Related Blogs

April 1, 2022 | Avalon Team

Last week my kids had Spring Break and we visited a theme park. I rode every single roller coaster. I was hurled from 0–50mph in 2.8 seconds, dropped from over 100 feet, and sent upside down and backward at 70mph.

Last week my kids had Spring Break and we visited a theme park. I rode every single roller coaster. I was hurled from 0–50mph in 2.8 seconds, dropped from over 100 feet, and sent upside down and backward at 70mph.

While it made for an exciting vacation, I want my investing experience to be exactly the opposite: boring and predictable.

Too many people fail to consider what happens between the start and the anticipated finish of their investment and end up feeling as though they had been on a theme park ride (but not nearly as fun).

Most investors evaluating a new investment strategy or investment product will look to the historical returns to determine their interest, but not me.

More important than return is understanding the risk that you are taking with an investment because an investment strategy is only good if you’re able to stick with it.

Remember March of 2009? At the exact bottom of the stock market selloff, investors sold over $25 billion in equity funds. The pain of loss had become unbearable. The only relief was to sell.

Of course, we know the rest of the story… the S&P 500 has gone up by nearly 300% since then. But that means nothing for the investors who got thrown off of the bus at the bottom.

Fortunately, there are ways that investors can be smart and never let this happen to them.

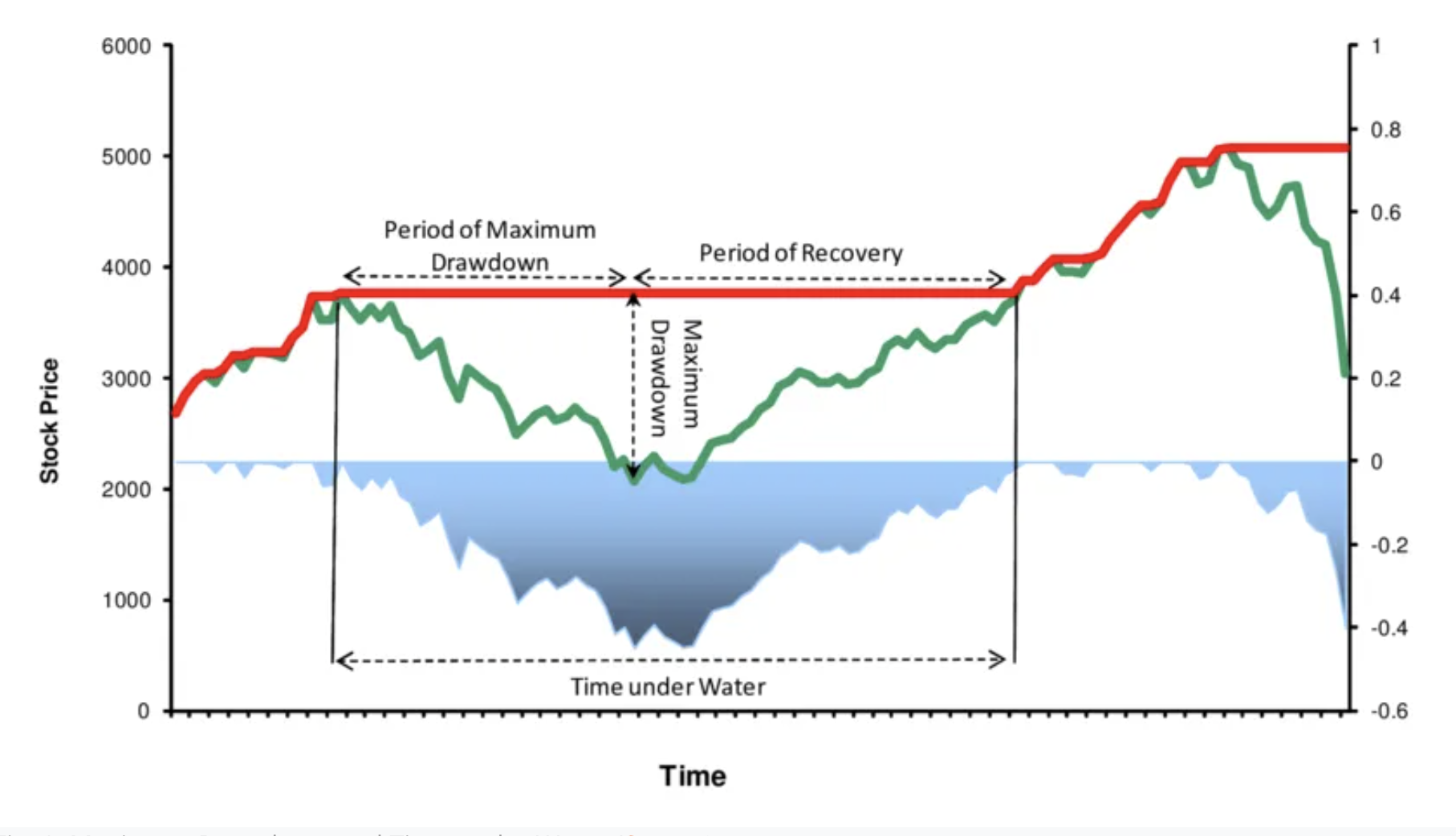

Maximum Drawdown

The first thing that I want to know when I am evaluating an investment strategy is what has been the historical maximum drawdown (MDD)?

No market-based investment goes up in a straight line. They go up. They go down. Sometimes they keep going down before eventually turning back up.

Maximum drawdown measures, in percentage terms, how much from the peak to the low before the investment recovers back to a new high. And it’s a pretty good measure of how likely an investor will be able to stick with an investment strategy.

Let’s consider the S&P 500.

There are a lot of investors who have chosen to buy an index fund and simply hold on.

Understand that this is a “strategy.” And as part of this “strategy” investors are supposed to sit through the entire ride.

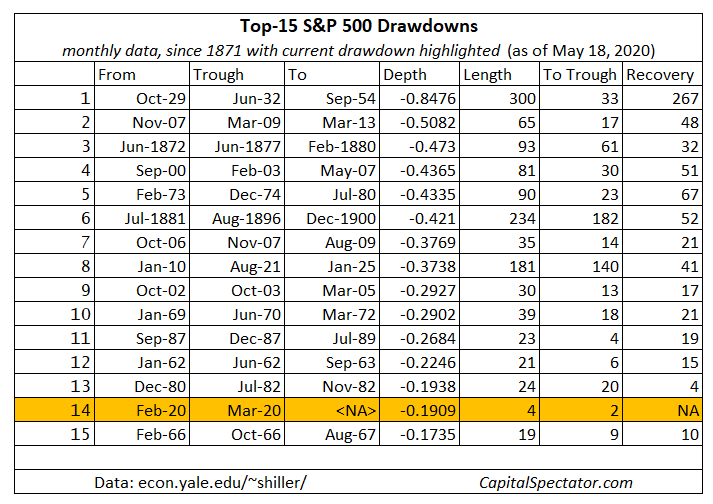

In looking at monthly data, we can see that there have been some doozies of drawdowns in the market’s history.

The Granddaddy of all of them occurred in the Great Depression when the market lost nearly 85% from the peak in October 1929 to the low in June 1932.

The worst drawdown in modern history is the market decline associated with the financial crisis. From November 2007 to March 2009, the S&P 500 lost over 50% of its value.

The drawdown itself is only part of this white knuckle ride. The other part is the length of time that it takes to recover your money.

In the example of the 1929 Crash, investors would need to wait over 22 years before the index would get back to 1929 levels.

That’s a long wait. And while the money was eventually recovered, investors NEVER got back their time.

The Covid decline in 2020 would turn out to be the fastest recovery in history. After ultimately losing 34% over the course of two months, the market fully recovered its losses by August 23.

The crash was unusually severe in a historical context, but the recovery was even more extraordinary. On the previous three occasions when the market has fallen by more than 30%, it has taken nearly three years or longer for losses to be recovered.

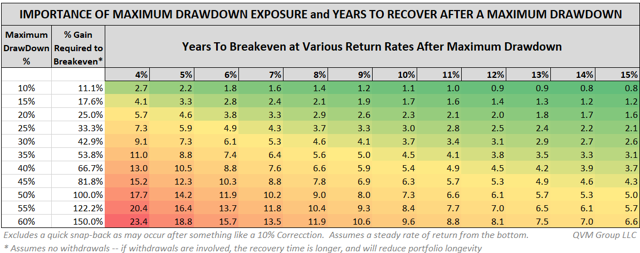

The following table shows the relationship between drawdown and recovery, and this is why keeping drawdowns low and manageable is so important.

Any investment strategy that allows a 50% drawdown to occur, requires a 100% return to get back to even. And who knows how long that can take.

So, Rule #1 is to never invest in a strategy that has large drawdowns. The pain and potential irrecoverable loss of time are simply not worth it.

For my own taste, I find that the vast majority of investors can bear drawdowns of about 20%, but beyond that, emotions begin to kick in.

For some investors, even 20% is too high. The key is to understand where your “too much to bear” pain point is and to never invest in a strategy that has exceeded that.

I prefer investment strategies that actively manage downside risk. Despite the critical importance of this, few investment products and strategies offered to investors actually do.

One example of a strategy that does, is Rowe Wealth’s recently released Volatility-Resistant Investment Model.

The strategy is 100% systematic and includes a very specific rule to make sure that investors never have to endure significant market losses during protracted market declines.

By automatically moving to cash (or cash equivalents) during periods of market losses, the model has a built-in safety net designed to protect investors’ capital.

The results speak for themselves.

By actively managing against them, the strategy’s largest drawdown is slightly over -12% (and that is inclusive of a maximum management fee).

And because downside risk is managed, the recovery time from losses occurs faster resulting in a greater compound of capital.

So forget the Wall Street misinformation that you must accept higher risks to earn higher returns. It’s is simply not true if risks are actively managed.

By beginning with a “risk-first” approach to investing, investors will find that the returns will take care of themselves.

Tune in next time when we’ll discuss a few other important risk metrics to help assure that your investments are performing as well as they can be.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.