Related Blogs

November 14, 2023 | Avalon Team

♫ Market goin’ nowhere, Mr. Powell help me

Somebody help me, yeah

Market goin’ nowhere, inflation help me, yeah

I’m stayin’ alive ♪

-inspired by Staying Alive, the Bee Gees

The lyrics of the catchy Bee Gees disco anthem, Staying Alive, conveyed a sense of resilience and determination in the face of challenge.

We can say the same about the U.S. stock market as measured by both the S&P 500 and the Nasdaq 100.

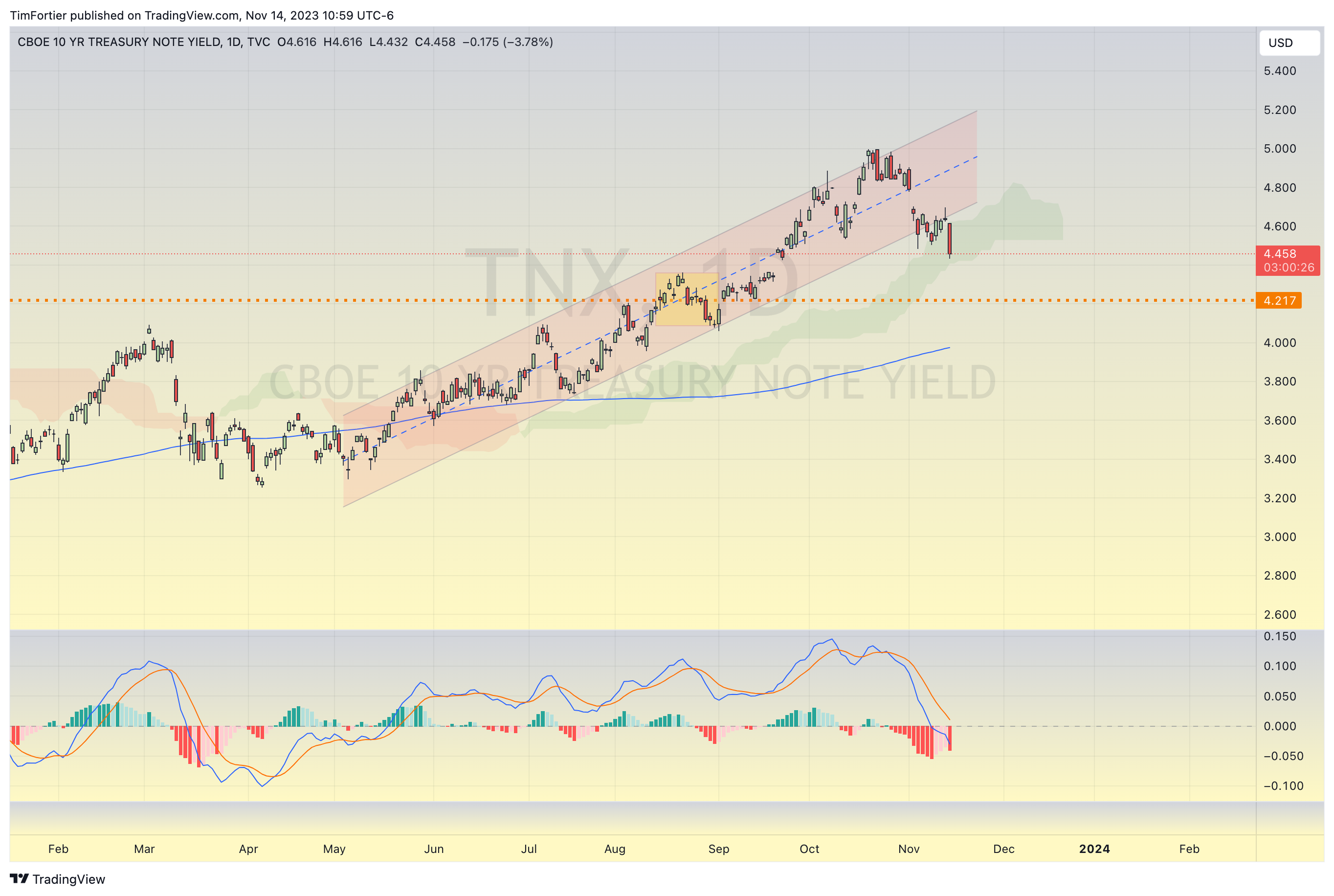

At the end of October, the S&P breached its 200-day moving average as the U.S. Ten Year Note yielded nearly 5%.

That looked challenging for stock market bulls.

As I stated in my commentary last week, things have quickly changed.

Last week marked the return of a trend we’ve seen all throughout 2023 – the domination of mega-cap growth and tech.

And today’s miss on CPI is adding more fuel to the fire.

Let’s start with the CPI.

Following two months of hotter-than-expected prints (driven by surging energy prices and healthcare methodology changes), the October CPI print was expected to slow materially from the previous month (from 3.7% to 3.3% on the headline) even if the core was expected to remain unchanged at 4.1%.

What we got, however, was a whopper, with CPI missing across the board with both headline and core prints coming in below expectations on both a sequential and annual basis.

This has sent yields plummeting and stocks soaring.

First, the Ten-Year is all the way back to 4.45%, representing a decline of over 50bps from its recent high.

Until today, yields had been clinging to the rising trend channel, but today’s break creates a lower low, and thus, by definition, rates have started to trend lower.

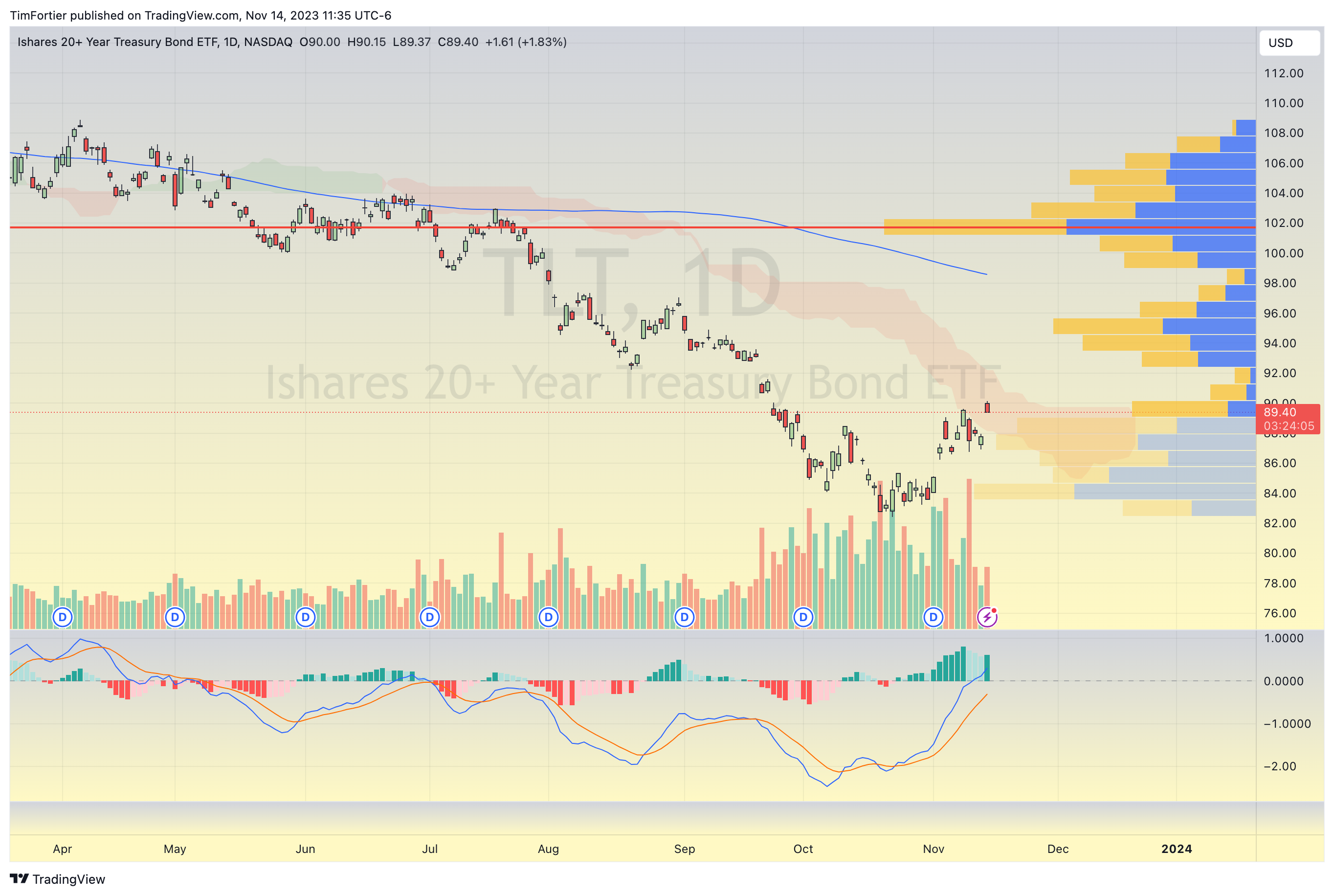

The long end of the curve has also responded positively, although less forcefully.

I am not that surprised that the 30-year treasury is having a more muted reaction.

In recent weeks, I have been asking, “What if interest rates are no longer being driven by the level of inflation and the economy in general? What if interest rates were increasing for all the “wrong reasons?”

What could be a “wrong reason?”

The out-of-control deficit and the required massive supply of bonds that is and will continue to be needed to be sold is one such example.

Back in mid-October, the Treasury auction for 30-year bonds was a disaster, sending yields to their highest level since 2007.

Primary dealers had to buy 18.2% of the auction, signaling poor investor demand.

The sagging demand resulted in a 16bps rise in rates, the single largest daily jump since March 2020.

This past week, the Treasury tried it again.

Complete disaster is how it was described.

Foreign bidders tumbled to 60.1%, the lowest since November 2021.

This time, dealers were forced to step in and buy a whopping 24.7% of the issue, about double the average.

Yikes!

I can’t entirely agree with the notion that bond yields are purely reflective of expectations for economic growth and inflation.

Economics 101 says that more supply with less demand results in falling prices.

When bond prices fall, yields rise.

Let’s not forget just three months after Fitch downgraded the U.S.’s credit rating, Moody’s is in line to be next on the list.

After Friday’s market close Moody’s downgraded U.S. Treasury Debt to a negative outlook.

Moody’s remains the only rating agency — part of the Big 3 with S&P and Fitch — that now maintains a AAA rating on the United States.

The rating agency cited the “nation’s diminished fiscal strength, undone by extreme partisanship in Washington,” according to CNN Business.

The market has shrugged this off but one point remains true.

U.S. government debt is no longer the world’s risk-free benchmark.

For evidence of this, consider that the risk premium for Emerging Market bonds and U.S. Treasuries is now the same.

This could be the result of a changing perception of U.S. debt.

It may be why we continue to see the BRICs continue to sell off U.S. treasury debt.

For instance, this is China’s holdings over the last decade:

So as a percentage of total U.S. debt, this is massive because right now, total U.S. debt is $33.7T, and China’s holdings sit around $875Bn for a percentage of total U.S. debt holding of 2.5%.

In contrast, this same nominal holding back in 2010 would account for 5.8% of the total outstanding.

So, while the United States has increased its debt by 2.25x, China has reduced its holdings by 2.3x percentage-wise.

So who picks up the slack? Why the U.S. Federal Reserve, of course.

Back in 2010, the Federal Reserve’s total U.S. treasuries owned was $777Bn.

Fast forward to today, and that figure is now $4.87T, an increase of 6.26x.

The problem with this is obvious: this is inflation via debasement; the more debt the U.S. treasury issues, the more money (credit) the Federal Reserve has to create to absorb it.

This is the source of our inflation, and it’s nothing more than masking the atrocious U.S. government spending problem and lack of fiscal responsibility.

So, while I would love to celebrate today’s decline in inflation, I remain concerned that the more significant culprit to our inflation woes is only worsening.

Further, if the decline in CPI also implies recessionary/deflationary forces may be at hand, that will only worsen the situation for the Federal government as tax revenues will also decline when interest costs on the Federal debt are rising.

But none of this seems to matter at the moment.

For now, stocks remain in rally mode.

The S&P has very clearly broken above the trend channel that has been guiding prices lower since the summer high.

Potentially, as prices have retraced .78% of the decline with today’s thrust higher, the one remaining bearish scenario would require an imminent reversal.

The fact that volume has been declining on the rally from the late October low does support a more cautious view, but market internals such as bullish percents remain positive.

Additionally, the percentage of stocks above the 50-day moving average is now above 50%, making this a much healthier market.

So, it’s best not to fight the tape for now as stocks are “staying alive” with some welcomed rate relief.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.