Related Blogs

March 3, 2022 | Tim Fortier

In the popular investment book A Random Walk Down Wall Street by Burton Malkeil, the author argues that asset prices are purely random. As a result, investors should just “buy and hold.”

In the popular investment book A Random Walk Down Wall Street by Burton Malkeil, the author argues that asset prices are purely random. As a result, investors should just “buy and hold.”

This thought has led the investment industry (and many investors) to simply close their eyes and hope for the best.

There are several glaring problems with this approach.

Maybe most obvious is that it leaves your outcome purely to chance – just like gambling.

Who wants to gamble on their financial future? Seriously?

It can also subject investors to significant drawdowns. In 2008 for example, investors lost a combined $7 trillion… all because of randomness…

Traditional advice tells you to endure losses in hope that prices revert in the long run, but “long run” may not work depending on your age.

Plus, there’s increased likelihood that investors will cash out and not benefit from any rebounds due to lingering doubt in the market.

Even worse, large losses can force investors to change their lifestyle.

The problem with Random Theory is that it simply isn’t true. Prices are not as random as you think…

For instance, the cost one pays for a security creates a path of loss aversion. This is played out one investor at a time and collectively as the market whole.

Random Walk and Modern Portfolio Theory both assume that investors are rational, treating the potential for gain the same as the potential for loss. But this is not how it plays out.

The pain of loss is much more intense than that emotion derived from the pleasure of gain. As a result, investors are more likely to react to falling prices than rising prices.

Let’s also talk about Momentum Factor – one of the most researched factors of all, momentum suggests that a price in motion stays in motion.

It’s not uncommon to see “momentum securities” trend for several months at a time.

So, if prices were truly random, and not path-dependent, then we’d expect the path a security takes to look like that of a drunken sailor.

The acceptance of randomness by investors and the adoption of buy-and-hold strategies leads investors to manage risk by diversification. The idea is that the price path that one security takes may offset another security that may be declining in value.

This is such an important assumption that it is a key input in Modern Portfolio Theory.

Once again, theory and reality are two separate things.

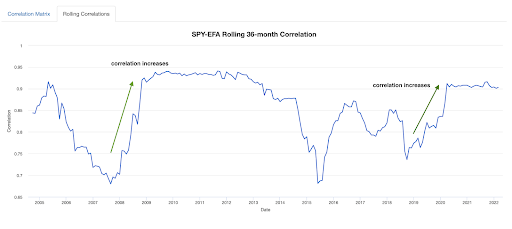

As it turns out, correlations among securities are anything but static.

Since 1971, the correlation between the S&P 500 and MCI EAFE has ranged from -0.2 to 0.94. That’s hardly stable!

But even worse is that when investors most need securities to be non-correlated, is exactly when the securities become the most correlated.

Check out the chart below and the correlation between SPY and EFA. During the Great Financial Crisis in 2008, and again during the Covid-19 market crash, the correlation approached 1.00.

That’s because both Random Walk and Modern Portfolio Theory both fail to recognize the systemic risk that is non-diversifiable.

Systemic risk accounts for as much as 75-94% of investment return (depending on the study), yet it’s not even addressed within the ivory towers of Random Walkers and Modern Portfolio Theorists.

It really doesn’t matter how you arrange the chairs if you’re doing so on the deck of the Titanic…

The global macro forces at work are resulting in an economic regime change that traditional portfolio strategies often fail to recognize.

The traditional techniques of diversification may help improve performance on a relative basis… but again, they fail to mitigate systemic risks that may cause the investor to suffer a loss.

A portfolio manager that suffers an 8% loss when the market loses 10% is considered “successful,” yet the investor has only 0.92 cents of every dollar invested.

This is the fallacy of relative returns. And it’s why it’s so important for money to be managed on an absolute return basis instead.

A loss of any amount, even if it’s “better” than some arbitrary index being used for comparison, is still a loss. You can’t spend your losses.

Now more than any other time in recent history, it’s critical to take a “risk first” approach to your portfolios.

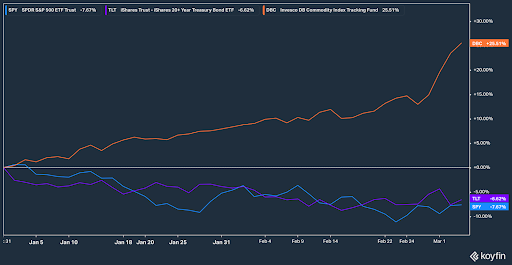

As I warned in my series The Death of 60/40, rising correlations between bonds and stocks could cause many investors’ portfolios to suffer larger than expected losses.

Both bonds and stocks are negative for the year.

Commodities continue to demonstrate persistent price strength, that has only been exacerbated by the war in Ukraine.

As I believe risk management is the most critical element to long-term investment success, I plan on writing more on this topic in the coming weeks.

Stay tuned until next time,

P.S. Rowe Wealth can help you manage risk and your portfolio – just give us a call. You can schedule a free 1-hour consultation here.

Tags

Get Our FREE Guide

How to Find the Best Advisor for You

Learn how to choose an advisor that has your best interests in mind. You'll also be subscribed to ADAPT, Avalon’s free newsletter with updates on our strongest performing investment models and market insights from a responsible money management perspective.