Related Blogs

January 5, 2023 | Avalon Team

One thing I enjoy about investing is that the markets and the economy are like trying to solve a giant jigsaw puzzle. Rarely are you given all the pieces together to complete a scene but instead, you must piece together little bits of evidence, one at a time.

The added challenge is that markets often anticipate economic events in advance, so by the time the actual event occurs, the market is off chasing the next “big idea.”

From Wednesday’s Fed minutes, we were reminded that the Fed is maintaining its resolve (in case we forgot from just a couple of weeks ago) to keep interest rates higher as not one Fed member supports a rate cut in 2023.

Toss in the fact that Minneapolis Fed President Neel Kashkari, who is now a voting member of the FOMC this year, started the day by saying that rates need to go up by another 100 bps before he thinks we’ve done enough.

I think it’s pretty clear that rates aren’t going down anytime soon.

And we know the impact that this has had on investors.

I will not belabor the difficulties of last year’s market, only to say that since the 1920s, the 10-year Treasury bond has declined by more than 10% only once – an 11% loss in 2009 during the financial crisis. In 2022, the 10-year bond lost 18%, making it only the second time this dubious feat was accomplished.

Moving forward though, with the Fed closer to the end rather than the beginning of increasing rates, I think the risk shifts from duration risk to credit risk.

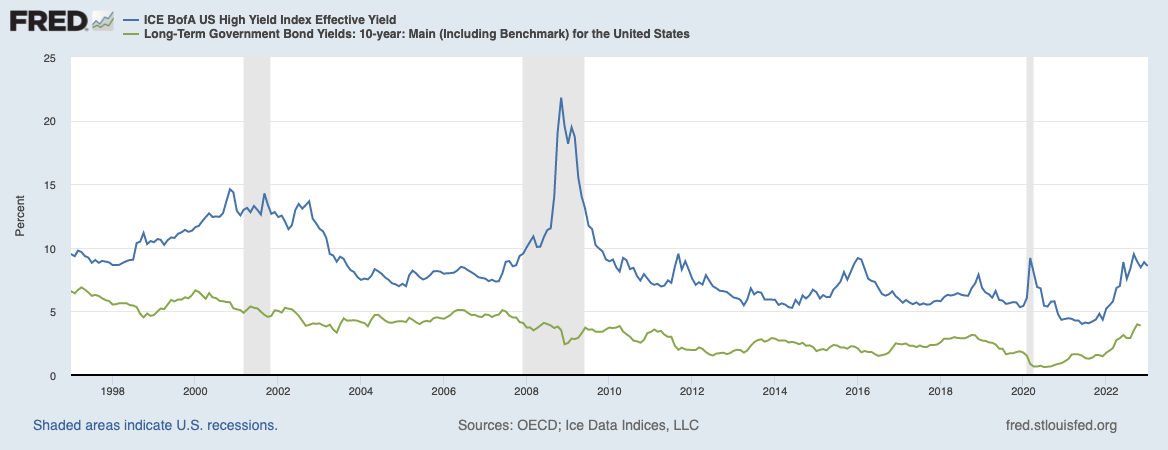

Today, even though stock and bond prices have been declining, even though the Fed has been aggressively raising interest rates, and even though a recession may be ahead of us, high-yield spreads have remained quite subdued.

This chart shows that the spread between “junk” yields and the 10-year has remained relatively constant.

This can’t last for much longer, and at some point, if we do indeed enter a severe recession, credit spreads are likely to blow out and junk debt becomes the biggest source of pain. And spreads would spike as they did in 2008-2009.

Speaking of recessions, I hate it when I see the consensus so aligned on a topic, and as it seems, just about everyone expects a recession in 2023.

While the jobs data does continue to suggest a tight labor market, I wonder for how much longer?

Layoffs are picking up steam. Yesterday, Salesforce (CRM) announced that they would eliminate 8,000 jobs and Amazon told us that they would cut 10,000 jobs. Andy Jassey (AMZN CEO) had to do a do-over after an insider revealed that 10,000 jobs weren’t really the number, it was really 18,000 jobs. They join a host of other tech companies that are slashing and burning employees.

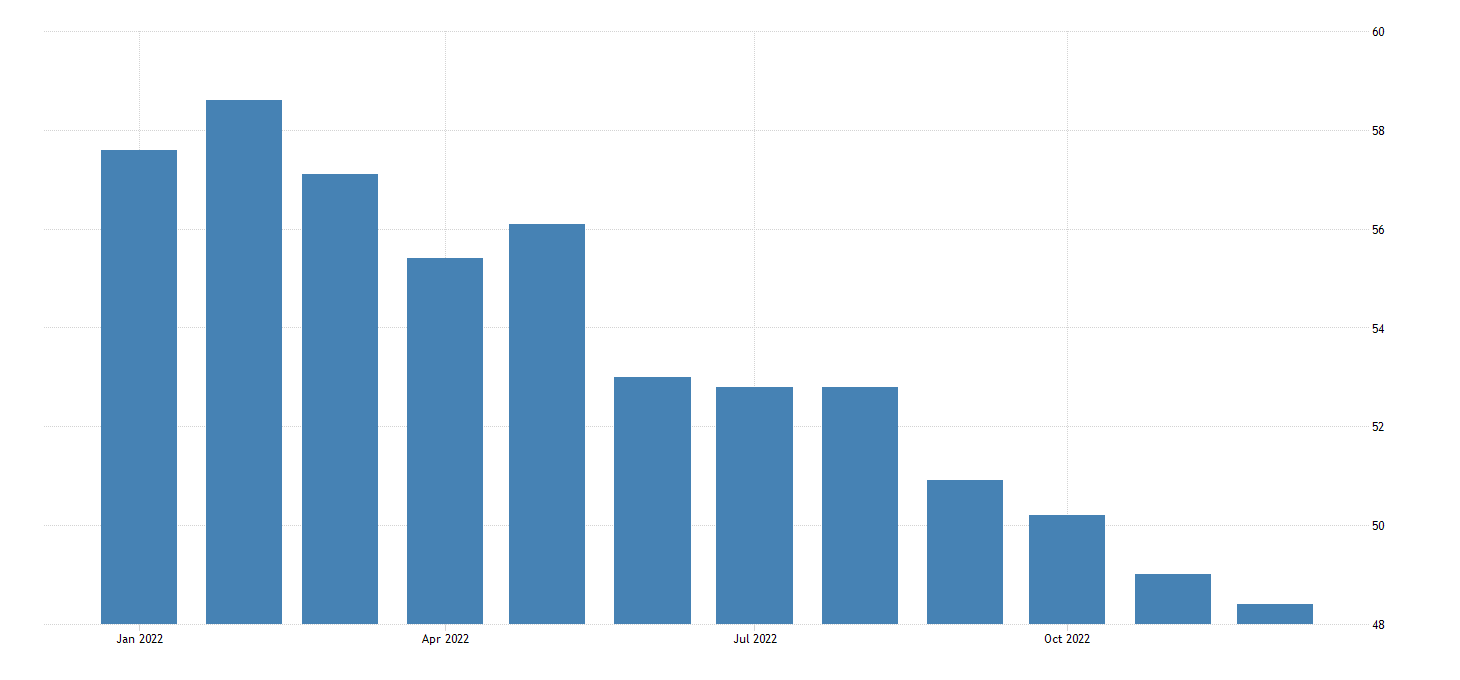

Other macro-data includes mortgage applications, which plunged by 10.3%, and ISM Manufacturing, which came in at 48.4 on Wednesday (contractionary territory and less than estimated).

In fact, Manufacturing has been in a steady decline for months and has not recorded two consecutive months of less than 50%.

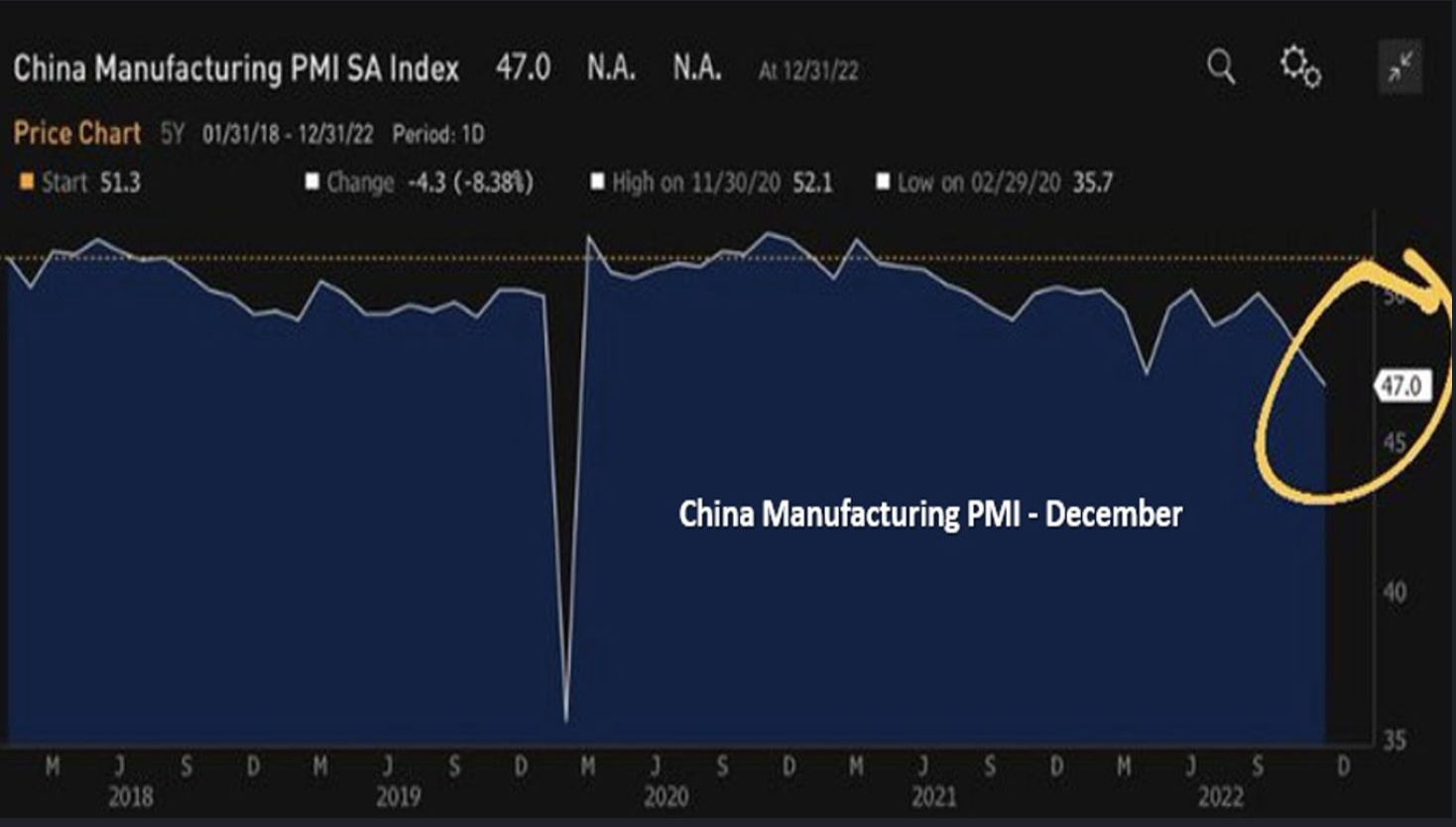

Now, this contraction isn’t just happening in the U.S. but it is also showing elsewhere. Here is a look at the China PMI showing the sharpest contraction in three years.

Now, China has been dealing with a Zero-Covid policy and so this could change if they shift back into growing their economy, but for now, the data is negative.

Additionally, Germany reports that exports fell in November, down 0.3% vs. the expected gain of +0.2%. Imports also dropped by 3.3% much more than the expected decline of 0.5%.

Now, perhaps the surprise will be as to just how deep of a recession we may see.

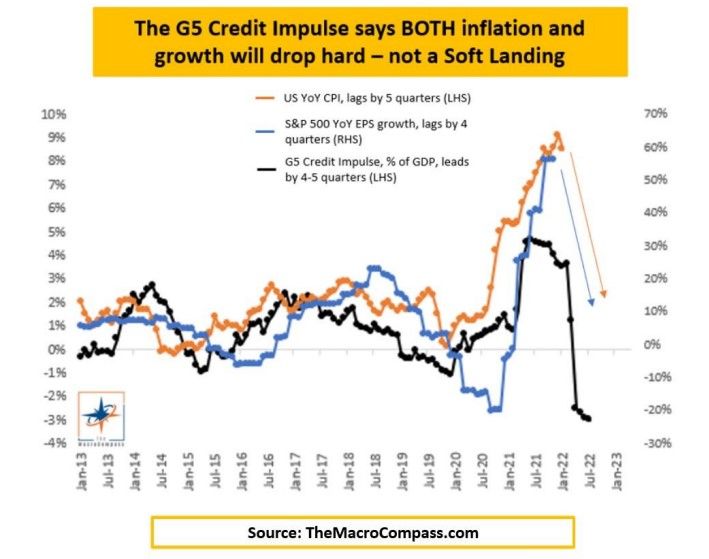

For that, I will point to something I have discussed a time or two in the past – the G5 Credit Impulse.

This index measures the rate of change in the quantity of money (in real terms, as % of GDP) held by the non-financial private sector in the five largest economies in the world. In other words, whether the real spending power of households and corporates is accelerating or decelerating.

As per preliminary October 2022 data, the -3.5% reading is by far the worst in 10 years and in line with the GFC levels.

Why does it lead to growth (earnings used as proxy) and inflation?

Because the more real-economy money creation is available for households and corporates to spend, the more they are likely to boost consumption, and spending and hence push nominal activity up.

Vice versa, if you dry up to the flow of real-economy money creation, it is foreseeable that private sector agents will slow spending and hence nominal growth will drop with a lag.

Where do we stand today?

The TMC Global Credit Impulse index (black, LHS) leads earnings growth (blue, RHS) and inflation (orange, LHS) by 4-6 quarters.

And the chart speaks louder than words: Nominal growth is set to dramatically slow in 2023.

And this is very fitting. Previously, I pointed to how illiquidity would likely become one of the single most important factors for 2023. And the credit impulse is saying this too as the global printing press has come to a sudden halt in 2022, and as a result, we should expect growth and inflation to markedly drop in 2023.

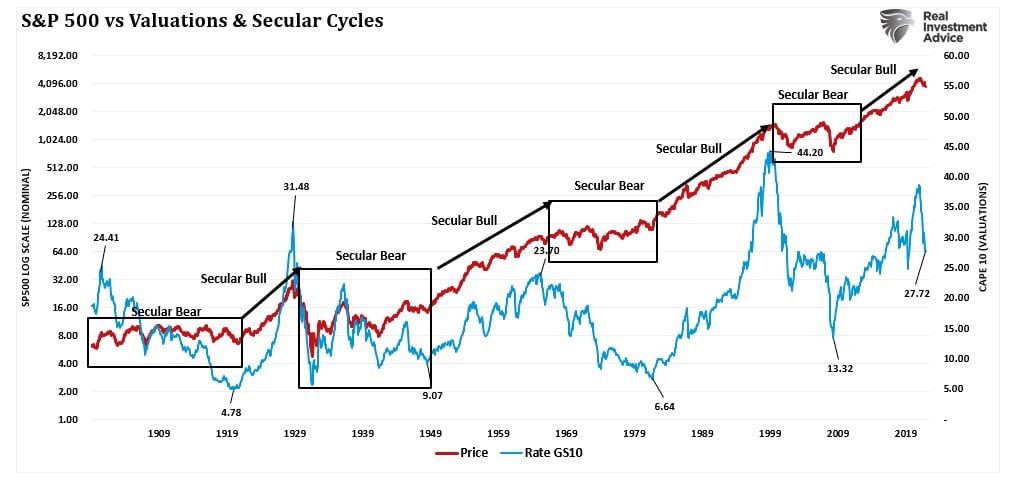

So just how much could this affect the stock market? For that, I will direct you to the following chart.

The chart above shows the history of secular market periods going back to 1871 using data from Dr. Robert Shiller. Notice secular bull markets begin with CAPE valuations around 10x earnings or even less. Secular bear markets tend to start with valuations of 23-25x earnings or greater (over the long-term, valuations do matter.) Most notably, secular bear market periods are defined by near-zero returns during the valuation contraction process.

Notably, 100% of the gains for the index occurred during secular bull markets. Further, secular bull markets are driven by:

- Falling interest rates

- Earnings growth

- P/E expansion

None of those factors are in place today.

And with a contracting credit impulse, it would seem difficult to argue that earnings growth and P/E expansion will be happening any time soon.

It’s not to say that there will not be any opportunities in 2023, but it’s always important to understand what it may look like when most of the pieces of the puzzle are fit together.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.