fund because, by definition, it must own the stock. The fund manager could really care less whether the earnings report was good or bad.

But for all of the other investors who want to act on the news, they are doing so amongst themselves, which represents a smaller pool of shares. As a result, stocks are displaying 4X the volatility during earnings events than they were 20 years ago.

So despite the tremendous fund flows into the market in recent years, because so many shares are held passively, it actually has decreased the liquidity, not increased it.

This also can have an impact on redemptions.

Index fund managers hate cash as any amount will cause the fund to display variance from the underlying index. As a result, fund groups, such as the Vanguard, actually do not keep cash on hand in the fund, but rather use an outside letter of credit to meet redemptions.

So a fund manager if given a redemption request must sell shares to meet the redemption request. They have no cash cushion and they are obliged to sell. In the normal course of business, buying demand and selling demand can offset each other.

But what happens when there is a significant shift to selling? Could this reduced market elasticity result in greater price movements to the downside?

The greatest concern is that the retirement savings of Americans have been placed on autopilot through Target Date funds, with no consideration for market valuations and shifts in economic regimes.

The highest stock market valuations in all of recorded history and the lowest interest rates in all of recorded history both precede periods of instability.

While passive funds have made it easy for investors to access the markets, they fail to protect investors from the very risks that they have created.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.