Related Blogs

December 29, 2022 | Avalon Team

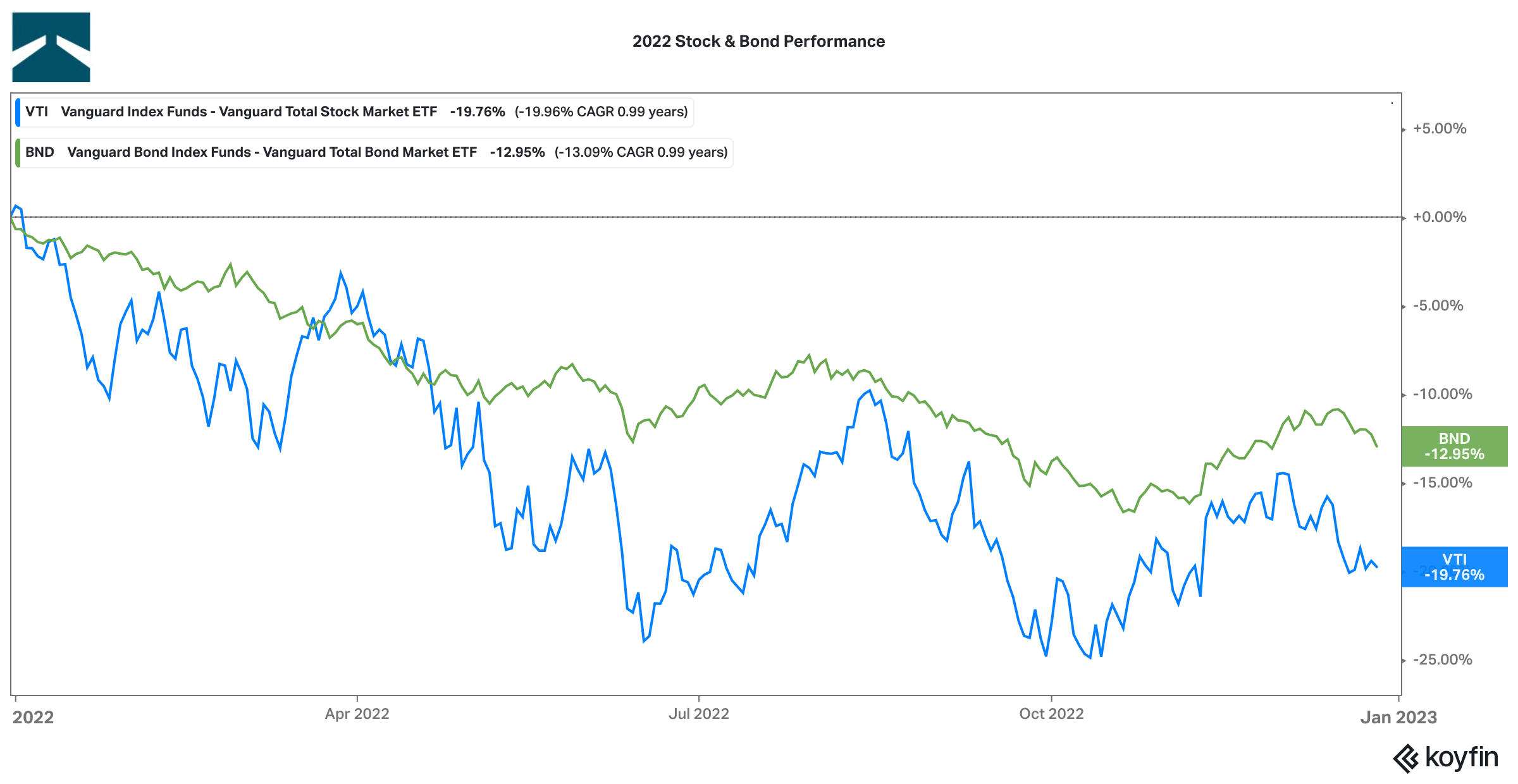

2022 will be remembered as one of the worst years ever for a portfolio of stocks and bonds. Stocks and bonds both fell by double digits.

It’s rare for stocks and bonds to fall in the same year.

By my calculations, it’s happened just four times before this year going back to 1928.

But in that time, they have never each fallen 10% or worse in the same year.

Now, this was not a complete surprise to me.

Earlier this year I pointed out how record-high stock valuations coupled with record-low bond yields, would lead to a period of sub-par performance for traditional stock and bond portfolios.

The one surprise to me was just how quickly this forecast manifested itself.

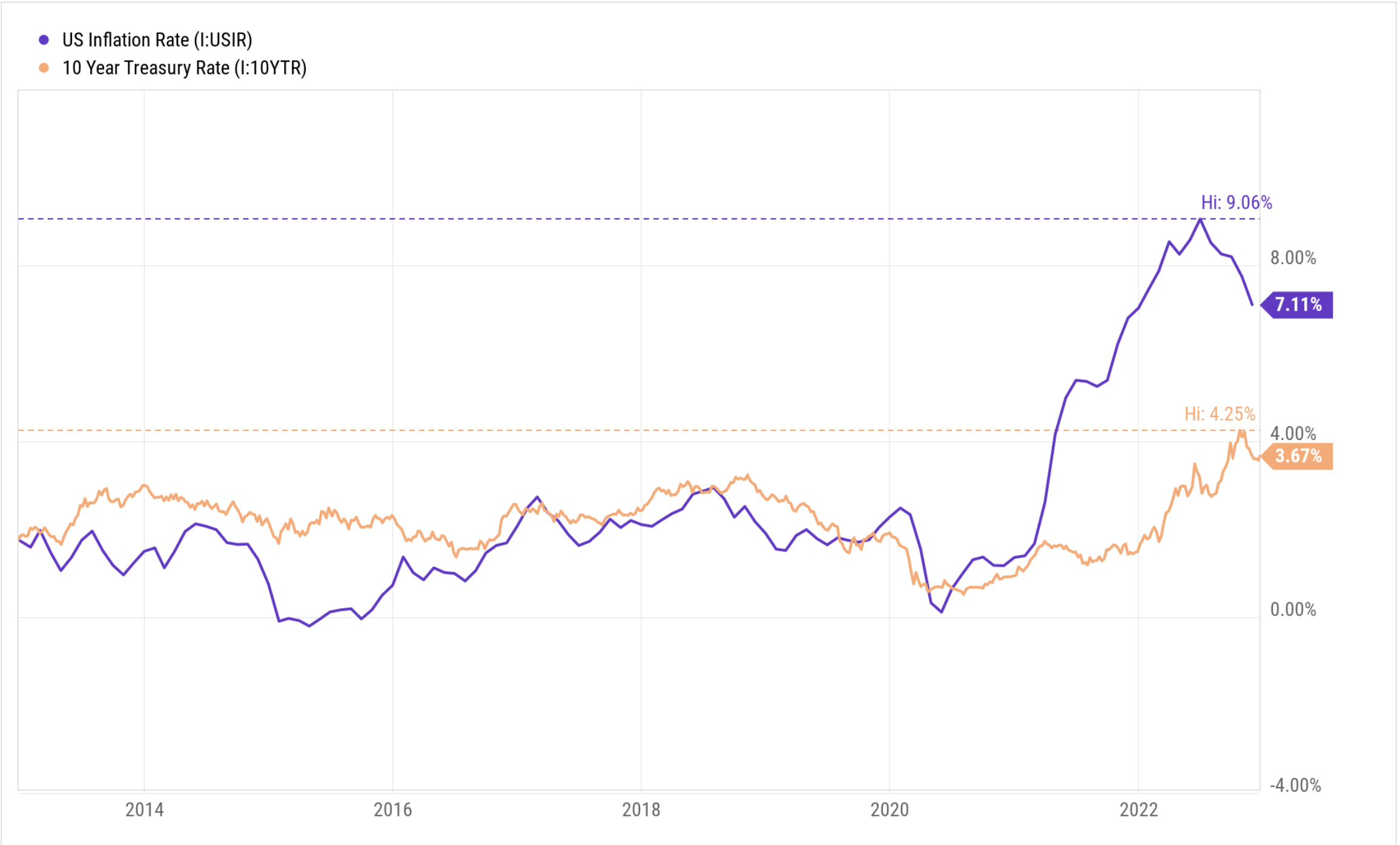

The rapid rise in inflation and interest rates was the obvious catalyst, but the speed by which the Fed increased interest rates (and continues to) was the real clincher.

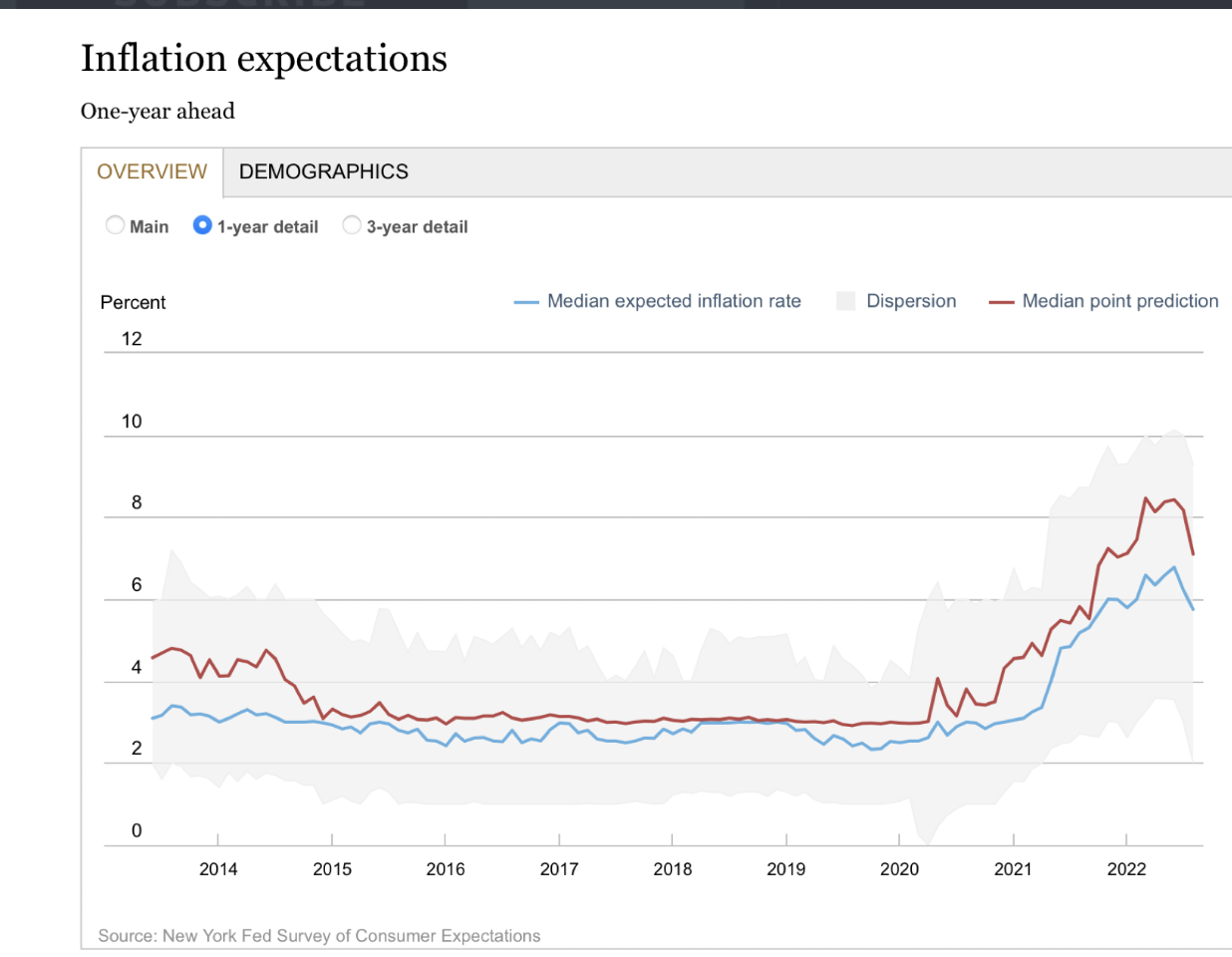

To many investors, consumers, and businesses, inflation in 2021 and 2022 has been shocking because a decade of low and stable inflation lulled them into complacency and left them unprepared.

While the inflation numbers flashed red in 2021, expectations for future inflation were slow to adjust. In 2022, survey results show a climb in inflation expectations as consumers react to hits to their pocketbooks.

The last year has proven to be one of the most rapidly evolving economic and financial market environments in history.

Across the globe, central banks have responded with coordinated monetary policy changes that have outpaced anything we’ve seen for several decades.

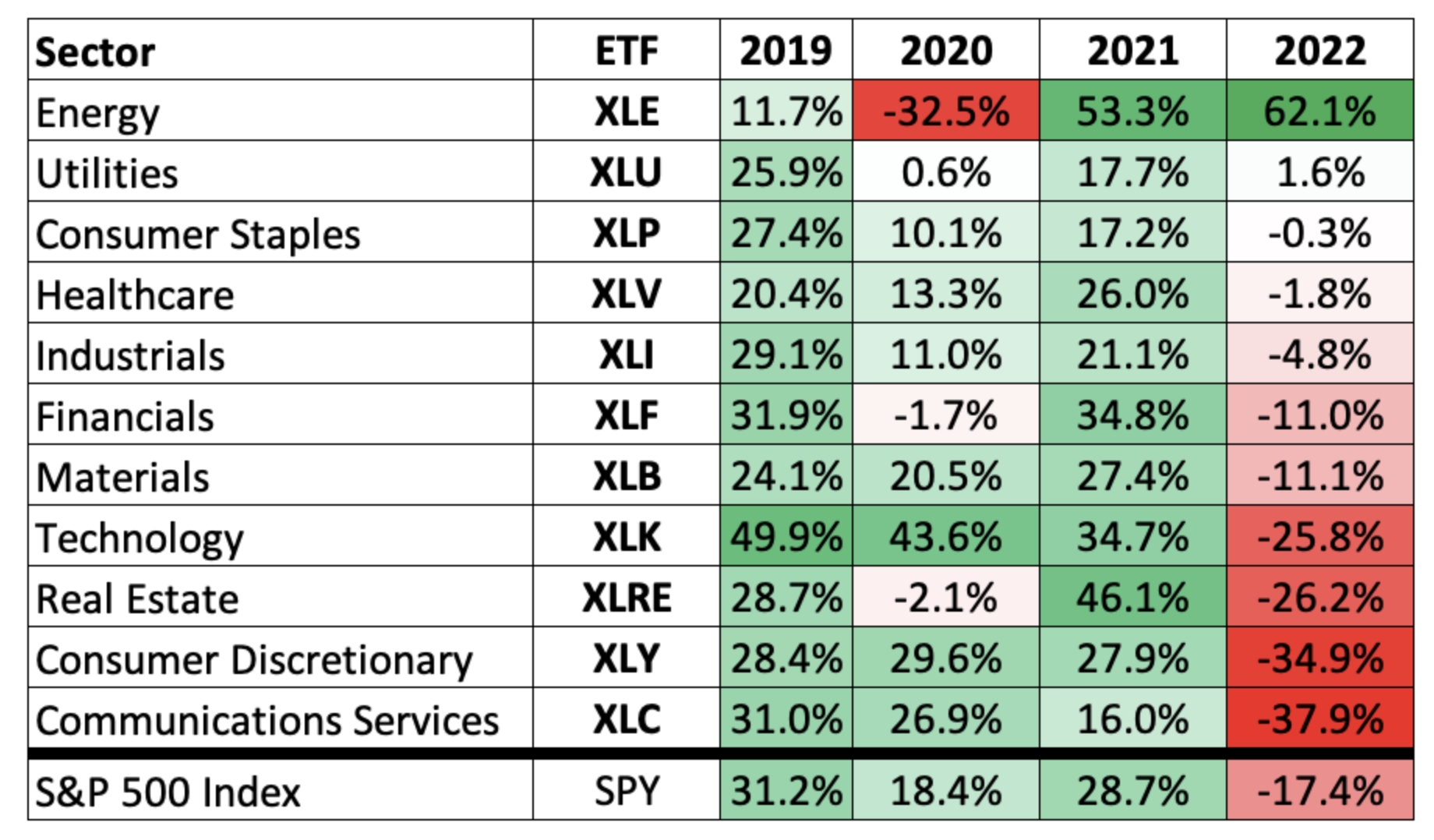

The impact across the market can be easily seen in the one-year performance heat map of the S&P 500.

Large rotation into industrials, consumer staples, and energy sectors is the story of 2022.

U.S. tech stocks had a rough year with the Nasdaq down -33% (its fourth-worst year in its 52-year history).

But if we take a step back and look beyond the Nasdaq, the falling out with tech really started in 2021 as small-cap, software, electric vehicles, and to some extent meme stocks, took a beating.

It was in 2022 that the pain finally came forwards to tech giants like Apple, Amazon, Microsoft, etc, with the giants down -41.6% in 2022.

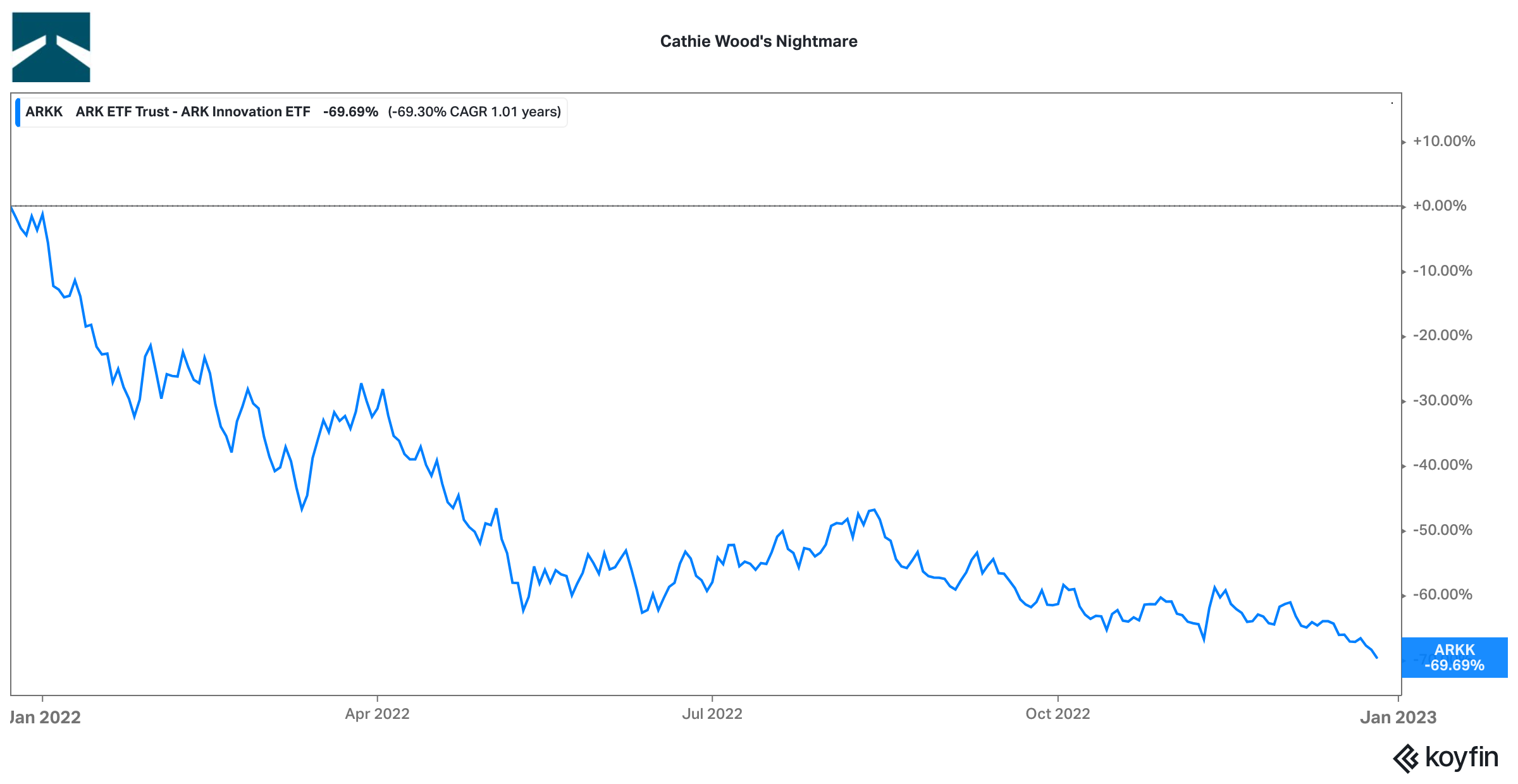

Just take Cathie Wood’s ARK Innovation Fund. At its peak, the fund had more than $28B in assets under management. Now, after last year’s nearly 70% loss, the fund’s assets have fallen to just a little over $6B.

This was on the heels of 2021’s loss of 23.5%.

There’s no better example of why risk management and stop losses should be used than this cautionary tale.

Sector Scorecard

The SPDR S&P 500 exchange-traded fund (ETF), SPY, is facing its worst year since the financial crisis of 2008, which saw a drop of nearly 37%. Contextually, SPY’s 17.4% drop this year sounds far less drastic. A deeper dive shows where the losses are concentrated within the index, specifically with four sectors down more than 20% each.

For all of 2022, only two sectors have positive performance: Energy and Utilities. Communications Services, Consumer Discretionary, Real Estate, and Technology were the worst-performing sectors.

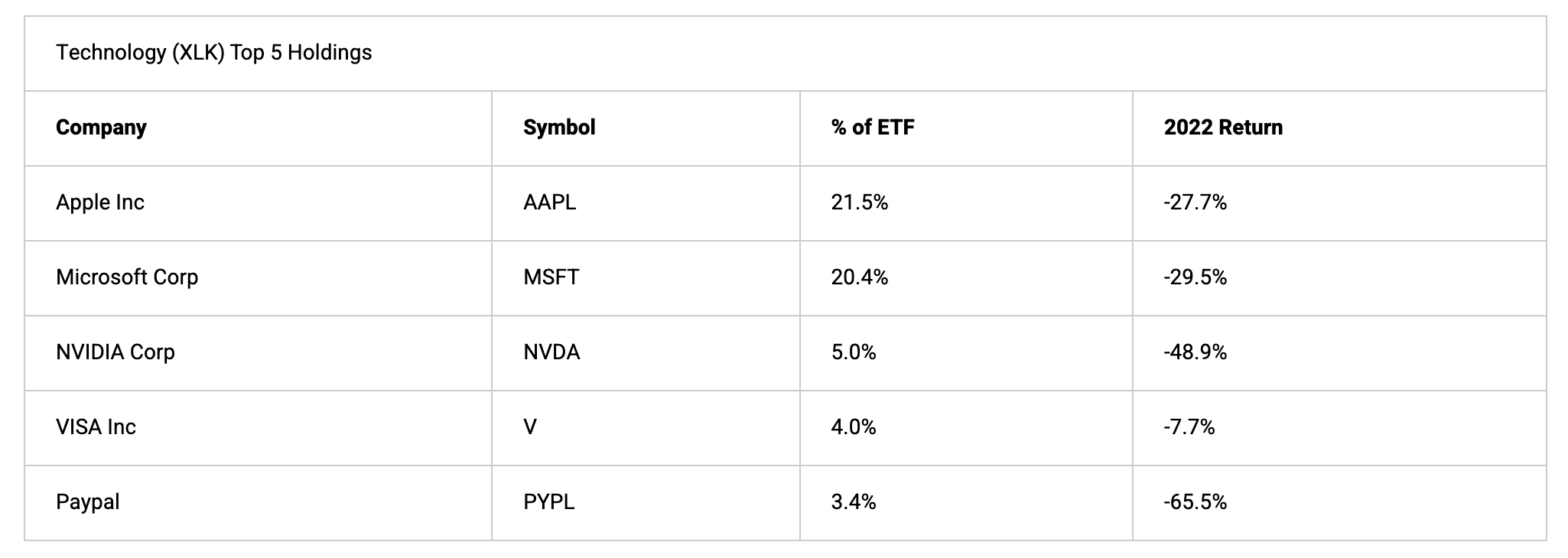

After being a dominant force for multiple years, the technology sector now faces a 25% loss as 2022 ends. XLK, the SPDR Technology Sector ETF, contains the two largest components of the overall index, with Apple (AAPL) and Microsoft (MSFT) comprising over 41% of the ETF. XLK itself represents over 25% of the S&P 500, thanks to the holdings in AAPL and MSFT.

The losses in these two stocks represent a sizeable amount of the negative performance for the overall index.

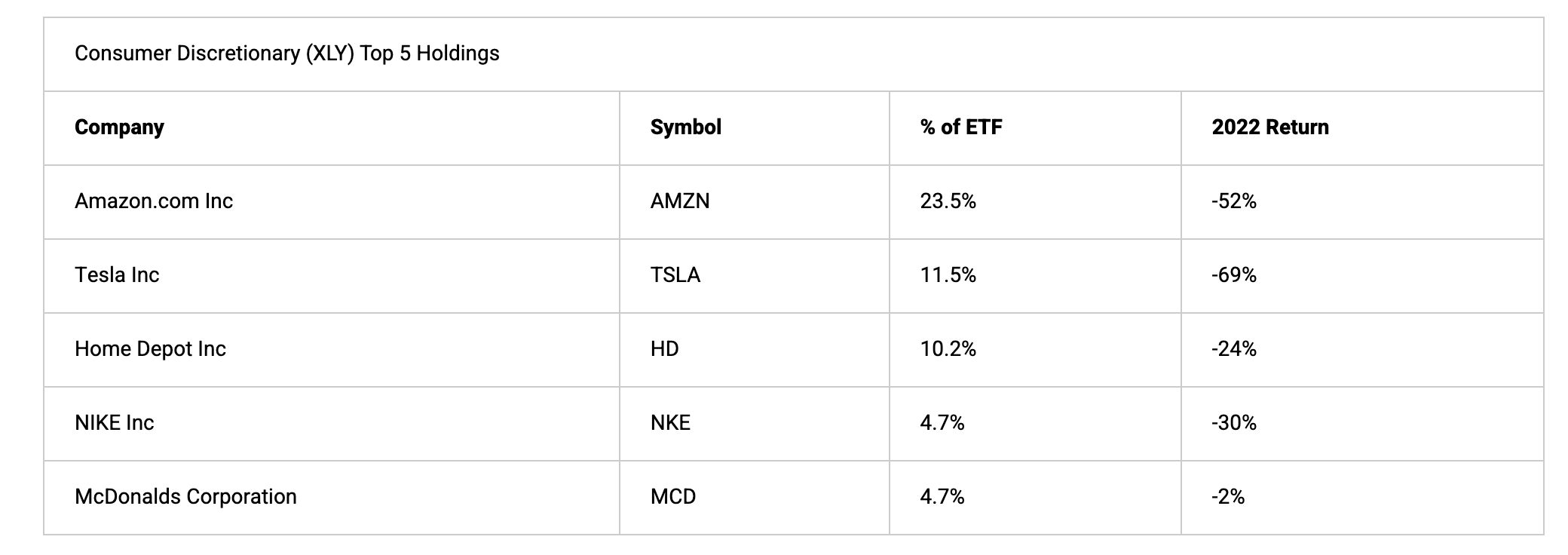

With constant discussions of recession and the continued battle with inflation, it’s no surprise that the consumer discretionary sector is struggling this year. The SPDR Consumer Discretionary ETF (XLY) is now down nearly 35% for the year, with its two largest holdings paving the way lower. Amazon (AMZN) has lost over 50% of its value since January, with shares of Tesla (TSLA) down almost 70% for the year.

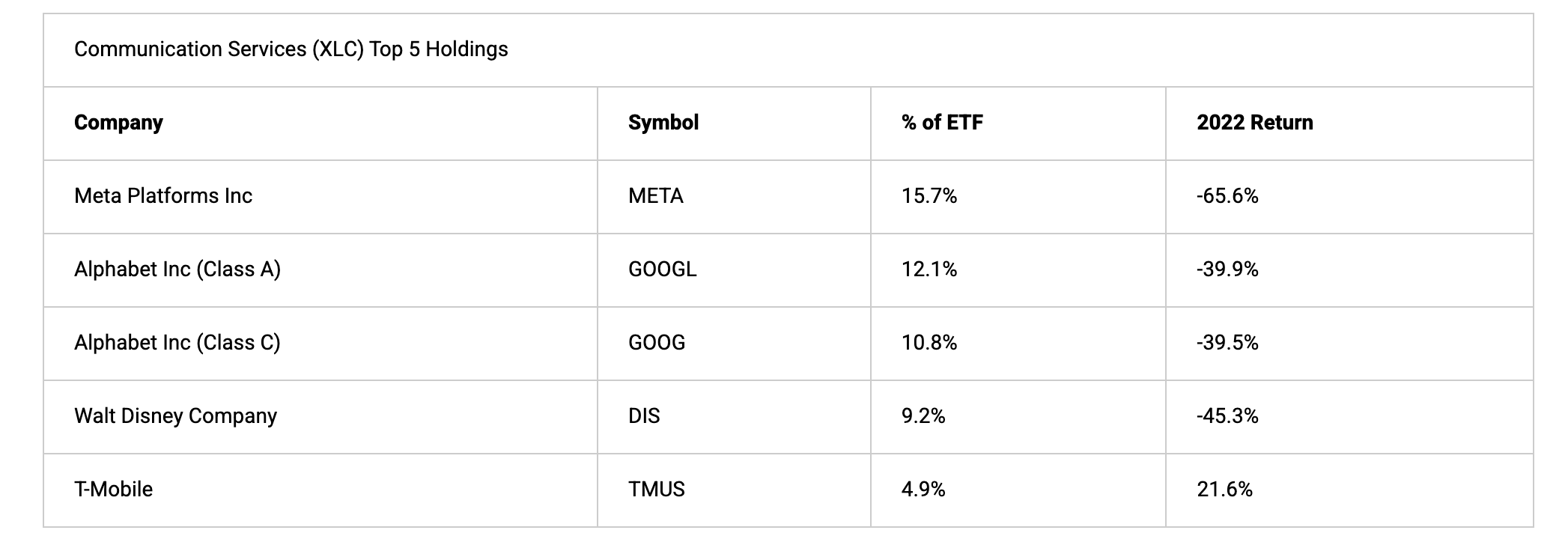

The worst-performing sector for 2022 is communication services. Looking at the holdings of XLC, the SPDR Communication Services ETF, it’s no surprise.

The top three holdings are Meta Platforms (formerly Facebook) (META) and the two share classes of Alphabet (GOOG & GOOGL), the parent company of Google.

While most investors may think of these firms as tech giants, their classification and inclusion are in the communication services sector.

Like the overall market, XLC saw strong returns over the past three years before 2022.

2023 Outlook

Although forecasts are a popular Wall Street pastime during this time of year, forecasts are a fool’s folly. For readers hoping for some type of forecast for the New Year, I don’t do forecasts.

The future is unknown. Period. End of story.

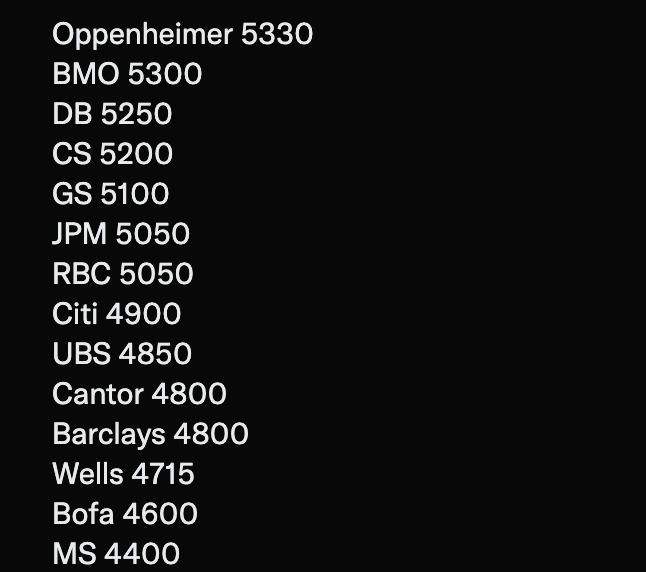

Here is how the Wall Street geniuses fared with their forecast for 2022:

As I write this, the S&P 500 is trading at 3808. See how well that worked out?

Top analysts with hundreds of hours of research couldn’t even get it close enough for a birdie putt.

For this reason, I manage money using an adaptive process. As market conditions change, so does my portfolio.

I don’t need to know the future. I simply adapt to the change as it takes place.

I think it is far more important to focus on what IS controllable, such as drawdown objectives and risk management.

Having a “predictable process” to manage the unpredictable future is the only way to manage money in my humble opinion.

For example, during 2022, as stocks and bonds have been negative, my portfolios have been heavily invested in cash or trend-following strategies that can participate profitably regardless of market direction.

Having said that, I will take a look at some of the macro factors that I think will continue to play a role in investors’ portfolios as we move into 2023.

1. Central Banks remain hawkish and interest rates remain high.

In the past few weeks, we have heard from Chairman Powell and the ECB, and the Bank of Japan (BoJ) abandoned years of artificial price control and raised the 10-year ceiling to 50bp from 25bps. Central banks are determined to reduce inflation and are not afraid to raise interest rates to do so.

The last time we had inflation this high in the 1970s and 1980s, government bond yields and inflation generally tracked one another fairly closely. But now, interest rates remain well below the inflation rate.

Additionally, China is getting looser on its Zero Covid Policy. This is going to make it harder for the Fed, as demand for energy and other commodities by China may limit the declines seen within inflation.

So with this as the backdrop, I believe that interest rates will likely remain high.

I do not think that the 2% target inflation rate set by the Fed is achievable and as a result, inflation will remain persistent, albeit at more modest levels.

The end result is that it will be very difficult for the Fed to pivot barring a complete economic collapse.

2. Valuations are “fair” but not cheap.

That type of environment is generally negative for stocks and bonds, particularly tech stocks as tech companies like to borrow money at low costs.

So unless inflation weakens substantially, this will not be the time yet to buy technology.

I see continued weakness in the weight of the FAANGMs tying the indexes down. As I wrote about last week, Apple (AAPL) has recently broken down and continues to trend lower. Same with Tesla (TSLA).

Even with the declines in stocks, the market is not necessarily “inexpensive” in terms of valuations.

Saxo Markets Hong Kong Chief Investment Officer Steen Jakobsen recently highlighted to CNBC that he believes 75% of the market is CHEAP and 25% is still very EXPENSIVE.

The expensive stocks are the FAANGs (Meta, Apple, Amazon, Apple, Netflix, and Alphabet) and other pure technology-driven platforms (e.g. Uber, Airbnb, etc.).

Although valuations have rolled back in tech stocks, both the Nasdaq and FAANG stocks have a PE ratio of ~26x.

Definitely back to pre-covid levels which are somewhat ‘fair’ but can’t be considered cheap yet for investors to pile back in.

Costs and revenue are likely still a concern looking ahead. When looking at recent tech earnings both costs and revenue should have set off some alarm bells.

Although they scaled back costs with a lot of aggressive layoffs and restructuring, the last quarter showed a number of tech giants really struggled to control their costs.

Meta has gone from the highest free cash flow in its history in Q4 2021 (US$12.7B) to the lowest in more than 10 years only three quarters later (basically zero) as Mark Zuckerberg is betting everything on the Metaverse.

Revenue via online advertising sales is down across the board as budgets are cut and this is also hitting companies like tech companies hard.

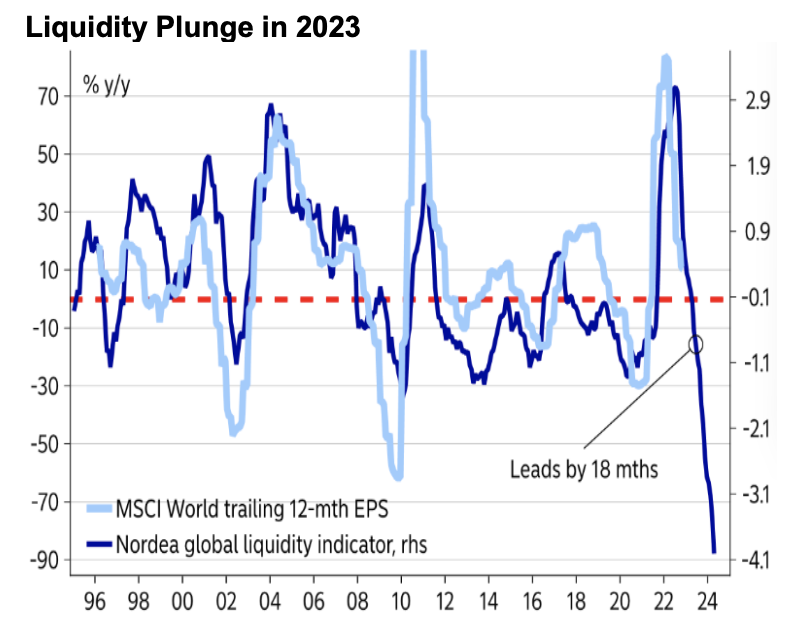

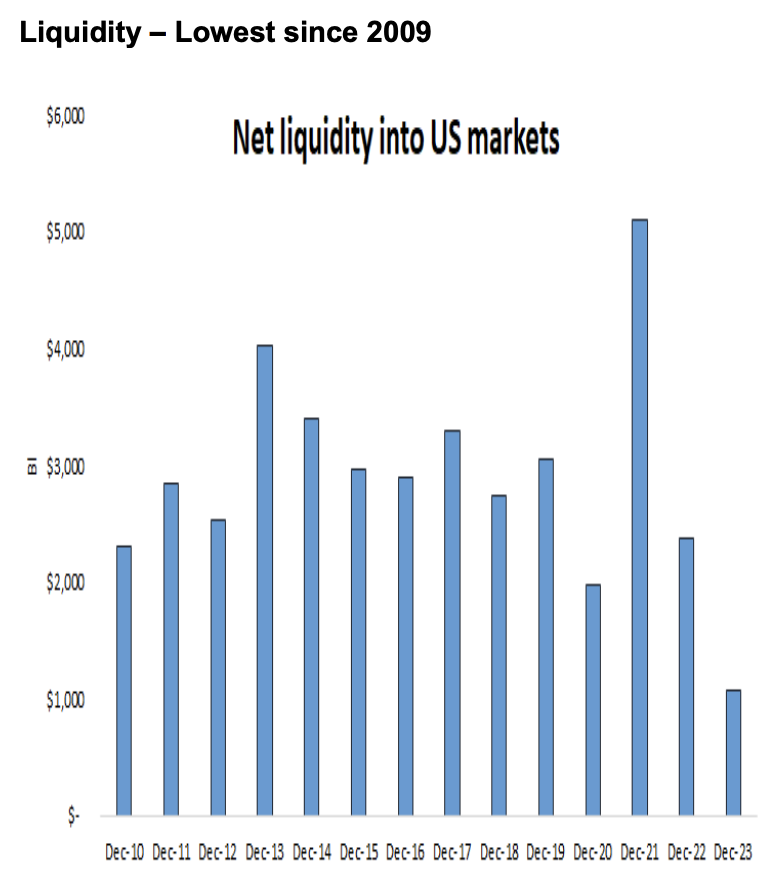

3. Global liquidity will turn extremely negative next year.

While global central banks turned hawkish one after another in 2022, the effect on liquidity will only start next year. The Fed announced the passive roll-off of the balance sheet in early 2022 but began very cautiously in the summer.

On top of that, the entire QT was more than offset by the drawdown of the TGA balance by the Treasury department. Therefore, the net impact on liquidity from the Fed’s QT has been negligible so far.

The US runs a structural account deficit with the rest of the world, and in return, the rest of the world must run a capital account deficit with the US. As such, a little less than $1T of capital flows back into the US via the capital account.

The government is a drain on liquidity, as it issues trillions of dollars of debt each year to finance its structural budget deficit.

Liquidity has been flowing into the US market in recent years, which of course ends up in both stocks and bonds. Nevertheless, liquidity will reach its lowest level since 2009, and this assumes that M&A activity and buybacks stay at the current level. It also assumes that the budget deficit remains at roughly the same level, which is a challenge with the passage of the $1.66T omnibus spending bill passed this week.

At this same time, China wants to grow the consumer sector and no longer just be the factory of the world. China also wants to reduce its exposure to the US dollar. This means more consumer spending and a lower trade surplus with the US while clearing more trade in bilateral currency transactions.

The end result will be a further reduction in liquidity for the US. and the need for further deficits to make up for any shortfalls.

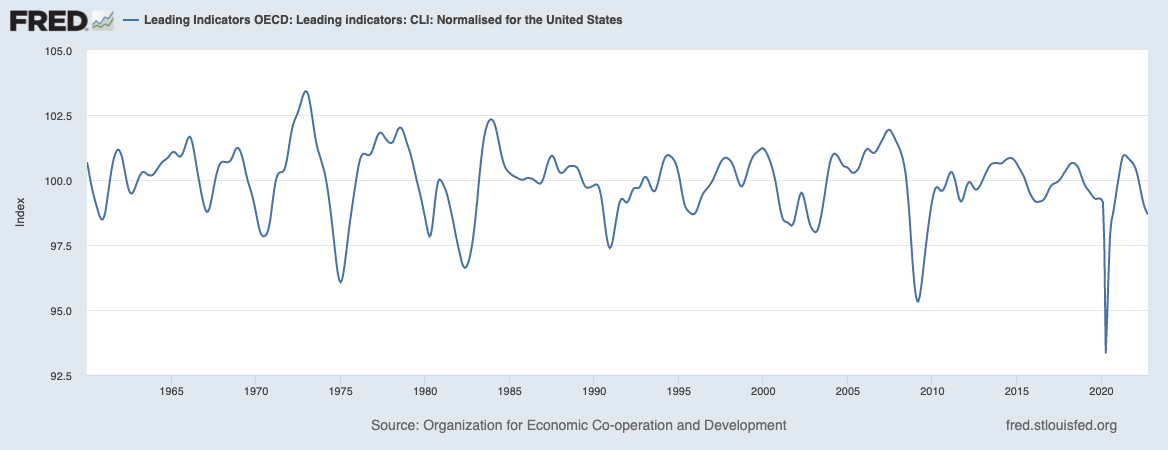

4. Leading indicators point to a recession.

The leading indicator index was published this week and flashes bright red. The indicator is now decisively in recession territory, reaching the lowest level since April 2020 when the US was in full lockdown.

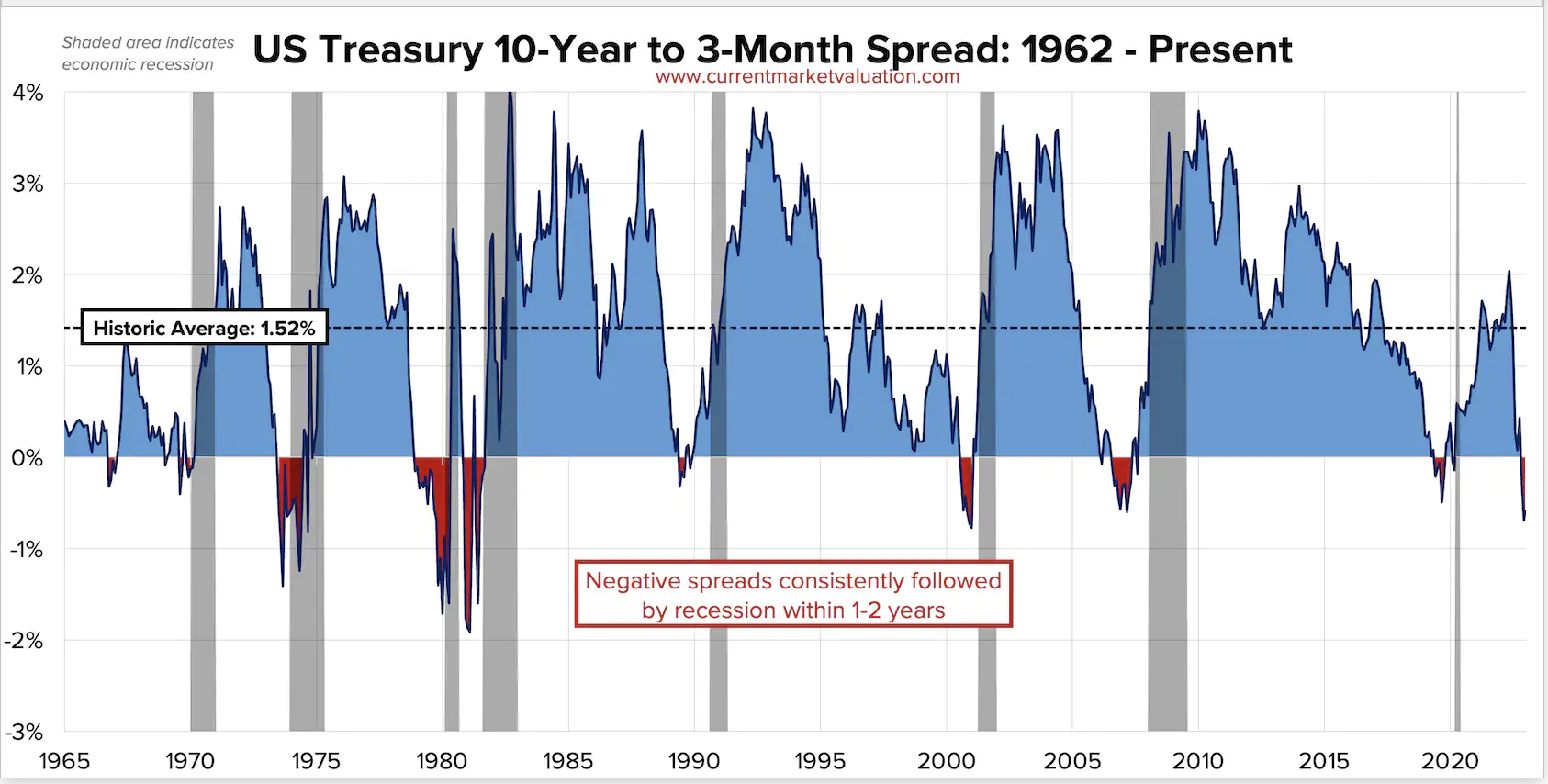

Add to this, the US Treasury Yield Curve is currently inverted, meaning short-term interest rates are moving up, closer to (or higher than) long-term rates. This unusual occurrence, called a yield curve inversion, has historically been a very reliable indicator of an upcoming economic recession.

Finally, another hint of recession comes from the relative performance of regional banks versus consumer staples.

Over the last year, regional banks are underperforming the consumer staples sector by close to 18%, which is something you only see prior to recessions. The KRE is pricing in commercial real estate, auto loans, and residential mortgage risk.

Conclusions

While I do believe that the markets will remain especially challenging for many investors, I do see opportunities for investors willing to step away from traditional asset allocation models and explore alternative investment opportunities.

We’ll start looking into those next week as we kick off the New Year.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.