Related Blogs

January 19, 2023 | Avalon Team

This week, the Commerce Department released a number of data series that were HIGHLY recessionary. Retail Sales clocked in at -1.1% month-over-month, Industrial Production came in at -0.7% month-over-month, and Manufacturing Production registered -1.3% month-over-month.

We just saw one of the worst two-month declines in retail sales since the Global Financial Crisis and the covid lockdowns – and with consumer debt at all-time highs, we don’t anticipate this trend changing anytime soon.

Furthermore, the Fed holdings of US Treasury notes and bonds just fell by the largest amount in history. So what has been a big prop for asset prices is being removed.

Now, if you take all of this to conclude that 2023 may be another bumpy ride, you probably are not too far off.

With the possibility of a recession ever looming, investors may be looking for ways to manage the uncertainty.

In the world of investing, diversification is often touted as a way to manage risk in a portfolio.

The idea is by investing in a variety of asset classes, such as stocks, bonds, and real estate, an investor can spread their risk and reduce the impact of any one investment on their overall portfolio.

However, during times of economic crisis, the correlation between asset classes often increases, meaning that they all tend to move in the same direction. This can lead to diversification failing as a risk management strategy.

One of the main reasons that diversification can fail as a risk management strategy is that correlation between asset classes often increases.

First, a quick primer on what correlation is:

- If asset class A rises by 10% and asset class B also rises by 10%, they have a perfect correlation of 1.

- If asset class A rises by 10% and asset class B doesn’t move at all, they have no correlation.

- If asset class A rises by 10% and asset class B falls by 10%, they have a perfect negative correlation of -1.

Here is the big problem. Correlations are NOT static. They can and DO change.

What investors are not being told is that during market declines, correlations increase.

At that EXACT point, you NEED correlations to be negative, they break down.

Let’s go through a couple of examples.

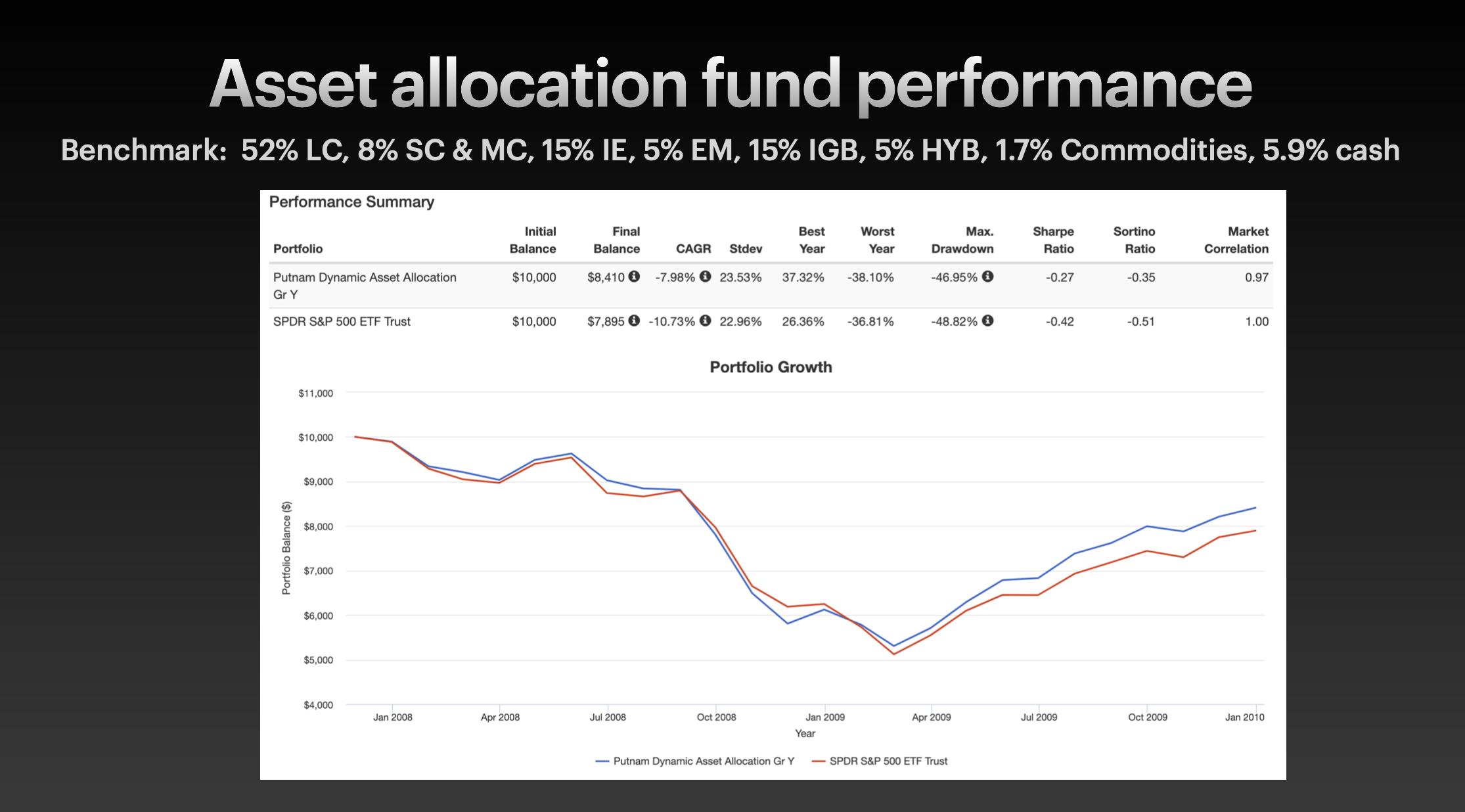

We begin with a traditional asset allocation portfolio, strategically allocated across large caps, mid-caps, small-caps, international equities, commodities, and real estate.

During the Great Financial Crisis, the U.S. stock market as measured by the S&P 500 Index fell by over 50% at its worse point.

There was little difference between the performance of the asset allocation fund and the general market.

Why is that? Isn’t diversification supposed to help?

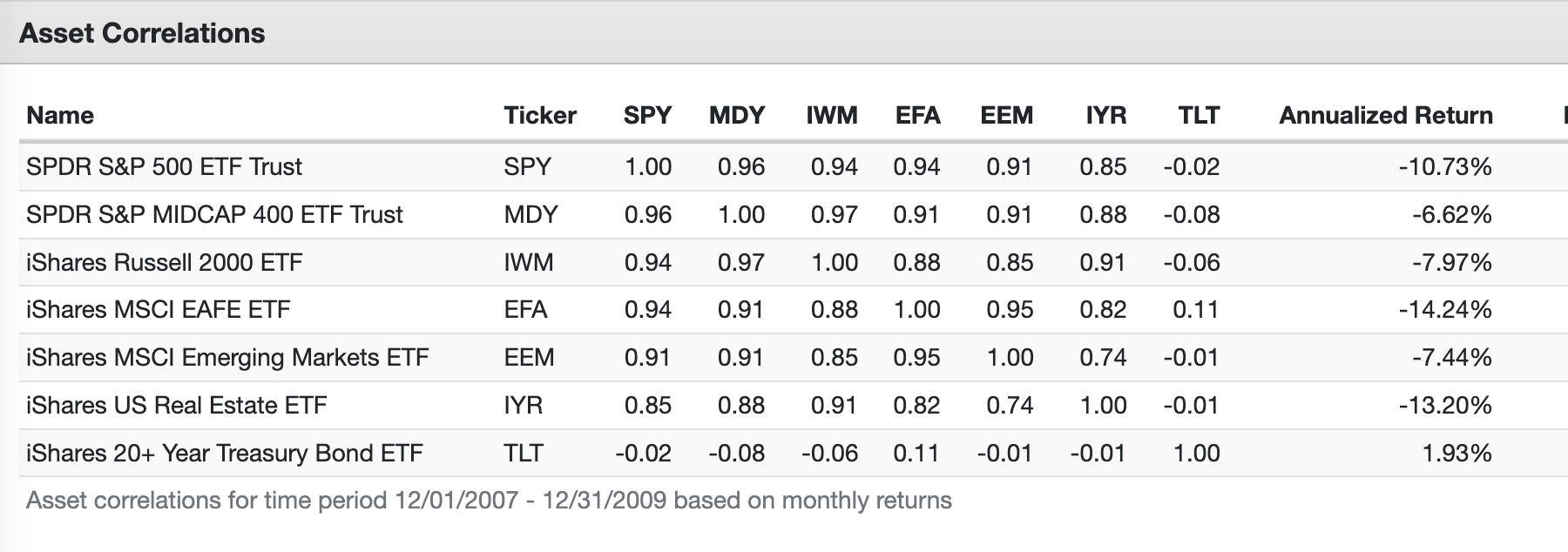

The answer lies in this table, arranged to show how each asset class compares to another on the basis of correlation.

Notice that nearly every asset class shows a correlation of .80 or higher. This explains why there was little performance difference between the “diversified” portfolio.

In this period, bonds did, however, provide some protection.

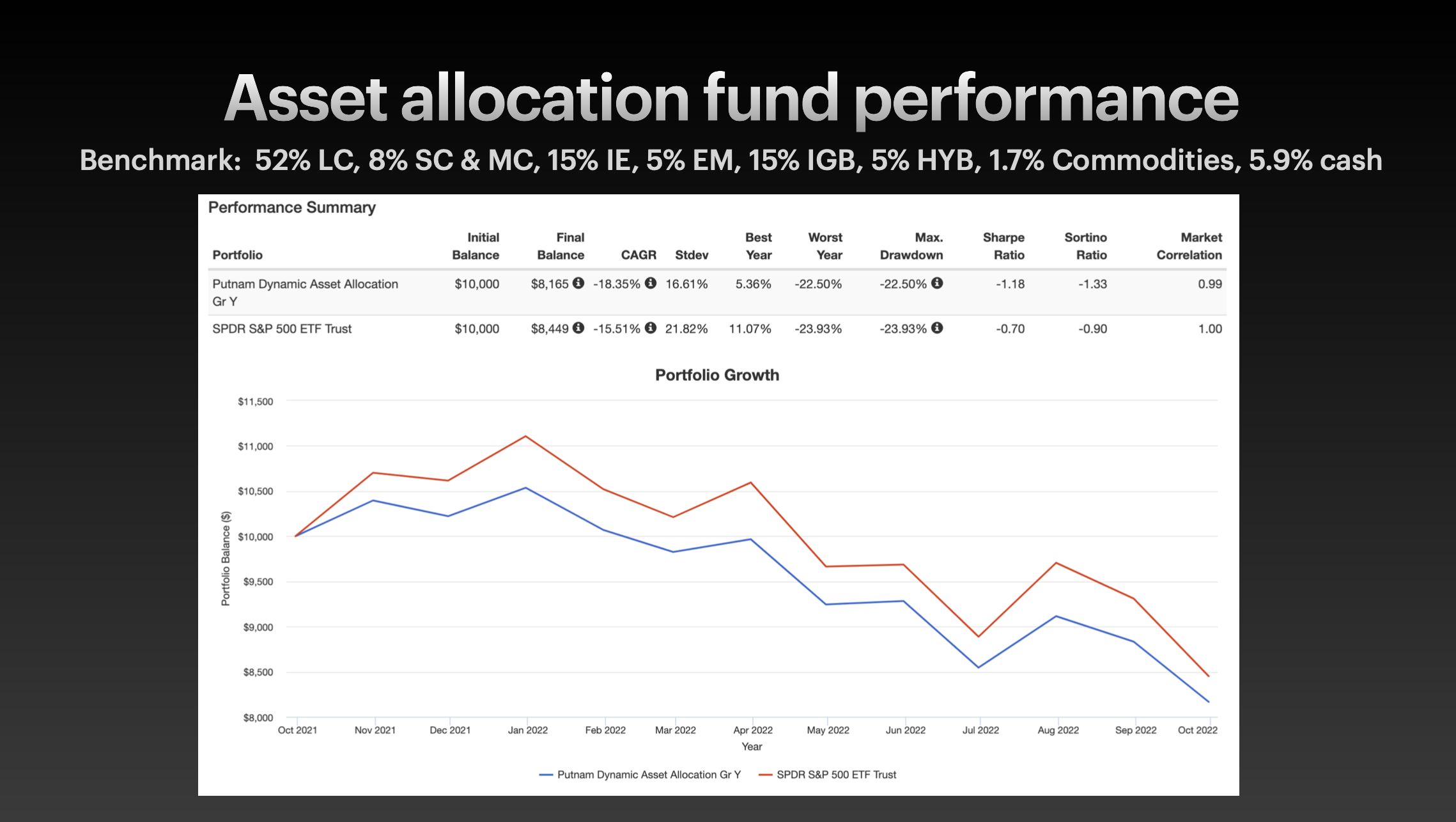

With 2022 still fresh in investors’ minds, let’s look at the same data.

It turns out in fact, that last year was even worse as the “diversified” portfolio returned less that the S&P 500.

Why? Simple. Bonds, often thought to mitigate risk in a portfolio, actually increased the risk.

And again, the correlation among the various securities remained high, with bonds now the worst-performing asset class.

If you still aren’t convinced, here’s another example to consider.

Target date funds are among the most popular choices in 401k plans. For many plans, they are the default choice because of the favorable view toward “diversified” portfolios.

But here again, the numbers come up short as the Target Date example performed worse than the S&P 500.

Do you see the benefit of diversification? No? I don’t either.

If the goal of diversification is to minimize downside risk, it seems to be failing in living up to its promise.

The key to diversification is not the number of assets you own, but the lack of correlation among the assets you do own.

The legendary Fidelity manager, Peter Lynch, called it “diworseification” and maybe for good reason.

There are better ways to manage downside risk… but that is a story for another day.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.