Related Blogs

April 4, 2023 | Avalon Team

In the end, it was a familiar face that won the NCAA Tournament. March Madness officially ended Monday night with UConn – a No. 4 seed, beating No. 5 seed San Diego State 76-59. For San Diego, it was their first time ever to come so far.

The final buzzer on Monday night ended the 3-week period leading up to it known as March Madness, an exciting time for basketball fans.

In some ways, the 3-week period leading up to the end of the quarter was the market’s version of March Madness, as underdogs have become heroes and some familiar names have clocked the best market performance.

Let’s reflect on the first quarter and ponder where we may be heading.

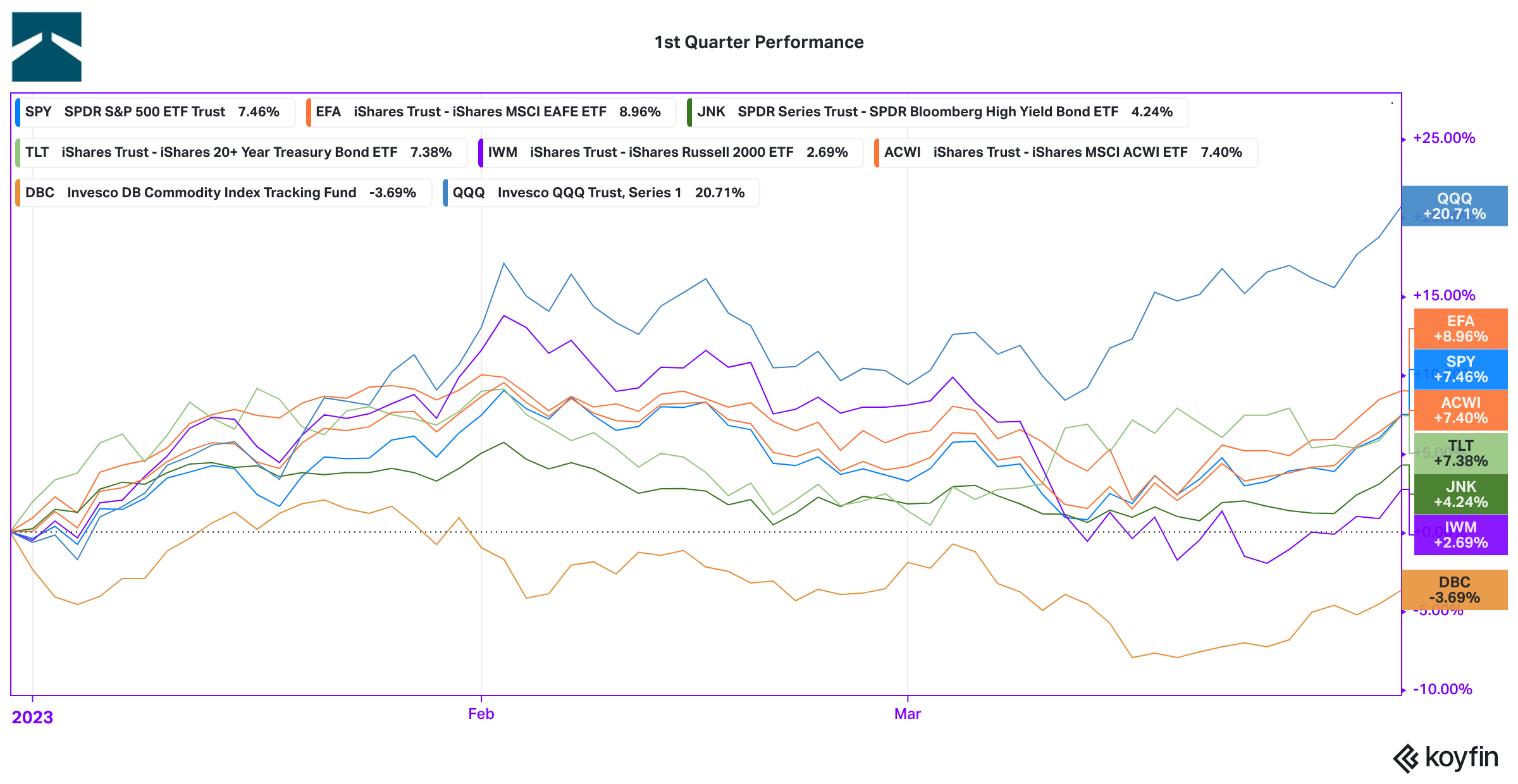

1st Quarter by the Numbers

When the buzzer went off on the quarter, the clear winner was technology, as the Nasdaq 100 finished up 20.38%, more than twice as good as international equities and the S&P 500.

March had its share of madness with some unprecedented news.

Let’s look at the highlights:

- The 2nd and 3rd largest bank collapses in U.S. history.

- Multiple countries ditch the U.S. Dollar for the Chinese Yuan.

- The Fed raised interest rates to their highest levels since 2007.

- Credit Suisse, one of the world’s largest banks, collapsed in under 48 hours and was bought by UBS.

- President Trump was indicted and is the first U.S. president to face criminal charges.

However, despite the mid-month sell-off, the month of March pleasantly surprised investors with a month-end rally, ending both the month and the quarter higher.

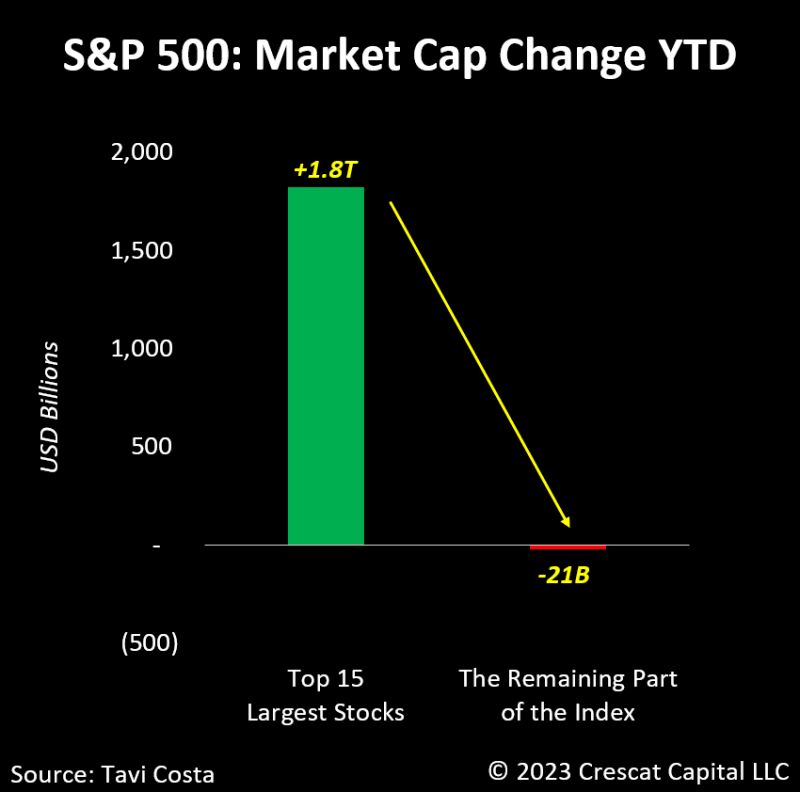

Across the entire S&P 500, the average stock was up 3% in Q1. That is much lower than the 7% that the S&P gained at the index level This means that the largest stocks in the index gained more than the smallest stocks.

This can also be seen in the wide dispersion in performance between market caps. Small caps were only able to gain 2.69% in the same period indicating how uneven the performance was.

This really points to the fact the market breadth has been quite awful.

How bad?

The entire market cap gains in the S&P 500 came from the top 15 companies. The remaining part of the index actually has lost money YTD.

Looking at the Q1 numbers, the real winner turned out to be technology as mean reversion saw 2022 worst performers become 2023 best performers.

The rally seems to have been more about liquidity, rather than fundamentally driven, as the Fed provided liquidity in the wake of the SVB bank collapse.

However, at least over the short term, there are some positives.

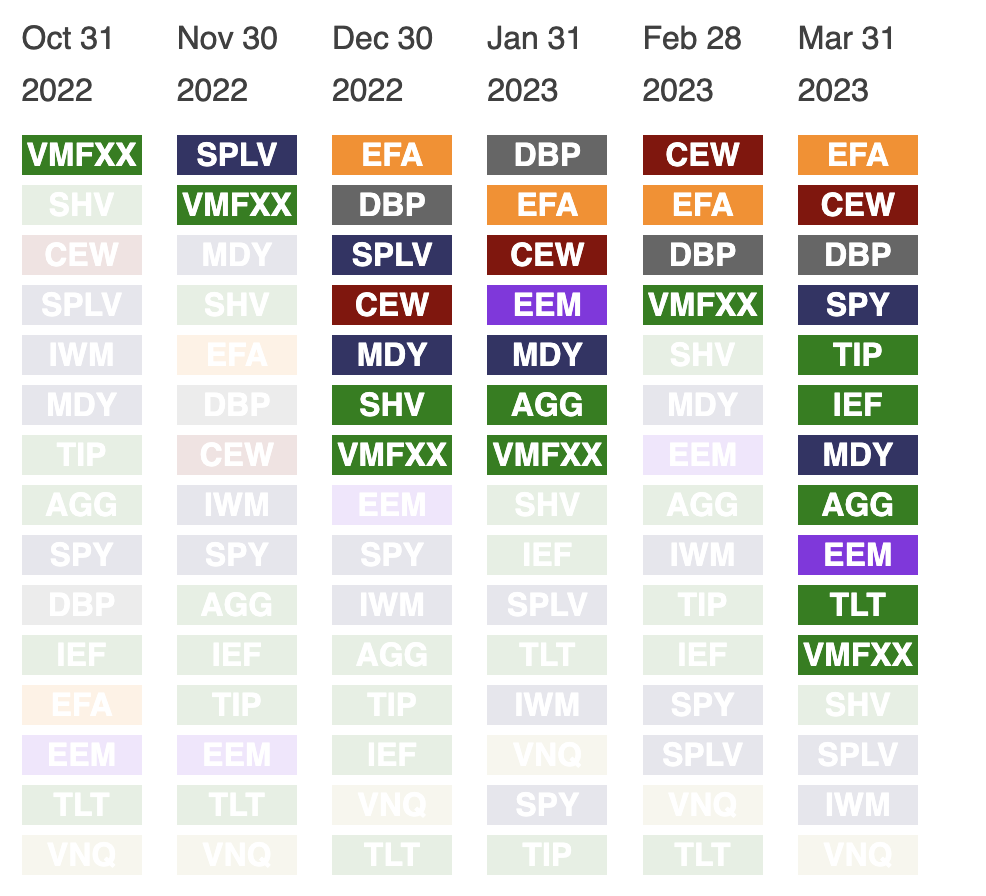

For one, the number of attractive asset classes as measured by absolute momentum has been improving as this table depicts.

In fact, this is the first time that SPY has been on this list since January 2022.

International equity (EFA) continues to dominate the top ranking along with emerging markets, non-dollar, bonds (CEW).

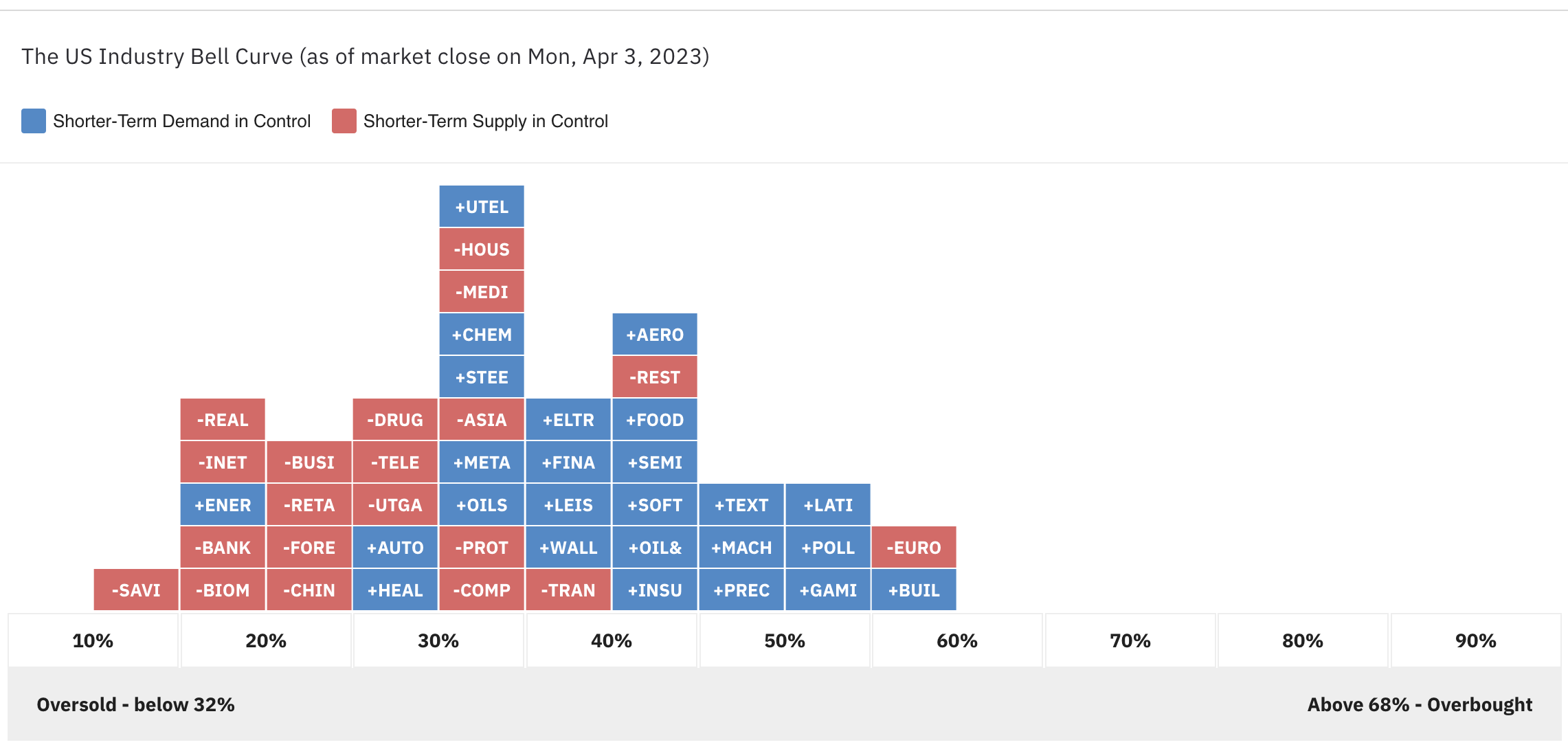

Just over 1 week ago, there were only 2 U.S. sectors with short-term demand. The picture is much improved today.

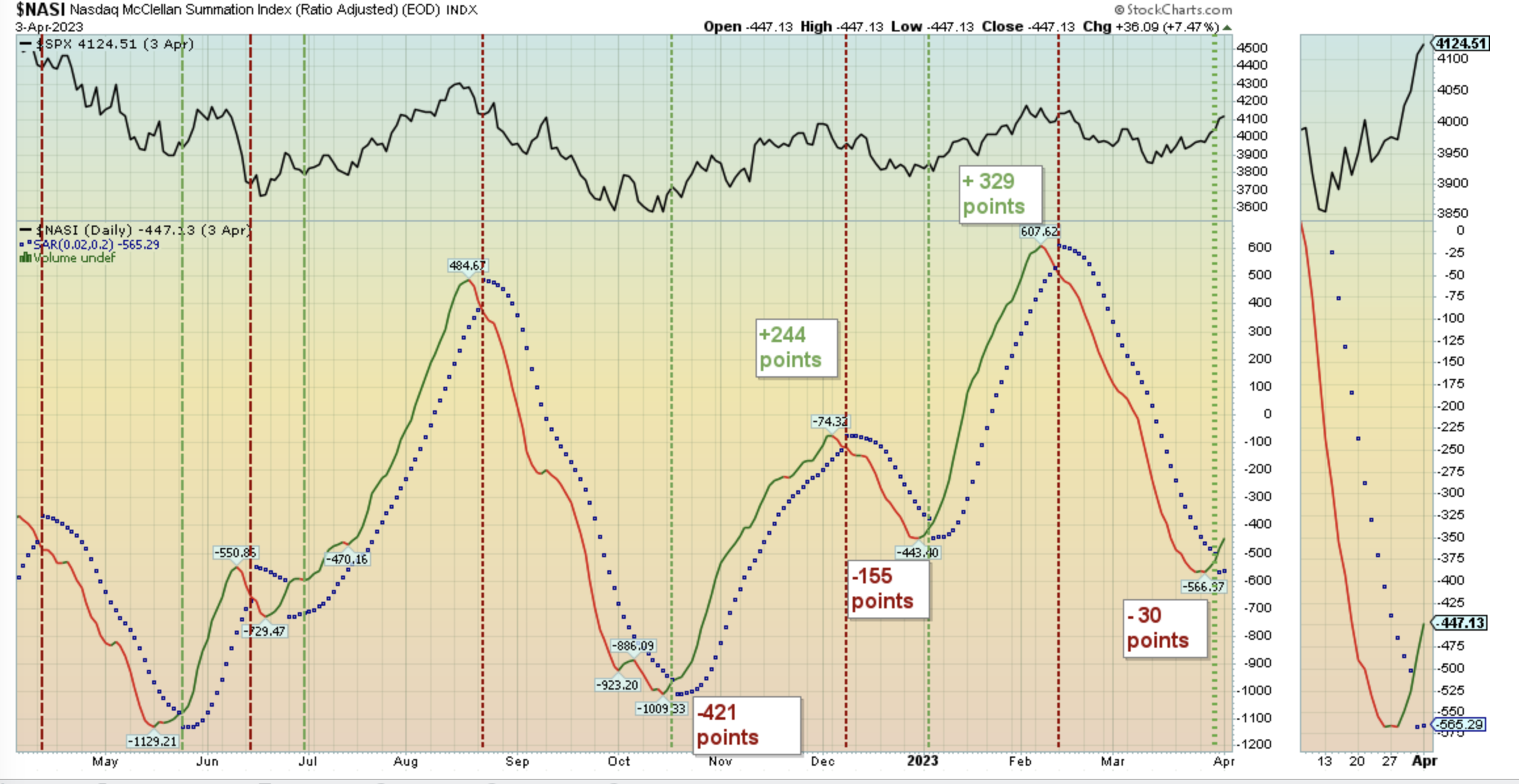

And finally, the Nasdaq Mclellan Summation Index, a breadth indicator, has recently triggered a buy signal.

And it’s as if, these indicators were right on cue.

April seasonality trends suggest the buying pressure could continue. Since 1950, the S&P has posted average and median April returns of 1.5% and 1.2% respectively. In addition, the index (S&P 500) has finished positive during the month 71% of the time, marking the highest positivity rate on the calendar.

But, be forewarned as there remain a number of concerns, chief among them, the growing signs of a recessionary slowdown.

The current rally in stocks has been partially based on the idea that the Fed will pivot. Indeed the bond market has shown some improvements in performance as yields have declined from their recent highs,

And now that Credit Suisse has been absorbed by UBS, and the Fed has bailed out depositors of SVB, all is well right?

But there are some issues…

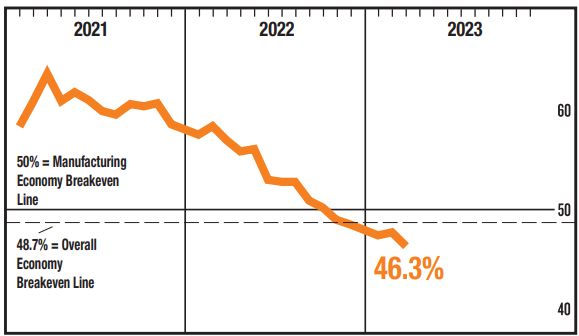

First, make no mistake about this. The economy is slowing.

The ISM U.S. Manufacturing PMI was 46.3 in Mar, down from 47.7 in February. The New Orders Index fell -2.7 pts to 44.3, while the Production index was mostly flat at 47.8. The Prices index fell below 50 to 49.2, down -2.1 pts.

Manufacturing is slowing down pure and simple. Negative EPS estimates are likely to accelerate as this declines.

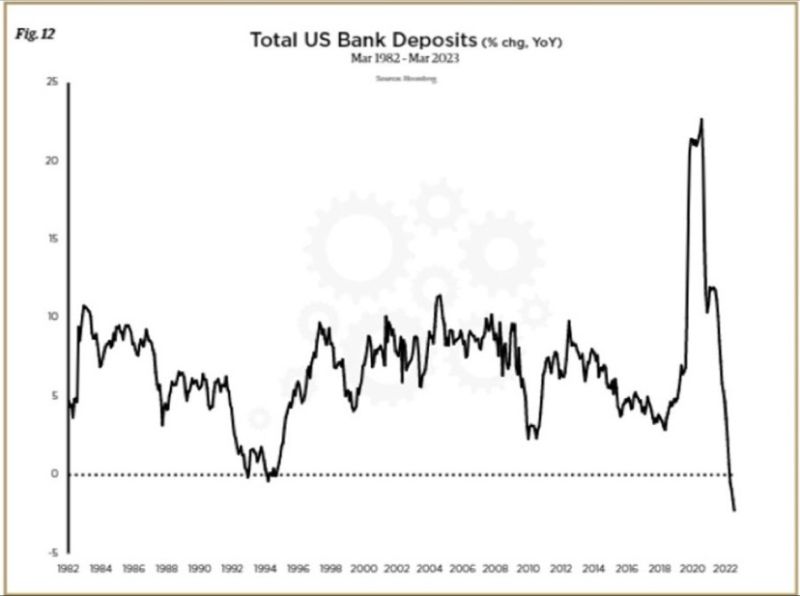

Money is still being drained from the banks.

This has, at a minimum, tightened lending making less capital available. Thus, the requirement for self-financing penalizes growth tech, biotech, real estate development, and banks.

So add these sectors to those that will become “earnings challenged” in the coming months.

JPMorgan economists see a sharp slowdown in bank lending growth to 2% this year from 12% in 2022.

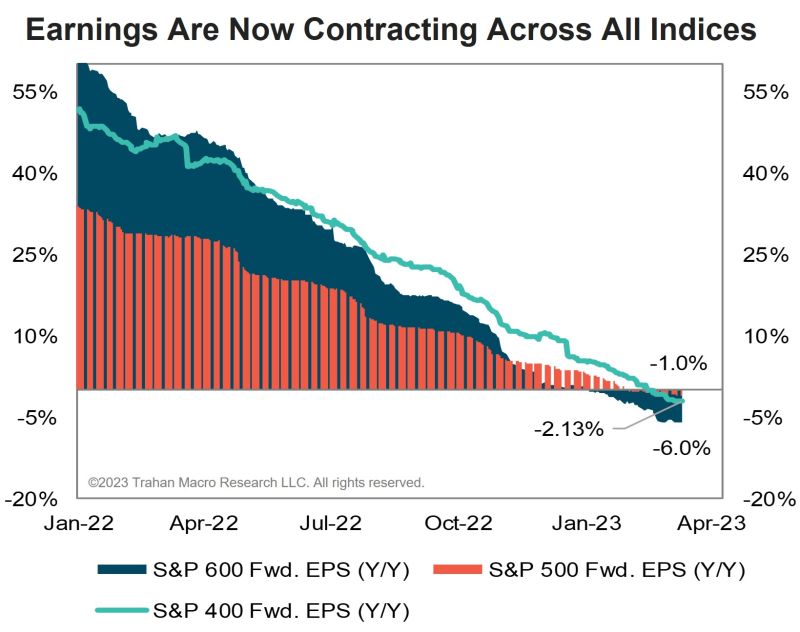

Earnings are now already contracting in small-cap stocks, mid-caps, and the S&P 500.

If you are a stock investor, earnings should be your primary focus. Everything else is just noise.

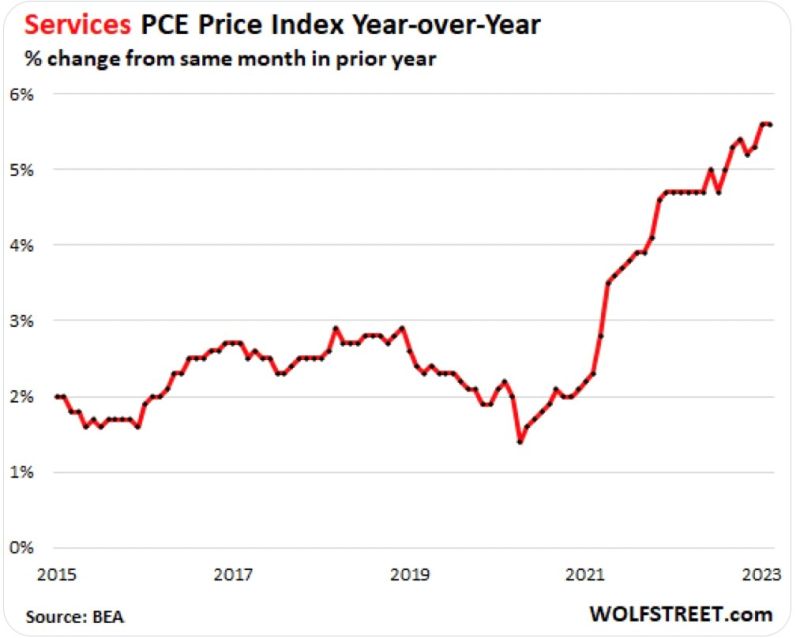

Finally, on the inflation front, the main reason the Fed continues to raise rates, despite the banking crises, fall in shelter prices, along with other components of the Core PCE Price Index (Fed’s CPI benchmark) is the rapid and stubborn rise in services inflation that represents about two-thirds of consumer spending, which is at its highest rate since 1984.

Add to this the surprise cut in production by OPEC which has just made the Federal Reserve’s job even that much tougher given that oil is a major input to the US economy.

In summary, while the first quarter rewarded select slivers of the market, the market leadership needs to continue to expand.

But given the outlined challenges, March may be a tough act to follow.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.