Related Blogs

March 29, 2023 | Avalon Team

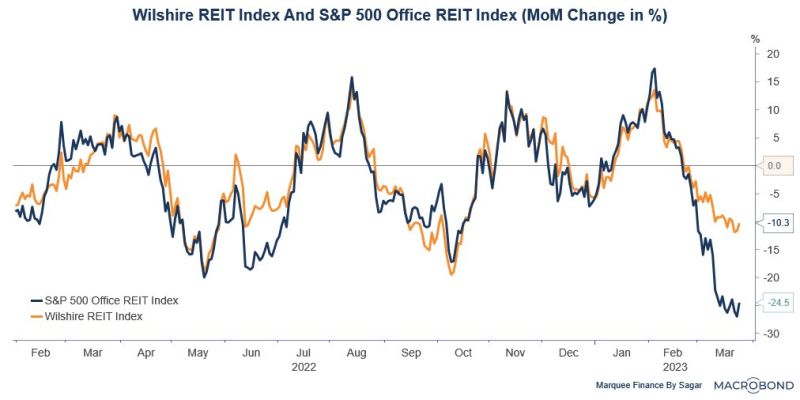

REIT investors are having a terrible year.

The guiding principle of relative strength investing is to invest in what’s strong and avoid what is weak.

The underlying principle of this approach is that assets that have been performing well in the recent past are likely to continue to do so in the future, while those that have been underperforming are likely to continue to struggle.

And right now, the weakest sector is Real Estate.

Today we’ll take a deeper look into this sector and explore the issues that have investors concerned.

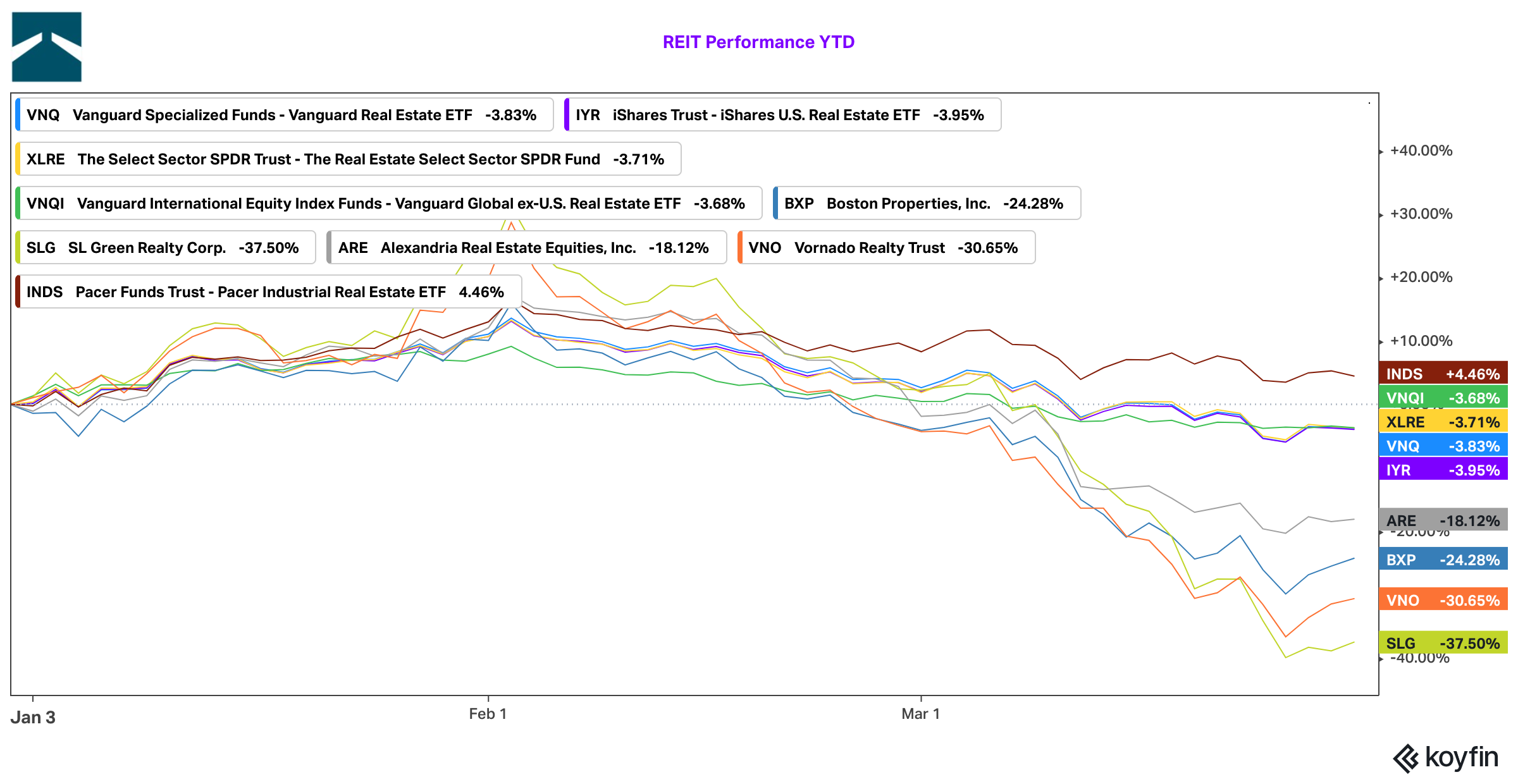

To be fair, some REITs are doing better than others.

Ex-Office REITS, hospitality, retail, hospitals, etc. are healthy and aren’t witnessing any stress yet. REITs that serve e-commerce, logistics, and storage, like the Pacer Industrial Real Estate (INDS) are up for the year.

But, some of the biggest names in the office REITs have seen enormous drawdowns in the last three months, dragging down the index.

Vornado Realty Trust (VNO), SL Green Realty Corp (SLG), and Alexandra Real Estate Equities (ARE) are some of the names that are down up to 40%, which means that markets are virtually signaling a potential default soon.

Even with positive GDP, the commercial real estate market (CRE) was already in the doldrums.

Covid created a tectonic shift in how workers view their work and many companies have found it difficult to get workers to return to a more traditional office space.

Vacancy rates are high and may get worse as work-from-home dynamics structurally reduce demand. Note too, that a recession will further increase the vacancy rates.

In recent weeks, we’ve covered the banking sector and the stresses that were being placed on banks caused by the increase in interest rates.

Banks already have enough to worry about with depositors fleeing and placing strains on banks’ balance sheets.

Before 2023, the most significant year-over-year decline we’d ever seen in bank deposits was a 1.58% drop back in September 1994. That record drop was broken earlier this year when we got a reading of -1.61% during the week of February 1.

Since that time, the year-over-year decline has only gotten worse. As of the most recent week (March 15), the year-over-year decline stands at -3.33%.

And now add the additional risk being caused by CRE…

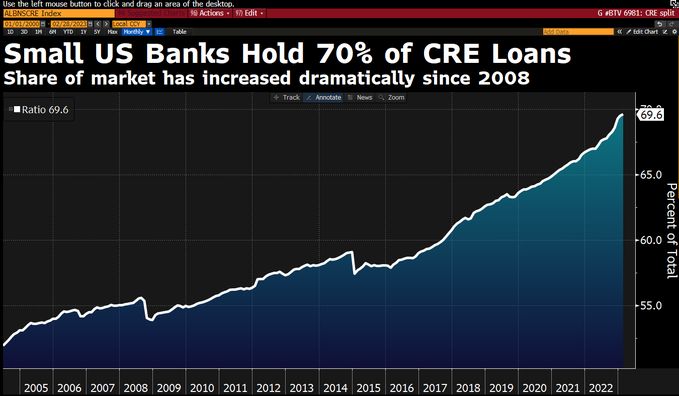

It’s important to understand that most CRE is financed by regional banks. Small U.S. commercial banks hold 70% of the total CRE loan exposure.

Small banks have more than 2.5 times the exposure as compared to large banks.

A record $862B was loaned to CRE last year, a 15% increase from a year prior, data provider Trepp estimates.

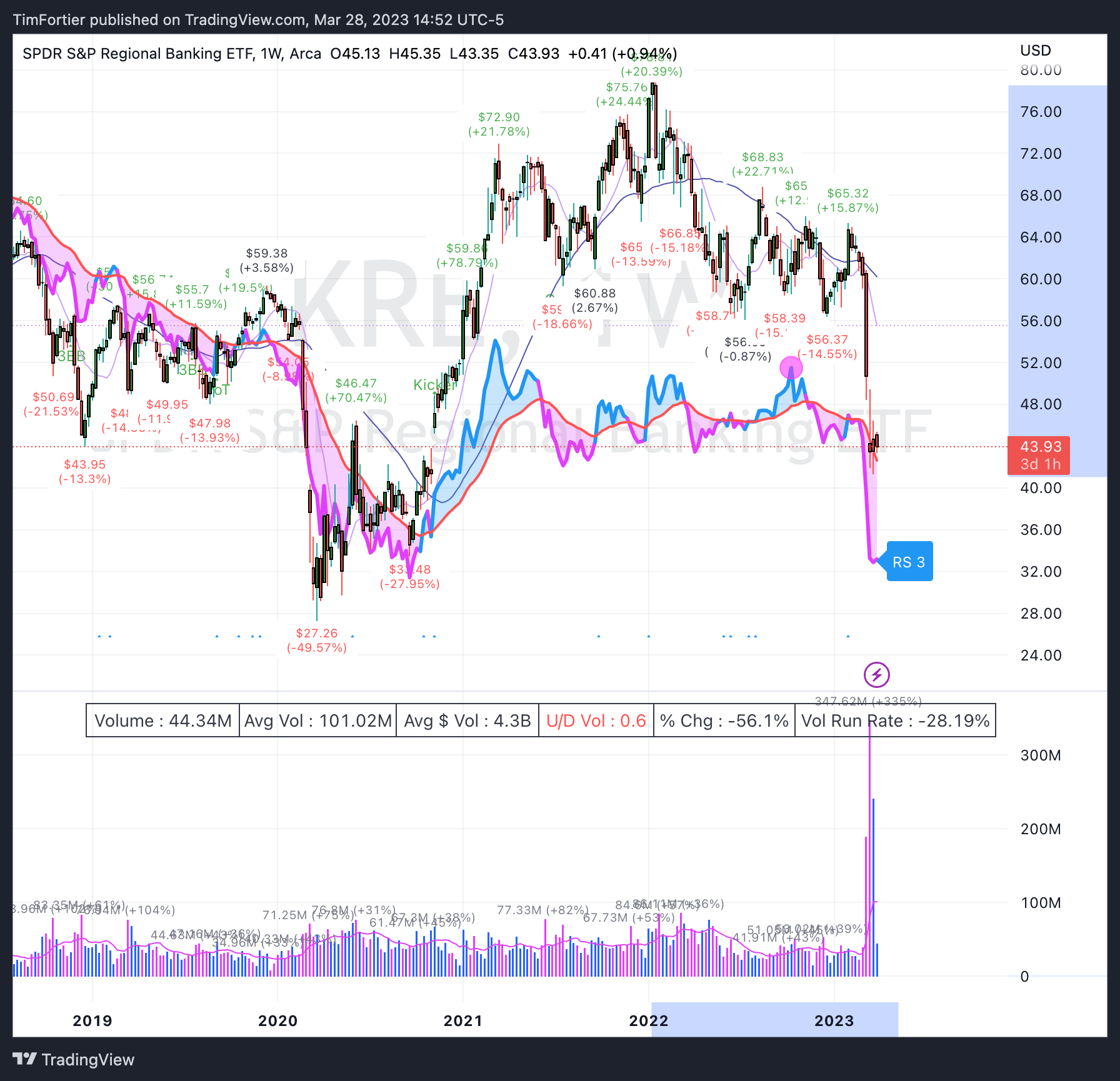

This fact has not gone unnoticed by investors as the SPDR S&P Regional Banking ETF (KRE) has lost nearly 50% from its high.

The existing pressure on banks is only going to make it worse for CRE.

Let me explain…

We will likely see the consequences of the recent events in banking down the road. Some are easier to figure out than others.

CoStar Group reports that the collapse of three U.S. banks means that one of the toughest real estate lending environments in decades is about to get even tighter, adding a new hurdle to an already challenging time for deal-making.

Note that lending standards were already at levels consistent with recessions of the past and now will almost certainly get tougher.

Tighter credit will make it more difficult for developers to access capital.

Plus, the enormous rise in interest rates is going to impact developers that are due for refinancing. Many owners like Blackstone have already defaulted on billions of dollars of loans, citing operational un-viability at the sky-high interest rates.

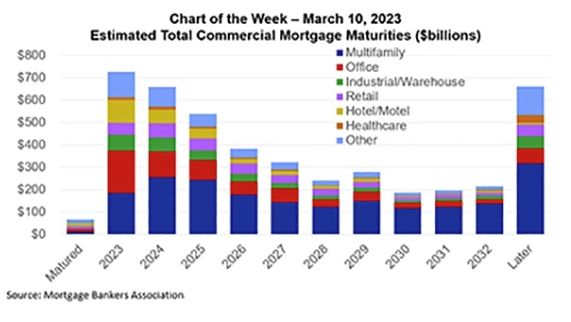

The Mortgage Bankers Association estimates that of the $4.4T of outstanding commercial and multi-family mortgages, $728 Billion (16%) will mature in 2023 with another $659B (15%) maturing in 2024.

Of this $728B of commercial mortgages maturing in 2023, office mortgages have the second largest share at $182B (25%).

To make matters worse, there are likely large office leases expiring over these next two years along with office employees continuing to work from home.

This could have a significant negative impact on NOI as office landlords look to reduce rents for tenants who are seeking less space or just have tenants move out altogether.

The Fed is not helping in this regard either, as they’ve continued raising the fed funds rate. The result of the Fed’s actions will be loan interest rates that will be significantly higher for these office building owners.

Interest rate sticker shock and potential economic headwinds (i.e. recession) could be very challenging for these office borrowers.

This means that many office buildings are now overvalued with write-downs that haven’t been taken into account yet, so the availability of construction lending for new industrial construction projects might not be readily available when needed in 2023.

The CRE sector is currently facing several macro challenges, leading to a general sense of pessimism in the market.

Many investors are adopting a cautious approach, waiting for more clarity before making any major decisions.

The prevailing view is that if a security or asset category is showing relative weakness, there must be a reason behind it.

Therefore, it is important for investors to carefully consider the underlying factors and risks before making any investment decisions in this sector.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.