Related Blogs

March 23, 2023 | Avalon Team

It’s about to get interesting… I think we’re about to see some bodies.

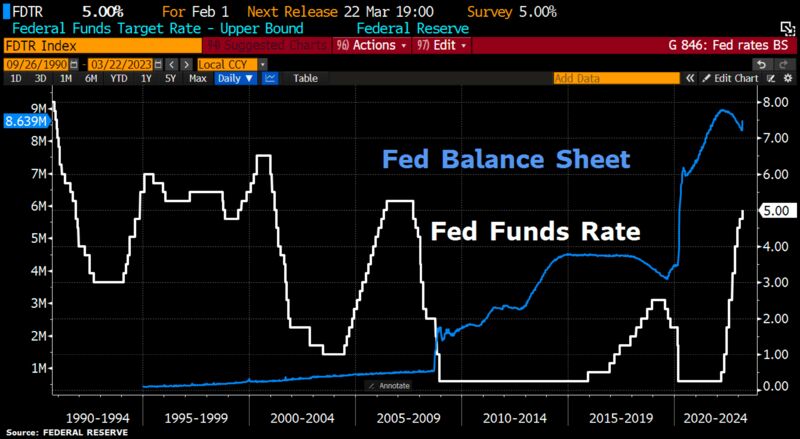

Yesterday, the Federal Reserve announced another 25bps increase in interest rates.

The Fed and Jay Powell made it clear that there is no trade-off between taming inflation and financial stability.

Echoing the thoughts of his European counterparts, Jerome Powell said it’s the Fed’s priority to bring down inflation to its long-term target of 2%.

This puts the Fed Funds rate at 5%, still 1% behind the recent 6% annual increase in CPI.

The guidance was slightly less hawkish than the last policy, as the Fed stated: “some additional policy firming may be appropriate.”

This reflected a change in tone as “ongoing rate increases” was changed to “some” and “may.”

Perhaps the Fed understands that banking stress is ultimately disinflationary, as the flow of credit to the real economy slows down, and so does economic activity, and inflation with it.

Let’s look more closely.

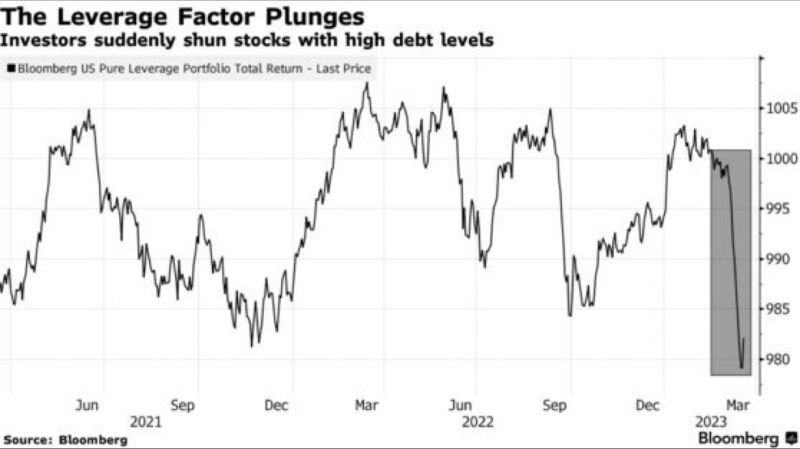

First, the markets have suddenly begun to realize that higher rates will lead to the demise of highly leveraged companies.

Popularly known as “zombie companies,” these are the ones that don’t generate enough EBIT to cover their interest costs, or in other words, have an interest coverage ratio less than 1.

Bloomberg has an index called “Bloomberg US Pure Leverage Portfolio” that goes long on highly leveraged companies and short on the ones with less debt.

Unsurprisingly, the index has seen one of the sharpest declines on record post-SVB fallout.

The triple whammy of demand slowdown, tightening lending standards, and loss of pricing power will lead to these companies defaulting on their debt.

As a result, bankruptcies will rise, succeeded by a rise in unemployment.

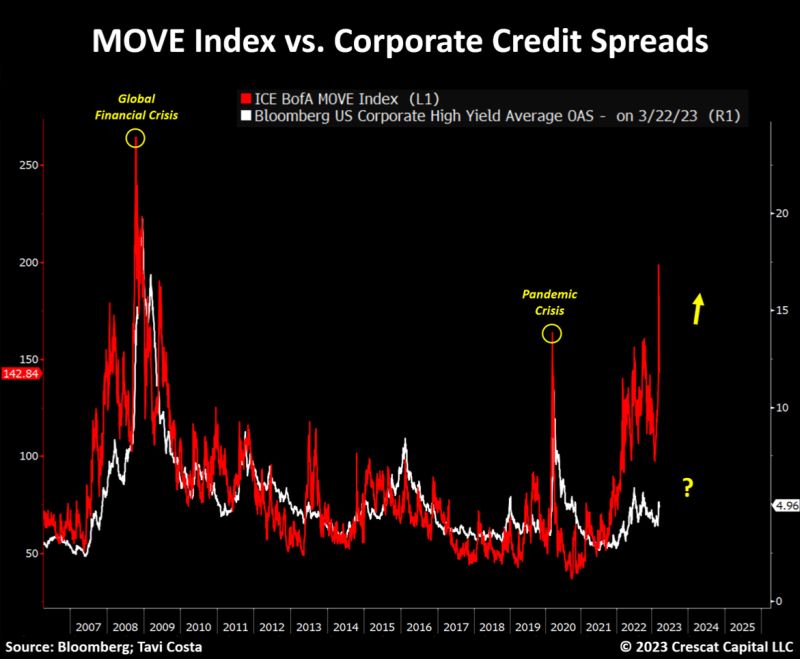

Next, the recent surge in bond volatility suggests that corporate spreads remain too tight and are likely to move significantly higher.

As default risk is starting to increase, this could add even further pressure on the cost of capital to rise.

While the announcement from the Fed was not too surprising, the knockout came from Janet Yellen…

Mainly because she said the complete OPPOSITE of what Powell was saying at his conference about deposits being insured.

She pretty much completely “walked back” previous comments about guaranteeing all $18 trillion of deposits in the U.S.

JP Morgan estimates that $1 trillion has flowed out of vulnerable banks since 2022, BUT $500 billion of that came between March 18th–March 25th during the SVB collapse.

Why is money flowing out of banks?

1) Money market funds are yielding 5%, and banks are paying close to 0%. Unless bank rates move up then money will keep flowing out. If they do raise deposit rates, this will hit bank profitability. Ironically, the Fed raising rates even higher last night means that the pressure is now greater.

2) Because of the FDIC insurance cap of $250K, $7 trillion is completely uninsured. As noted by JPM, money markets invest in the safest/most liquid instruments so are now actually perceived to be safer than keeping your money in a bank.

So it’s likely, that in the coming days and weeks ahead, we will continue to see deposits being yanked from the banks, increasing the concern that more banks may run into trouble as they are forced to sell assets held in their portfolios at a loss.

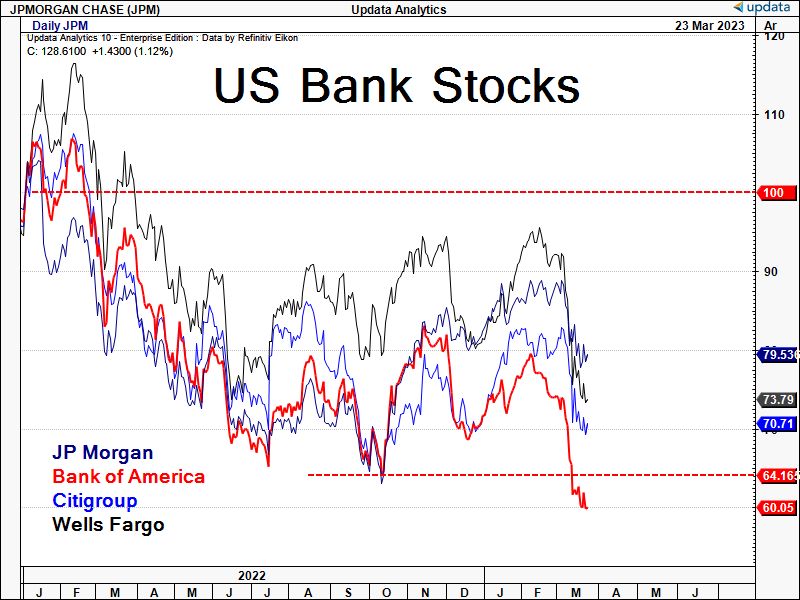

And the bank stocks are reflecting these concerns.

The banking crisis triggered by the failures of Silicon Valley Bank and Signature Bank will likely lead small and midsize institutions to prioritize having a healthy balance sheet which in turn will lead to tighter lending standards.

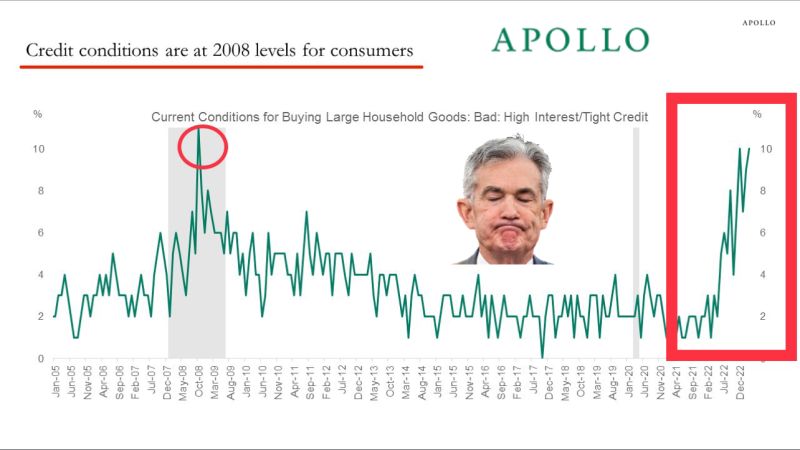

Now, even before the recent bank failures, conditions were getting worse for the consumer.

Private Equity Giant Apollo Global Management, Inc. says credit conditions for consumers are at 2008, global financial crisis levels.

And this University of Michigan survey was taken BEFORE the Silicon Valley Bank and Credit Suisse collapses.

Consumption is the engine of the U.S. economy and can make up as much as 70% of the GDP.

But now the combination of lagged Fed hikes and tighter lending standards, points to a sharper-than-expected downturn in the economy than previously expected.

Powell had this to say about the banks and the tight lending:

“Such a tightening in financial conditions would work in the same direction as rate tightening […] You can think of it as being the equivalent of a rate hike or perhaps more than that.”

For investors, the fallout from all of this is likely to be rising unemployment, slowing growth, and slimmer profit margins…

Which leads me to believe that the markets have further to go on the downside in the months ahead.

Buckle up.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.