Related Blogs

February 3, 2022 | Avalon Team

Welcome back to another week of “The Death of 60/40.”

For the last two weeks, I’ve described how stock valuations play a role in defining future expected returns – and how today’s stock market valuations portend a forthcoming era of low returns.

“But isn’t the reason we allocate 40% to bonds, is to help offset weakness in stocks?” a smart investor might ask…

Yes, but…

Bonds have so little to give for such a big role.

I think an analogy is in order…

The 1964 children’s book The Giving Tree by Shel Silverstein, tells the story of a boy and an apple tree. The tree lives up to its name by providing the boy with resources to fulfill the boy’s desires.

The tree provides apples which he sells for money, and then the branches are used to build a house, and later, the trunk is used to construct a boat. At the end of the story, the tree is just a stump and can provide only a place to sit quietly.

Like the Giving Tree, bonds have offered much to investors during the past decades, but just like the story at the end, have very little left to give to investors.

As I did before with stocks, I will first show you the historical returns of bonds and the factors that drove returns. Then, I will compare to present-day factors as I assess future expectations.

Historical Returns of Bonds

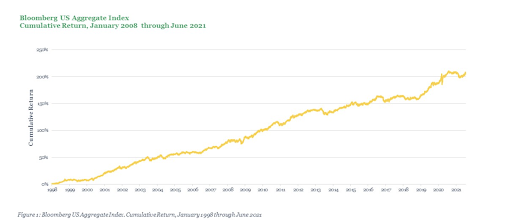

The Bloomberg Barclays U.S. Aggregate Bond Index (“AGG”) measures the performance of investment-grade bonds in the United States.

The index includes U.S Treasuries, government-related issues, corporate bonds, agency mortgage-backed pass-throughs, consumer asset-backed securities, and commercial mortgage-backed securities.

Since 1980, the average annual gain for AGG is 7.67%. The highest return was in 1982 at 32.65%. The lowest return was -2.92% in 1994.

During this period which included the dot.com bubble and crash, the financial crisis in 2008, and more recently, the Covid pandemic, US AGG has been a dependable ballast in portfolios.

Throughout the experience of most fixed-income investors in the market today, bonds have been a source of return, resilience, and consistency – backstopping retirement savings portfolios without much thought or worry.

But like the Giving Tree, bonds are running out of things to give investors.

Bonds have been long-trusted to deliver two things: an income stream that is determined by the coupon (issued yield) and price appreciation.

The latter, price appreciation is inversely influenced by prevailing rates. For example, if a bond is issued at 3% but current rates are only 2%, then the 3% income stream is a “premium” to current rates. As a result, the 3% bond is priced at a “premium,” and if an investor went to sell the bond, could potentially capture a gain.

It works oppositely if interest rates rise. A bond issued at a lower yield than prevailing rates will be “discounted” so that the current yield is close to current yields. Thus, if an investor went to sell the bond, they could experience a loss.

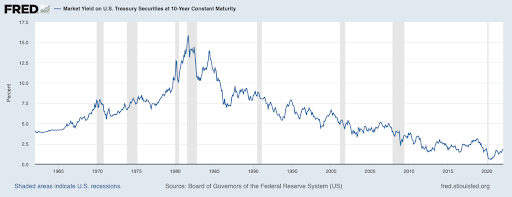

Ever since 1980, interest rates have been falling. This has created an ideal environment that has richly rewarded bondholders.

As interest rates have trended down in secular decline since the mid-1980s, the great fixed-income bull run has increasingly relied on price appreciation to generate its total return (to recall the key relationship, bond prices rise as interest rates fall).

Now, there are very few things that I can guarantee when it comes to investing, but one thing I know for sure – it is mathematically impossible for bonds to return what they have over the past few decades.

Simple bond math suggests that absent a significant change in policy, there is not much left for fixed-income markets to provide. The four-decade trend in cutting yields has likely come to an end, and even if rates were to drop from the present 1.70% to 0%, that only leaves about 3% price appreciation left in the AGG Index.

It is more likely that interest rates will need to increase, not decrease.

And the timing could not be worse.

We come to realize that our Giving Tree has been cut to a stump. Current-day coupons are minuscule. The slightest uptick in interest rates will send mountains of near zero-coupon rate bonds sinking like a ship.

And the catalyst for rising rates are many. Inflation is running high and the Federal Reserve has recently been forced to play the hand of the “enforcer” by adopting a path of monetary tightening.

The consensus is that the Fed will be raising rates. The only question is by how much and by how many times.

Bloomberg’s chief U.S. economist Anna Wong says, “Our baseline is for the Fed to hike five times, each 25 basis points, this year, and balance-sheet runoff to begin in July. Our in-house rule for the Fed’s reaction function flags an upside risk for a 50 basis-point hike in March followed by five 25 basis-point hikes in the rest of the year.”

Consider that the 10-Year Constant Maturity Rate, currently yielding 1.81% is negative when considering the inflation rate. This alone suggests that interest rates should be higher.

On top of inflation, the National Debt has just exceeded $30 Trillion for the first time. This implies a continued reliance upon debt issuance. But to who and at what costs?

Again, the simple facts are that the deflationary forces of the best decades and the continual decline of interest rates are fading in our review mirror.

The macro factors we face today look nothing like they did 40 years ago.

For investors to extrapolate the past results of bond investing into the future will surely result in shock and disappointment.

The Giving Tree has nothing left to give.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.