Related Blogs

June 2, 2022 | Avalon Team

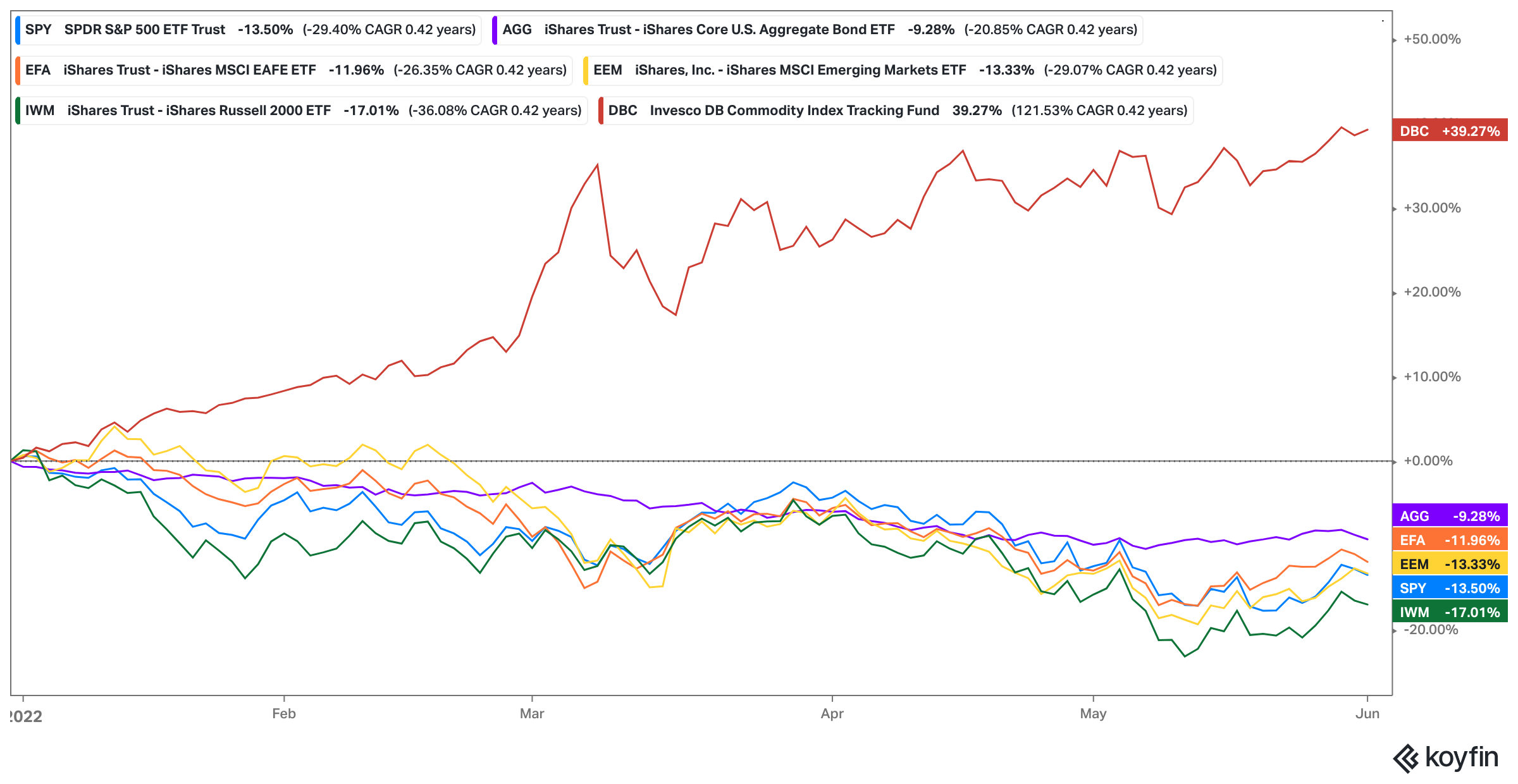

No question about it, this has been a challenging year for investors.

Most asset classes continue to post negative returns.

Between April and May, investors saw the S&P 500 post seven consecutive weekly declines before staging a rally last week.

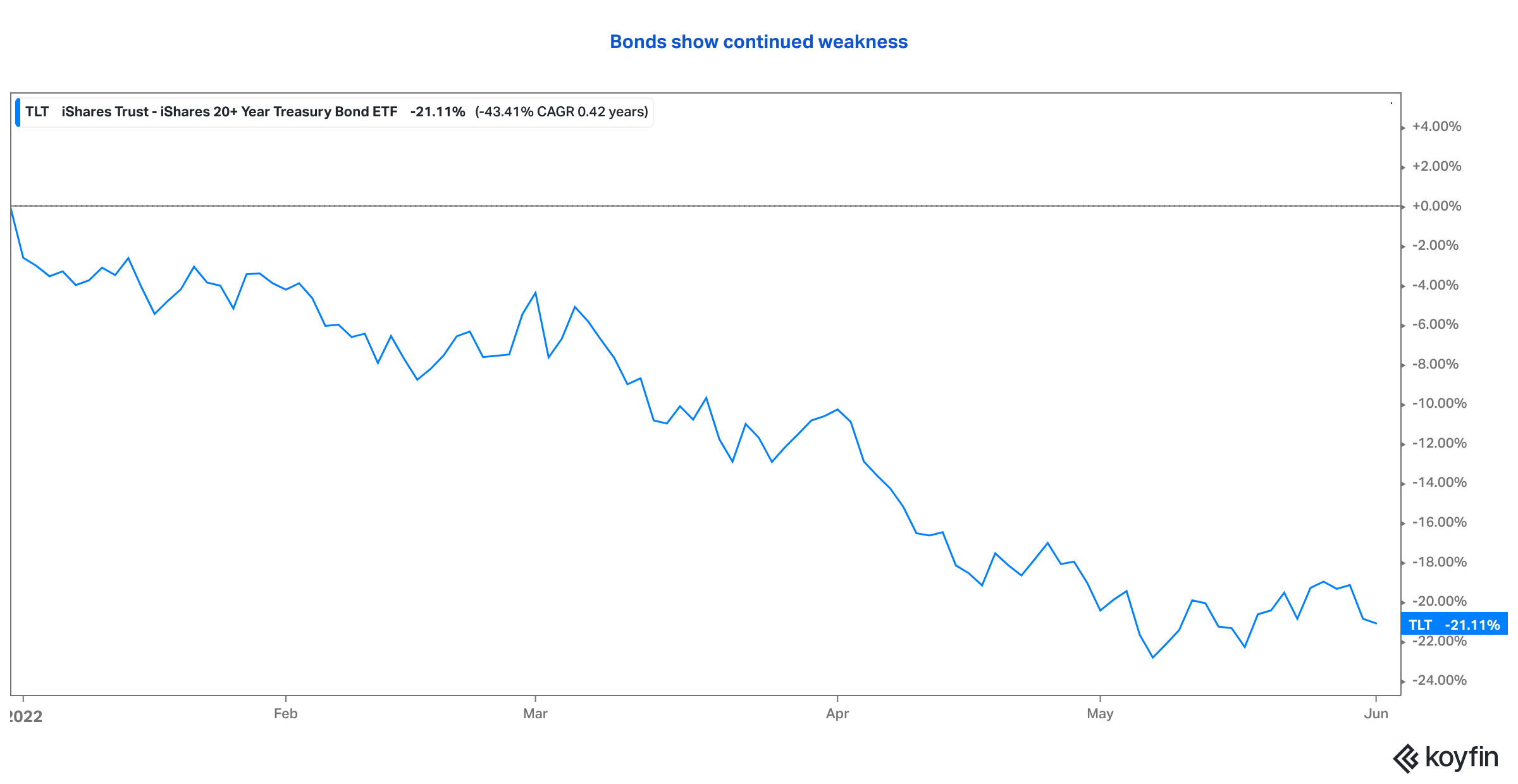

Noticeably missing is the customary positive returns that bonds often provide during periods of stock market weakness.

Indeed, long-term treasuries have posted the worst return of all major asset classes.

In my series of articles “The Death of 60/40,” I warned investors of this very thing.

Stretched valuations for both stocks and bonds implied that future returns would be much less than what investors had come to expect during the past decade.

The catalyst for declines has been, of course, the rapid surge in inflation and the anticipated monetary actions by the FED to bring inflation under control.

Despite the challenges posed by this more hostile investing environment, there are solutions – investors can achieve positive returns by using a technique known as “return stacking.”

And, I want to stress, that this is not just theory. It is the very same approach I have taken with Rowe Wealth Management’s new Adaptive CORE strategies.

This new series of models are designed to provide consistent returns in all kinds of market environments.

Take a look at the Adaptive Diversified Growth strategy.

For some background, I will cite the Dragon Portfolio from “The Allegory of the Hawk and Serpent: How to Grow and Protect Wealth for 100 Years.”

The essence of the paper is that a portfolio must be constructed to withstand a variety of economic regimes and be able to prosper during periods of secular growth and secular declines. The Dragon Portfolio’s key strength is its adaptability to most imaginable market scenarios

Many investors continue to invest with portfolio allocations that would be fine in disinflationary, falling interest rates, and reasonable valuation environments, none of which are consistent with today’s environment.

The essence of return stacking is to reduce the exposure to stocks and bonds to accommodate non-traditional assets that are non-correlated, but that also have the ability to efficiently add a stream of return while reducing overall risks.

The monthly returns in the above model show a remarkable level of consistency, despite the various curve balls that are being thrown at the financial markets. Most importantly, the downside risk has been kept to a minimum with a Maximum Drawdown of only -4.18%.

How to Build a Return-Stacked Portfolio

At the core of each model is a flexible, diversified strategy that is intended to be consistent with an investor’s goals.

Each strategy is designed for investors who want to preserve exposure to traditional stocks and bonds while bolstering expected returns with non-correlated return streams like trend following, global macro, and tail-hedging strategies.

For example, in the Adaptive Conservative Model, the core blends four different strategies that can invest in bonds, REITs, dividend-paying stocks, and alternative income products such as closed-end funds or income partnerships.

Depending upon the market environment, these strategies can range from being fully invested to 100% cash. The “stacking” takes place by adding additional holdings to the core.

In my article, “How to Build an All-Weather Portfolio,” I discussed the advantages of using managed futures as an important portfolio diversifier. In my return stacked portfolios, managed futures are the first product I reach for in constructing the new models.

Check out the table below for this year’s monthly returns for the Standpoint Multi-Asset Fund, one of the two products I use for this alternative asset class. This has added positive returns during the tumultuous months of February through May.

Managed-futures products can provide exposure to a variety of investments that are simply not found in traditional stock and bond portfolios, such as commodities and currencies, as this list of underlying sectors shows.

- Domestic and International Equities

- Grains, Meats, and Soft Commodities

- Metals and Energy

- Global Currencies

- International Bonds and Interest Rates

- U.S. Treasuries and Investment Grade Fixed Income

And with the ability to profit from either long or short exposures, managed futures are trend agnostic, making them an ideal portfolio diversification tool.

Moreover, decades of established research provide strong economic reasoning for their continued efficacy in providing both absolute return and structural diversification.

Additional portfolio diversifiers in a “stacked” portfolio can be used to mitigate known risks. For example, with the Fed on a course of monetary tightening, perhaps for some time to come, there is the obvious risk of continued weakness in bonds.

Fortunately for investors, there are new and innovative products that can easily be allocated to offset such risks and even provide an additional source of positive return.

One such product is the FolioBeyond Rising Rates ETF (RISR). This ETF invests in interest-only mortgage securities that benefit from rising interest rates. At the same time, these types of securities can effectively shorten the duration of a traditional bond portfolio.

Unlike traditional hedging strategies such as shorting or buying puts, IO-mortgage securities currently pay an interest rate of 3-4%. And unlike other fixed-income products, these will typically appreciate in a rising interest rate environment.

You read that correctly – RISR is up 29.24% YTD!

By utilizing a flexible core process, and through the judicious use of alternative products, it is entirely possible to construct a portfolio that is capable of navigating financial storms.

Where the rubber hits the road is demonstrated in the risk metrics of the aforementioned ADAPTIVE Diversified Growth strategy.

The risk-adjusted return, as demonstrated by the Sharpe Ratio, is about 3X better than the traditional 60/40 portfolio with much less downside risk.

You can have more returns with less risk when you intelligently stack your returns with the correct alternatives.

For investors who manage their own money, hopefully, this article has inspired you to begin your own exploration of stacked returns.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.