Related Blogs

February 11, 2022 | Avalon Team

Welcome to the last of the series “The Death of 60/40.”

I have written in this series on how the 60/40 portfolio was justifiably a staple in investor portfolios based upon past performance.

By any measure of financial history, the last four decades were one of the most significant periods of asset growth price ever. A remarkable 91% of the price appreciation for the classic 60/40 over the last 90 years comes from just 22 years between 1984 and 2007.

But, I have also written on how and why the future has a very low probability of looking like anything in the past.

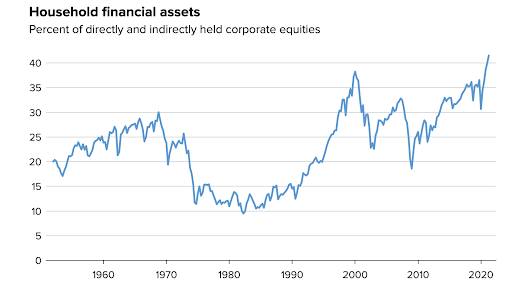

Over four decades ago, the Federal Reserve began easing interest rates from a high of 14% after battling the stagflation of the 1970s.

Stocks had been pummelled to their lowest valuations in modern market history and offered dividend yields near 6% and single-digit P/Es.

Aging baby boomers with an eye on retirement began investing at an ever-increasing rate in the stock market, aided in part by the popularity of mutual funds.

The result was more than tripling in the amount of household financial assets held in equities.

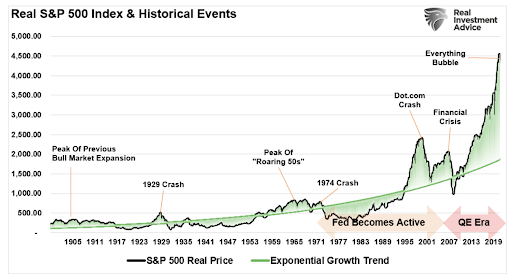

By 2000, stocks had become richly valued and had reached historically high extreme valuations. At the onset of the Dot.com crash, stocks had been pushed well beyond their exponential growth trend.

Today, investors are once again staring at historically high valuations.

Further, over the past 12 years, fueled by massive fiscal and monetary intervention, extremely low borrowing costs, and corporate buybacks, stocks are stretched so high above the exponential growth trend, that it now dwarfs even the dot.com era.

One crucial point is that large deviations above the exponential growth trend historically “mean revert.” Such reversions previously led to very long periods of no returns.

Research conducted by money management firm GMO shows that ALL 2-sigma equity bubbles in developed equity markets have burst – all the way back to trend. The U.S. reached the 2-sigma level in the summer of 2020.

The U.S. reached 3-sigma in late 2021, suggesting a longer-lasting and deeper correction is on the horizon…

With the potential for zero to negative returns for stocks probable, investors cannot rely on bonds to provide the cushion that they have in the past.

The period of disinflation and falling interest rates of the past 40 years appears over.

Supply chain constraints and labor shortages coupled with high demand have resulted in a surge in the consumer price index and general inflation.

Interest rates have started to rise right at a point when the average interest rate on recently issued debt is minuscule.

Given the inverse relationship between interest rates and bond prices, bond prices are near certain to drop in price.

The irony for investors is that bonds, the supposed risk mitigator within asset allocation plans, may now pose a similar risk as stocks.

In short, bonds have little left to give and are unlikely to provide the cushion and sanctuary of safety that they have done historically.

For investors, the dual threat of falling stock and bond prices provides little chance that financial goals can be achieved using traditional passive allocation strategies.

The 100-Year Portfolio

While some investors may view this grim reality with despair, it is important to understand that what I outline is nothing new.

The entire history of money is defined by periods of spectacular growth fueled by virtuous cycles of rising asset prices and value creation to only be followed by periods of secular change that challenge, and sometimes destroy, the growth cycle.

This is a natural cycle. It is should not be feared, it cannot be stopped, but it can be prepared for.

While the classic 60/40 is well-intentioned and performs excellently during periods of growth, it is not well-suited for secular change.

The once-in-a-lifetime boom in risk assets over the past forty years has caused investors to over-allocate to assets that profit from secular growth (stocks, real estate, credit) and under-allocated to non-correlated and active alternatives that profit from change (gold, long volatility, commodity trend, and global macro).

The 60/40 Portfolio suffers from recency bias and is highly reliant on assumptions derived from a once-in-a-century bull market in stocks and bonds.

Rather, investors should step back and look at what kind of portfolio has worked well over a longer time span that includes periods of both expansion and contraction.

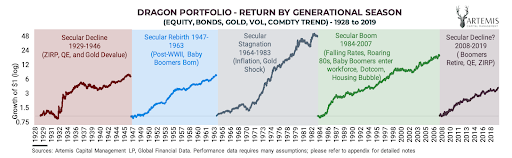

In a research paper, “The Allegory of the Hawk and Serpent. How to Grow and Protect Your Wealth for 100 Years” published by Artemis Capital Management, the goal was to discover a century-long portfolio that could provide both capital appreciation and protection through all market environments: inflation to deflation, growth to crash.

The innovative portfolio that resulted from the research was a portfolio that diversifies risk based on the market regime (e.g. growth, deflation, inflation) rather than by asset class.

While the concept is easy to understand, it is a radical departure from traditional portfolios that allocate by investment category such as the 60/40.

I stress again that traditional portfolios like the 60/40 suffer from a dangerous overreliance on a stable relationship between stocks and bonds and their performance.

By balancing assets that perform well in the growth cycle (equity, real estate), with alternatives such as long volatility and commodity trend, the portfolio has shown the ability to perform consistently through both growth regimes and periods of decline.

Adaptive Allocation

For investments held within traditional asset classes such as stocks and bonds, I propose that an active, adaptive approach will be required for long-term success.

I will say this again as it bears repeating: Passive approaches based on current market overvaluations have little to negative return expectancy in the coming years.

To be successful, investors will need to think outside the box and be willing to approach the markets with new strategies.

Rotation strategies that can quickly adapt to the changing market conditions and that can seek out the best performing asset classes while avoiding the worse are one such example.

And sometimes, the best-performing asset class will be cash.

The primary goal of investors should be to protect their capital from significant and potentially non-recoverable market losses.

Rather than making the 60/40 Portfolio static and owning the entire stock market and bond market, one method can be to approach each part of the 60/40 with a more granular approach.

For instance, stocks can be subdivided into international (non-U.S.), U.S. large-cap, U.S. small-cap, and so on.

Bonds can be subdivided as well into categories such as U.S. government, (short, intermediate, and long-term duration), corporate, and high yield.

Using this kind of approach can amplify the positive performance of factors that tend to rotate depending on broader macro influences and take advantage of relative valuation differences.

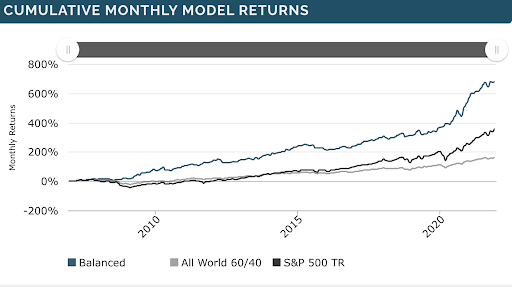

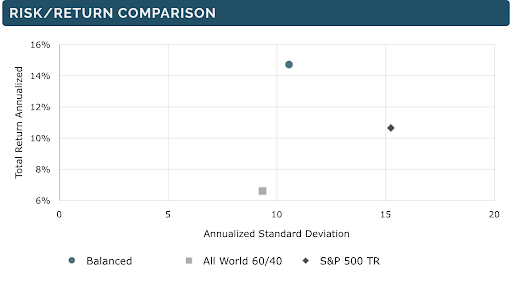

In recent years, such an approach has outperformed the classic 60/40 by a wide margin, and with significantly less risk.

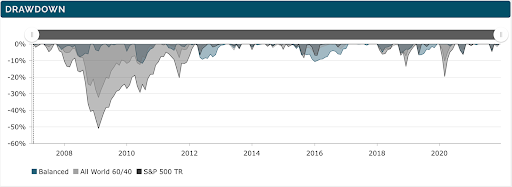

There is no more important metric than the maximum drawdown of a given strategy. The ability of a strategy to contain risk allows for consistent compounding.

With the ability to rotate the cash and other defensive assets in times of market turmoil, this new approach to the 60/40 does a much better job of managing downside risk.

Where the S&P 500 has incurred a loss of over 50%, this strategy has a max downside loss of only 11.68%…

In other words, the adaptive strategy has provided over 40% more return with 80% less risk!

The key is having a flexible approach versus a static approach.

The markets are not static so why should your portfolio be?

I believe that investors are entering a new regime and with it, will come new challenges.

Investors who continue to invest using strategies that have worked well during the last four decades will be disappointed, to say the least.

I hope I have inspired investors to think critically and to take preemptive action to make sure that they’re able to stay on course to reach their financial goals.

While change can be sometimes difficult to make, it can also bring new opportunities…

In the words of the Greek philosopher Heraclitus, “Nothing endures but change.”

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.