Related Blogs

February 22, 2023 | Avalon Team

Despite the recent rally from the 4th quarter lows, the markets are still significantly down from their peaks.

And while the tech rally has been impressive, the run might be starting to fizzle out. It’s possible that there still may be more declines ahead.

Interest rates, after a brief pause, are back on the rise, likely because there’s a growing acquiescence that the Fed may leave rates higher for longer in order to keep inflation in check.

Yes, inflation is coming down. The reported 6.4% adjusted CPI print is still way ahead of the Fed’s target of 2.5%.

But investors need to be cautious with what they wish for…

A decline in CPI may also bring with it a decline in economic activity.

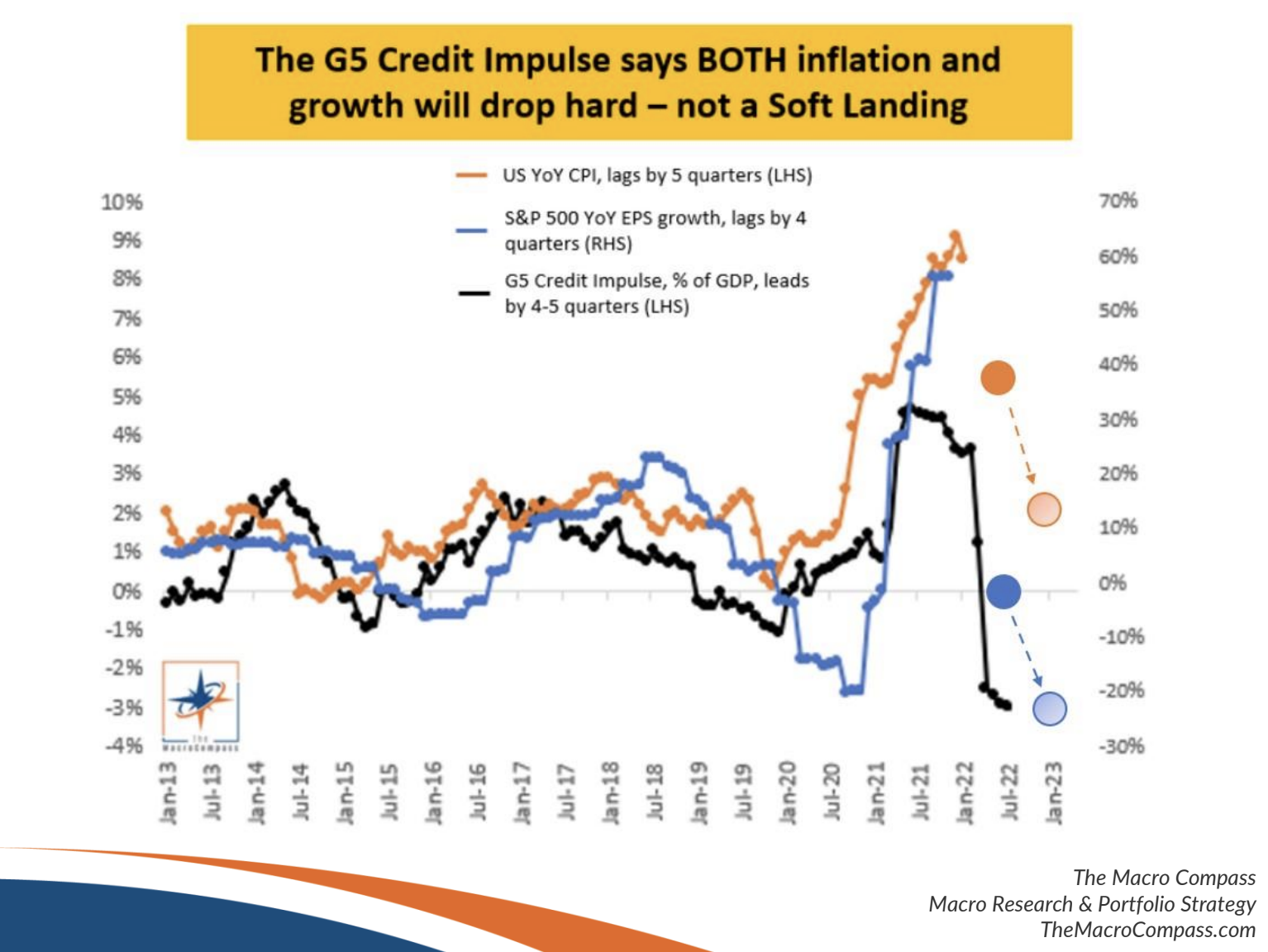

Global Credit Impulse leads economic activity by six months and there is nothing “soft” that it is projecting.

Like clockwork, the rapid decline in credit creation in early 2022 has led to a material deterioration in EPS growth in early 2023 – we’re fast approaching negative YoY earnings growth as we speak.

What’s ahead? By Q2-Q3 2023, we should be looking at -20% YoY earnings growth.

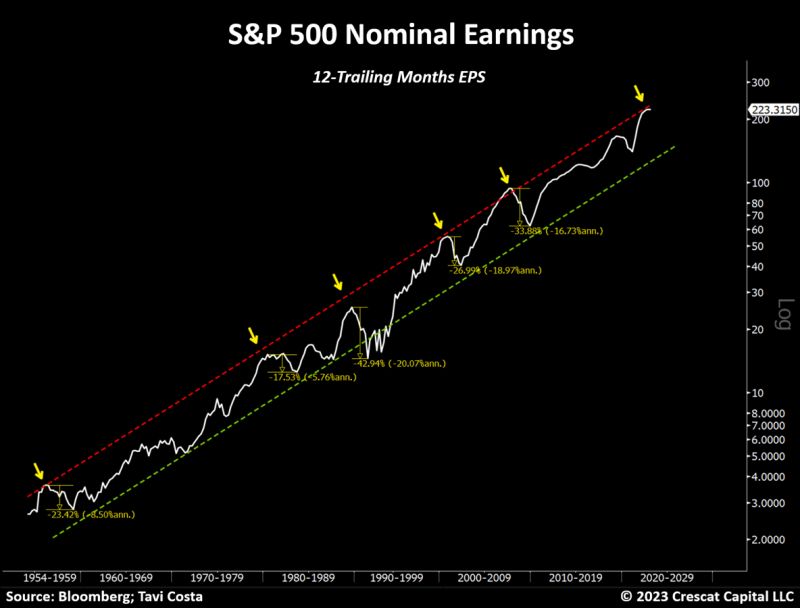

This is just as profits have reached the upper band of a 70-year upward trend in corporate earnings. Every time this level has been reached in the past, an earnings recession followed.

Concurrently, the spread between the S&P 500 earnings yield and the 10-Year Treasury yield has fallen to lows not seen since 2010.

As the spread falls, it decreases the attractiveness of equities and increases the appeal of holding Treasuries on a risk-adjusted basis.

If this spread was to turn negative, it would imply that risk-free assets would be generating superior return than riskier equities.

Remember too that any decline in earnings will also reduce the earnings yield, so treasury yields will need to fall faster than earnings in order to prevent this important ratio to drop further.

Couple that with U.S. 2-Year yields are nearly 3% above the S&P 500 dividend yield.

This is the most attractive short-end Treasuries have been relative to dividends in over a decade!

So for the next 12 months, the economy is likely to show evidence of signs of a nominal growth slowdown that involves earnings, unemployment, and inflation. At the same time, the Fed is promising to keep policy very tight.

It’s going to be interesting…

Which leads us to the question, “What can an investor do?”

Be Cautious With These Hedges

2022 provided investors with some invaluable lessons.

For investors seeking to hedge their portfolios, alternative asset classes offered mixed success.

Gold has generally disappointed, not living up to its billing as either an inflation or risk-off hedge.

Avoid These ETFs

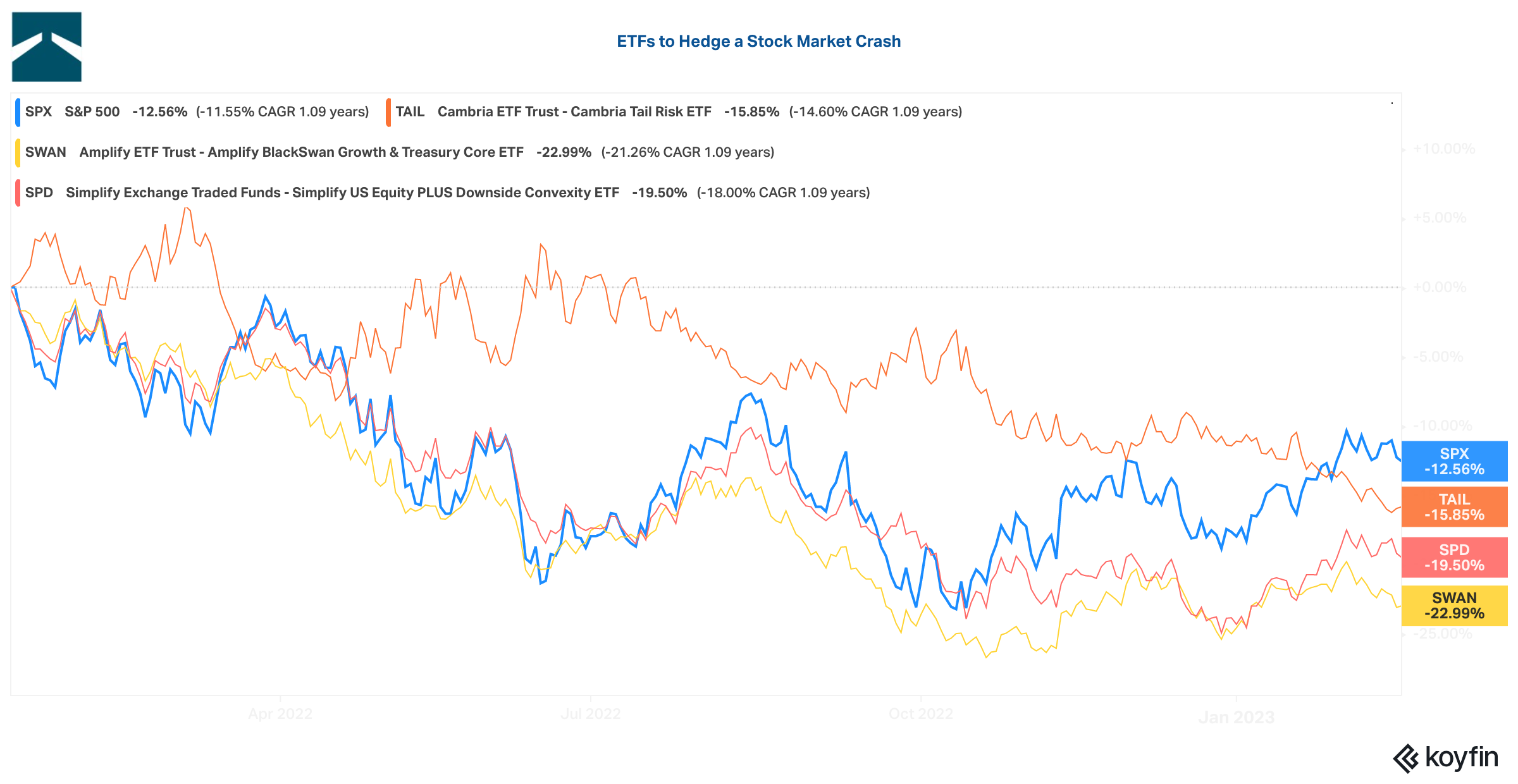

Among the biggest disappointments were specialty ETFs whose purpose is to hedge the market. The graph below shows three such ETFs that have actually performed worse than the index itself.

To understand why these have not worked, it is important to understand the structure of each.

- TAIL (Cambria Tail Risk ETF) allocates a portion of its capital – in this case, about 20% – to a ladder of out-of-the-money (OTM) puts on the S&P 500. The remaining 80% of the ETF is allocated toward U.S. Treasuries and Treasury Inflation-Protected Securities. The idea is that during a “crash,” the value of the puts will soar while the Treasuries remain stable or appreciate as investors rush to safety. The problem in 2022 was that the market decline was more of a constant bleed rather than a “crash” and treasuries were far from safe, losing as much if not more than stocks.

- SPD (Simplify U.S. Equity Plus Downside Convexity) comprises just two holdings. The first is the S&P 500, which accounts for around 96% of the ETF. The remaining 4% is invested in a ladder of OTM put options. During a bad crash, these put options can soar in value, which can offset the losses in the S&P 500. Similar to problems experienced by TAIL, the market never “crashed” per se, and to make matters worse for SPD, by holding the S&P 500, it lost money there too.

- SWAN (Amplify Blackswan Growth & Treasury) holds 90% of its capital in Treasuries while investing the remaining 10% in long-term equity appreciation securities (LEAPS) call options. The theory is that during bad crashes, the “flight to safety” effect and cuts in interest rates by the Federal Reserve will cause the price of Treasuries to soar, which can offset stock losses. During bull markets, the S&P 500 LEAPS mimics holding the index. The problem here is that the market did not play by the rules in 2022. The Fed did not cut, Treasuries did not soar, and the S&P LEAPS lost value.

The lesson here is that it is critically important for investors to understand how an ETF is structured and to look deep beyond the name alone. Each of the three examples above shares

similar objectives, but offers distinctly different structures and requires a very specific type of market to work.

Looking into the immediate future, it does not seem that these ETFs offer any better prospects and I suggest investors take a hard pass.

The good news there is a better way to hedge your portfolio. And fortunately, it is not that difficult.

Last year, the use of absolute relative momentum kept some Avalon models mostly in cash. There is no reason to believe that this process will not continue to guide us as the methodology is 100% systematic and mathematical.

Portfolios that are adaptive to changing markets are always my preference and never more important than during times like now.

The current allocation based on absolute momentum remains similar to our comments since the beginning of the year.

International stocks (EFA), Emerging Markets Bonds (CEW), and Mid-Cap U.S. stocks (MDY), are the current top three selections. Noticeably absent are large-cap U.S. stocks, which aligns well with concerns for U.S. stock earnings deceleration.

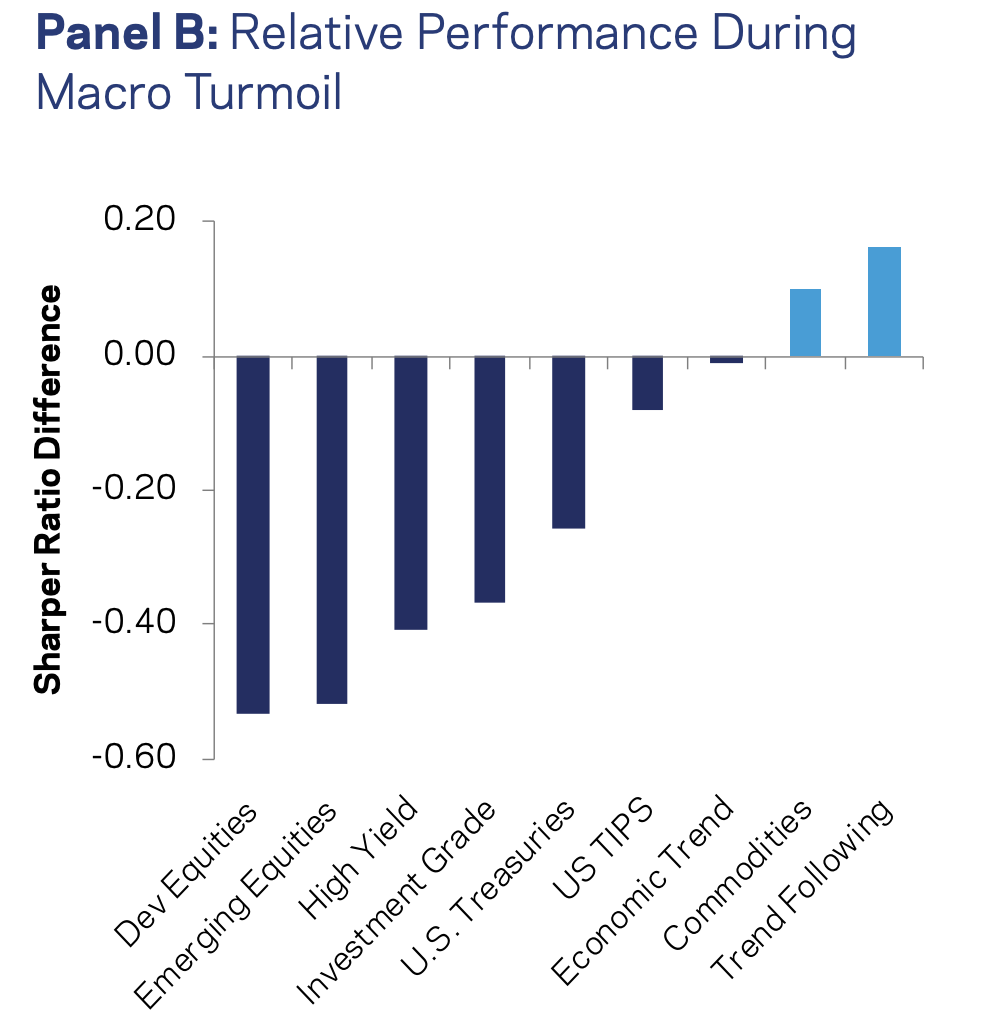

While absolute momentum did a nice job of keeping our models defensive, systematic trend-following systems shined last year with many positing double-digit gains.

A recent research report published by AQR called Should Your Portfolio Protection Work Fast or Slow makes the case for continued success with such strategies.

As previously mentioned, few approaches work as well as trend-following during market turmoil.

The additional benefit of trend-following strategies is that they not only provide benefits during market declines (due to short exposures), but also have the ability to provide a source of positive return during market recoveries as well, making them a favored strategy for investors seeking a sanctuary in these challenging times

To summarize:

- Interest rates and earnings will continue to be a driving force to equities.

- Cyclical forces increase the prospect of earnings declines.

- Traditional hedges such as gold may continue to disappoint investors.

- ETFs that market bear market protection should be avoided due to structural concerns.

- Absolute momentum and trend-following strategies should continue to provide investors with adequate risk-adjusted returns.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.