Related Blogs

July 15, 2022 | Avalon Team

This week marks the kickoff to earnings season – that magical time of the year when a large number of public companies release their quarterly earnings reports.

This season in particular is going to be a nail-biter as we’ll learn what the impact is of rising inflation, rising interest rates, and a strong dollar on a company’s bottom line.

There is a lot riding on these reports.

In a tumultuous first half, just the Nasdaq 100 alone, wiped out $5.6 trillion in market value with rate hikes hitting stocks valued on future earnings, inflation driving up costs, and the threat of recession weighing.

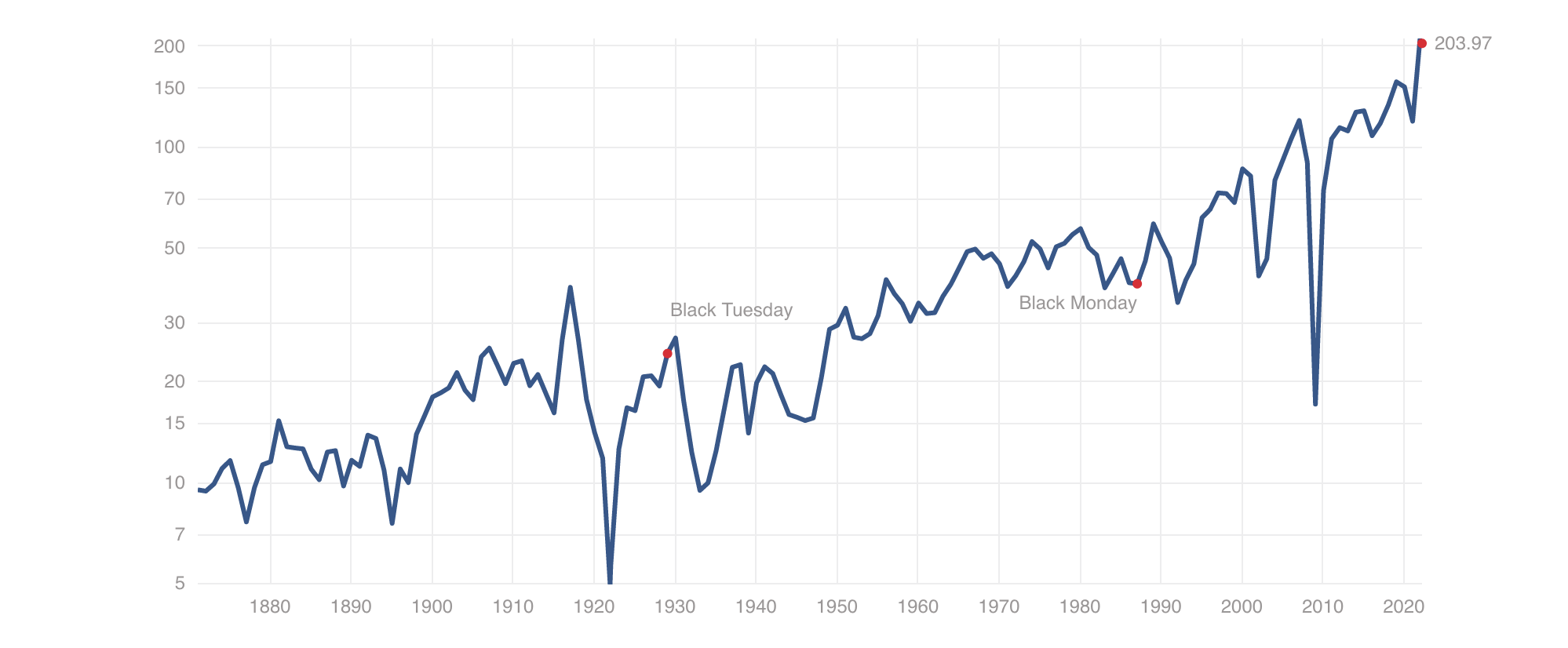

Trailing earnings for the S&P 500 are $203.87 as of March 31, 2022.

Aggregate earnings for the S&P 500 had been sequentially flat in the two years preceding the 2020 Covid crisis. As the economy responded to the massive Fed injection of money, 2021 earnings experienced a meteoric increase of nearly 50%, which is more of an anomaly.

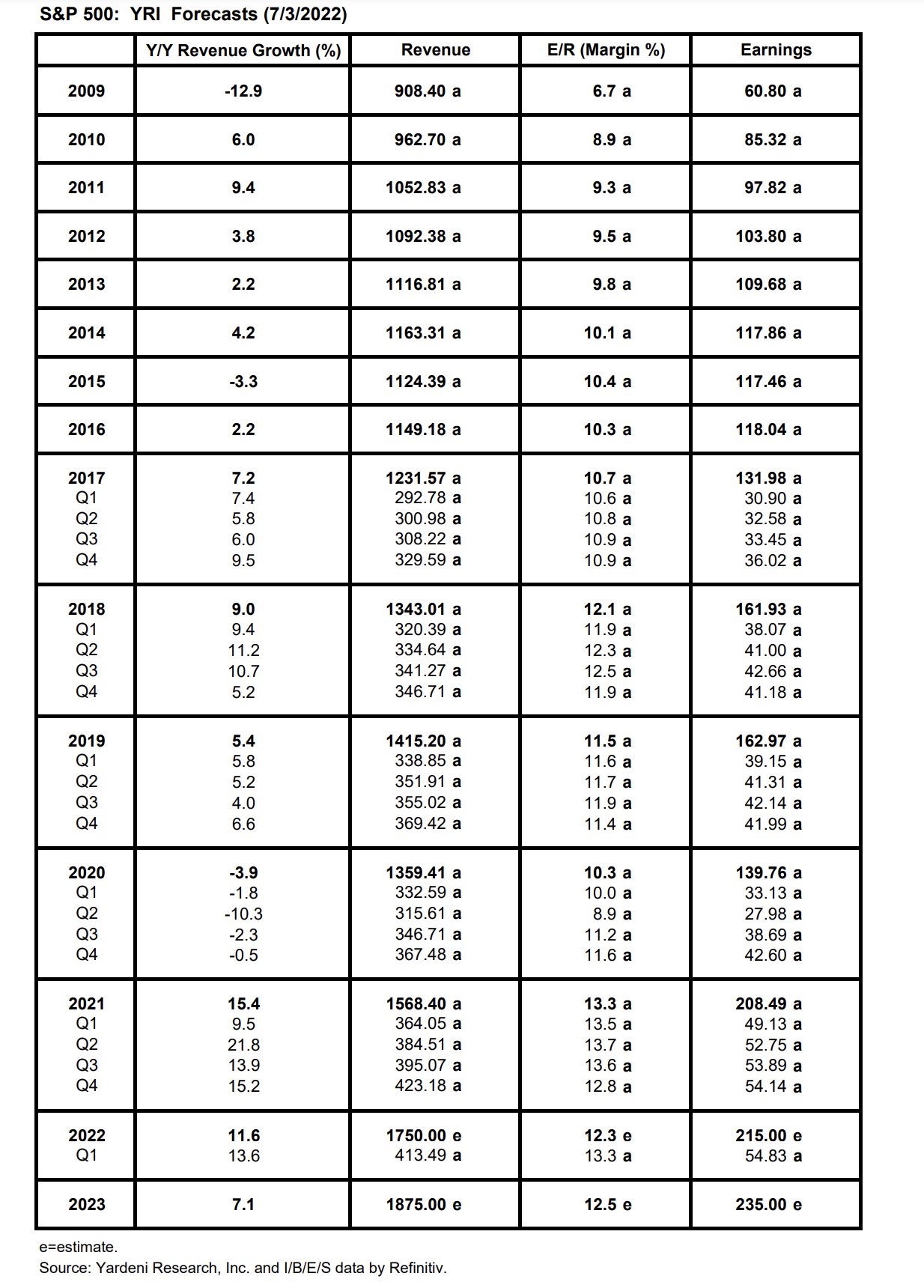

According to Yardeni Research, revenues in the coming 12 months are expected to grow at a rate of around 7%, with S&P earnings growing at around 9%.

We shall see…

Several banks gave us a shaky start to the earnings season.

The nation’s largest bank, JPMorgan (JPM: NYSE), fell 3.5% yesterday after earnings and revenues came in below analyst expectations. The 28% YOY profit decline resulted from its $1.1 billion provision for credit losses, comprised of a $428 million reserve build and $657 million in net loan charge-offs.

The bank’s CEO, Jamie Dimon, expressed mixed sentiment, saying that the economy continues to grow, the job market is healthy, and consumer spending and balance sheets remain healthy.

But, on the other hand, he did say the deteriorating data and challenging environment for businesses and consumers are very likely to negatively affect the global economy at some point down the road.

Meanwhile, the slowdown in global dealmaking caused Morgan Stanley’s (MS: NYSE) profits to fall 30%, missing analyst estimates for the first time in nine quarters.

Wells Fargo (WFC: NYSE) announced today that their earnings fell by 48% and that they too are setting aside funds for bad loans. The bank also cited that rising mortgage costs have resulted in a decline in the mortgage business.

Signs of how consumers are reacting to rising costs showed up in ConAgra Brands’ (CAG: NYSE) earnings report. The maker of Hunt’s canned tomatoes forecasted annual earnings below Wall Street expectations as inflation-induced price hikes dent demand for frozen foods and snacks while mounting costs crimp margins.

The company also reported a 6.4% drop in fourth-quarter sales volumes with consumers showing signs of push-back against price increases.

I remain very concerned that the consumer pushback is going to cause a greater decline in earnings than most analysts expect.

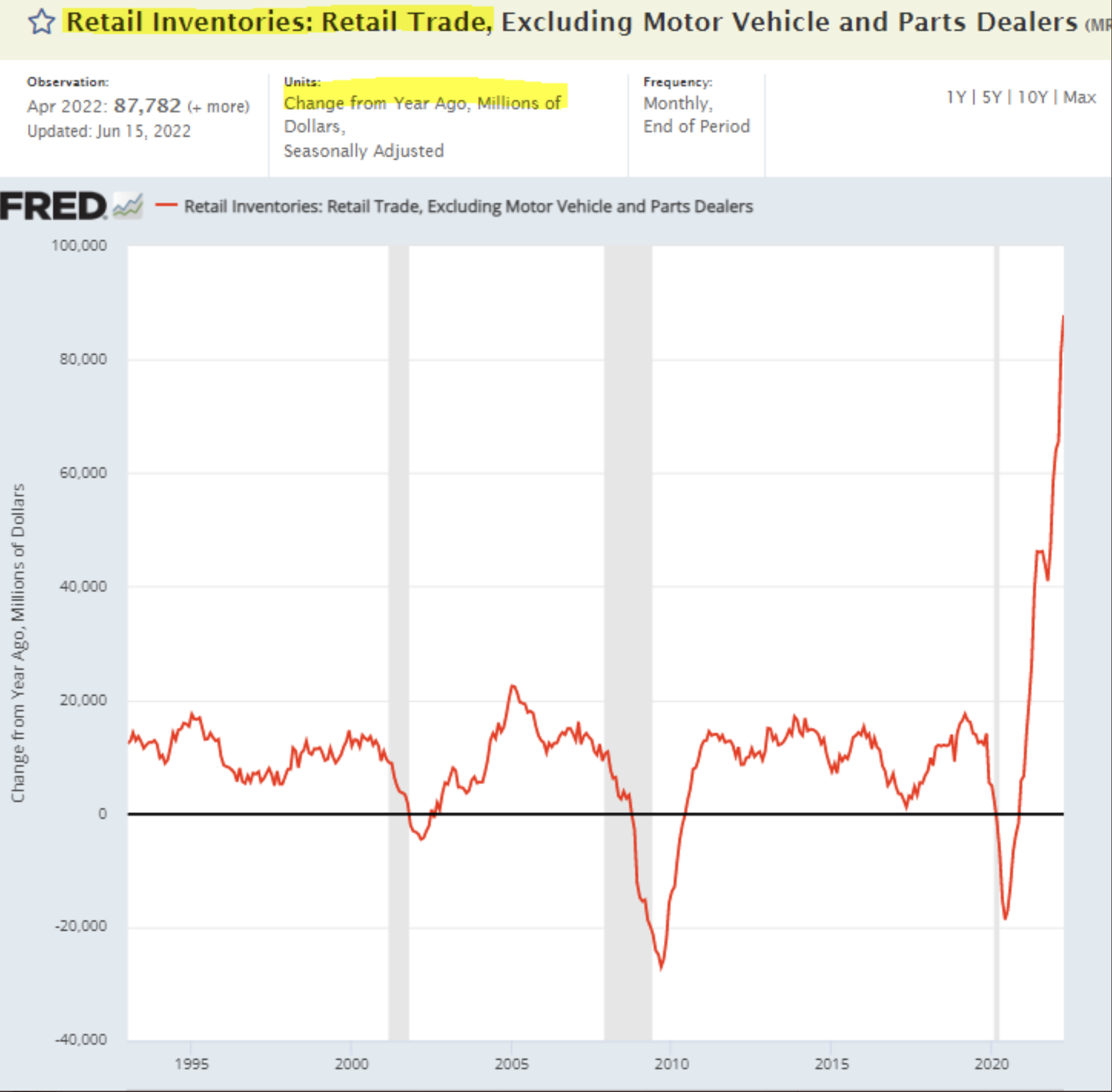

Consider the following data on inventories.

Retail inventories continue to surge. We already know what a debacle earnings were at retail giants Target and Walmart. As inventories build, eventually goods will be liquidated at lower prices resulting in lower (if any) profit margins, which of course leads to lower future earnings.

Today we got word that June Retail Sales came in at +1.0% – better than the expected +0.9% estimate. But, this number was elevated due to the additional costs related to gasoline sales and food.

Unlike many other government numbers, the retail figures are not adjusted for inflation, which rose 1.3% during the month, indicating that real sales were slightly negative.

Two other charts also make me cautious.

The first is the ISM Manufacturing PMI, which is one of the most widely watched and trusted measures of manufacturing activity and overall economic health.

The ISM Manufacturing PMI is highly cyclical and captures the “growth-rate cycle” quite well.

Underneath the headline, ISM numbers are several sub-components, including new orders, inventories, employment, prices paid, and more.

A reading above 50 signals an expansion or positive growth, while a reading below 50 signals contraction or negative growth. The ISM Manufacturing PMI is a remarkable indicator that strongly correlates to changes in asset prices, corporate earnings, and more.

The spread between the new orders and inventory readings is a reliable leading indicator of the overall ISM Manufacturing PMI. This makes sense because if new orders are falling faster than inventory, companies have to cut production in the future to combat a building imbalance.

The spread between the ISM new orders and inventory sub-subcomponents crashed in June, which is a strong warning sign that future declines in the overall ISM Manufacturing Index should be expected.

Given that the ISM Manufacturing PMI holds a very strong correlation to earnings estimates, further declines should be a warning sign.

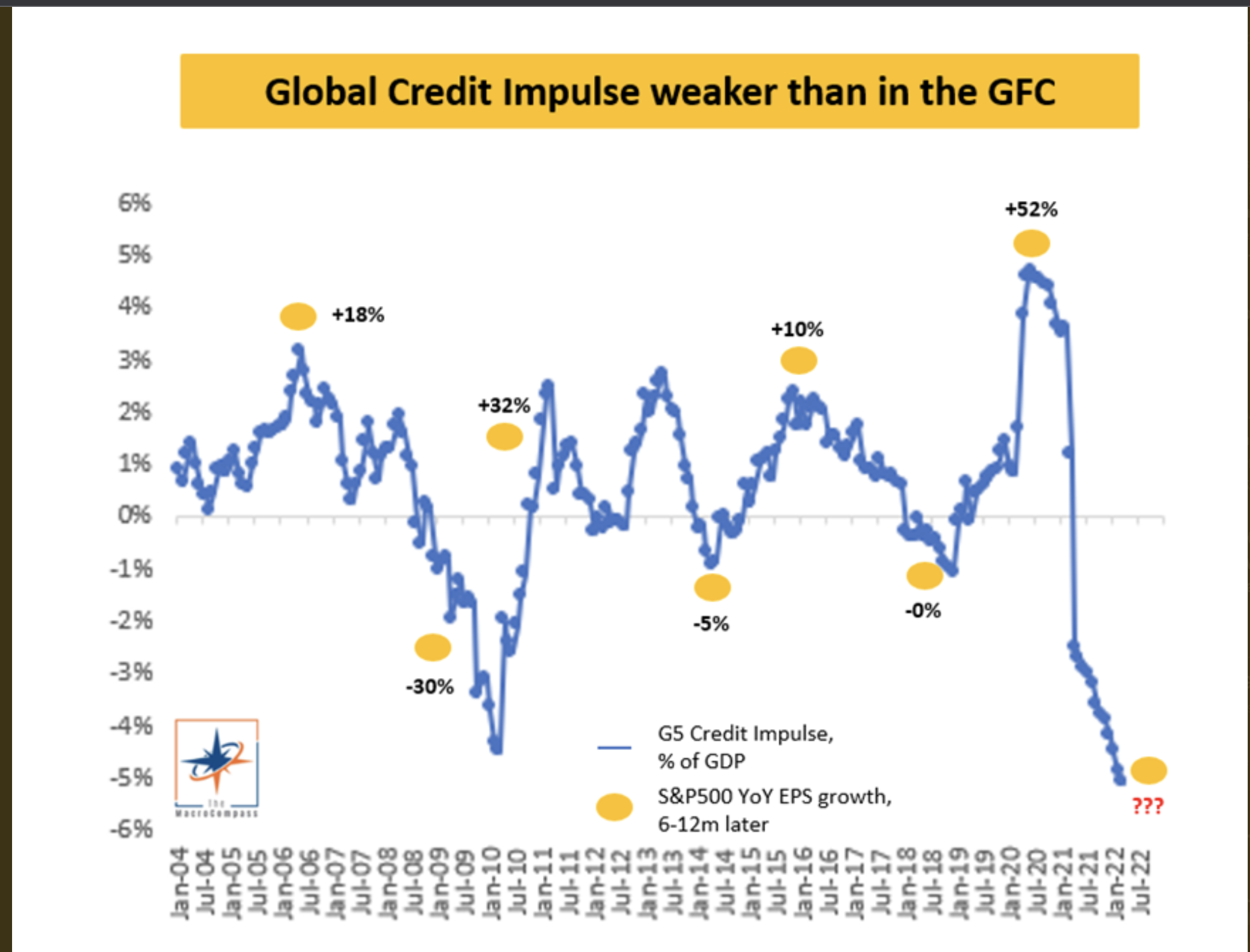

Finally, although I don’t see this indicator being discussed mainstream, the Global Credit Impulse has done a good job of leading the economy. This indicator measures the creation and flow of new credit.

Credit is one of the largest drivers of economic growth and is used to facilitate new manufacturing, purchase orders, etc.

China has been on a near shutdown basis as its strict Covid policy takes its toll. Elsewhere, European manufacturing is slowing as energy and other commodities have become scarce.

Add to that the negative impact of a strong U.S. Dollar on emerging markets and it’s not too difficult to understand why global economic activity is rapidly declining.

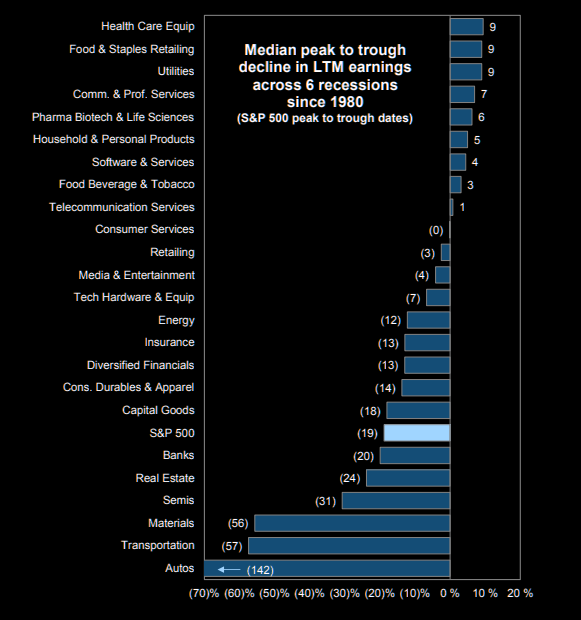

Given that it seems nearly certain we’re heading into a recession, I thought the following data was interesting. It shows how previous recessions have impacted various sectors of the economy.

Some of the best-performing sectors during recent weeks are among the same sectors that have held up the best during prior recessions…

Could it be that institutional investors are already in their “recession playbook”?

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.