Related Blogs

March 24, 2022 | Avalon Team

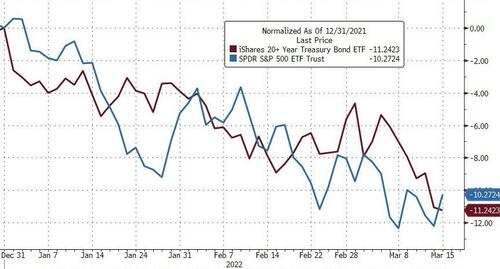

In my recent series, “The Death of 60/40,” I cautioned investors that traditional asset-allocation strategies that have worked in recent years would begin to fail.

We’re not even three months into the year so far and the classic 60/40 is down more than 10%, on pace for the worst drubbing since the financial crisis of 2008.

It also marks the first time on record that both bonds and stocks are down 10% together in a single quarter.

In fact, for a 50:50 allocation of stocks/bonds, it has been the worst quarter ever.

Wondering what gives?

The short answer: regime change.

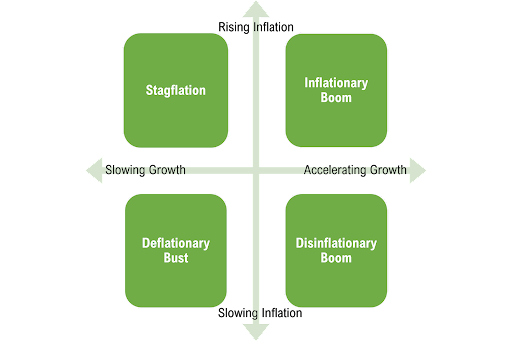

Stagflation is back.

Assets are being hammered by the double whammy of the risk of a stagnant economic expansion and fears of out-of-control ‘non-transitory’ inflation (a combination that could cause poor returns, or even losses, to extend for some time to come).

And this spells trouble given the prospect of poor returns and less diversification potential from bonds.

Andrew Patterson, a senior economist at Vanguard Group Inc., said “markets are verging on a period of low gains for the 60/40 portfolio.”

And Jean Boivin, head of the BlackRock Investment Institute, has this to say, “Investors will have to live with higher inflation and that will challenge the role of government bonds in a portfolio.”

Now more than ever, it’s important that investors examine the role that bonds play in their portfolios and possibly seek alternatives.

Every investment within a portfolio represents a future stream of returns, which is the net sum of cash returned, plus or minus any gains.

Given that nominal bond yields are low and that rising interest rates and inflation can cause bond prices to fall, we can conclude that the future return steam for bonds is currently negative.

The goal then is to replace the bond allocation, or some portion thereof, with an investment that provides an expected positive return stream.

Let’s examine the case for managed futures versus a range of other liquid assets and strategies including investment grade, high yield, emerging market debt, gold, commodities, and hedge funds.

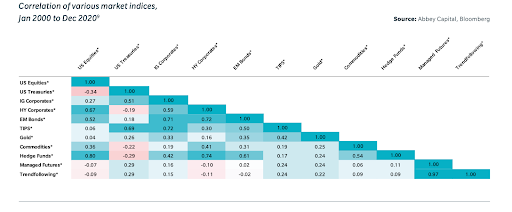

In considering the alternatives to government bonds, investors should assess not only their risk and return characteristics but also their correlation profile. Investors should also analyze which assets and strategies can potentially generate returns in periods when equities suffer significant drawdowns.

Managed futures are considered an alternative investment and are often used by funds and institutional investors to provide both portfolio and market diversification. Managed futures provide this portfolio diversification by offering exposure to asset classes to help mitigate portfolio risk in a way that is not possible in direct equity investments like stocks and bonds.

Looking at cross-asset correlations, we can see that historically, after government bonds, managed futures have exhibited the most attractive correlation profile with equities from the perspective of diversifying equity risk.

The concern is that the correlation is changing with respect to bonds and equities as inflation emerges. We are seeing this already.

Managed futures strategies, like trend-following, generate returns when there are sustained trends in markets. As managers can be long or short and typically trade a wide variety of asset classes, it seems reasonable to expect that returns will continue to be uncorrelated with a long equity portfolio over the long term.

So, with managed futures demonstrating a negative correlation to equities, they pass our first test of diversifying a portfolio.

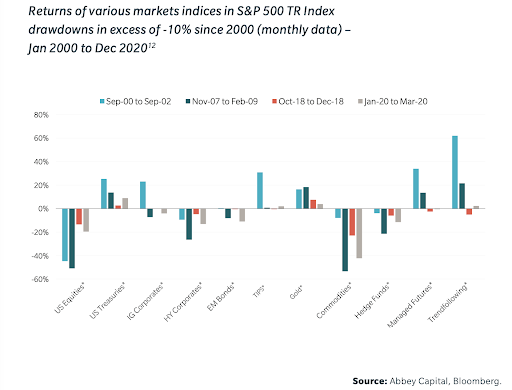

A second consideration is to study which assets and strategies have the ability to deliver positive performance during crisis periods for equities. That is after all, why bonds have been traditionally allocated to in the classic 60/40.

In looking at returns of various market indices when the S&P 500 fell by at least 10%, we can see that managed futures have had not only the lowest drawdowns but have also delivered a positive performance in those same periods.

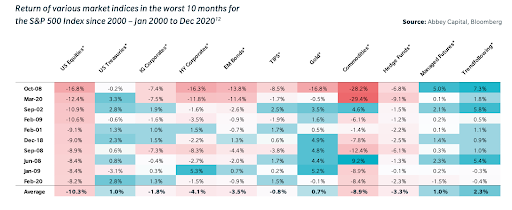

Looking more closely at monthly data among the worst 10 months since 2000, we can see how managed futures and trend following have consistently delivered positive returns during these periods of equity stress.

So it seems that managed futures also meet our second criteria of providing positive returns during periods of equity weakness.

It’s important to keep in mind that historically, managed futures returns have been achieved in a period of overall low inflation.

It’s quite reasonable to expect that if we are to move into a period of sustained higher inflation, then product inputs like metals, energy, and agricultural commodities will experience greater price trends, and thus the ability to potentially increase return attributes for the asset class.

Traditional portfolio allocations are already beginning to demonstrate the stress from a less accommodative FED, economic instability, and the increasing likelihood of stagflation.

When considering alternatives to government bonds, investors need to assess both risks and return characteristics as well as correlation and the potential to generate returns in periods when equities suffer significant drawdowns.

I believe the low negative correlation between managed futures and equities along with the differentiated return profile relative to other asset classes and the ability to generate positive returns during periods of crisis, make managed futures a compelling alternative for investors to consider.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.