Related Blogs

September 20, 2023 | Avalon Team

Whatever the Federal Reserve’s current and future decisions are regarding interest rates, it’s an important reminder that the Fed only controls the direction of short-term interest rates. The market controls the longer end of the curve.

U.S. Treasury bond yields are a function of three factors: term premium, inflation, and economic growth expectations.

Term premium, also called term premia, is the amount by which the yield of a long-term bond exceeds the expected yields of short-term bonds. Currently, longer-term bonds yield less than short-term bonds, so the term premium is negative.

This implies that buyers of long-term bonds believe that short-term rates will be below long-term rates in the future, which is likely true with all things being equal.

After all, statistical means project GDP to average only 1.65% over the next ten years (stock investors take note!) and inflation has been coming down from where it peaked last June.

However, my growing concern is that context is a critical fourth factor that traditional methods fail to recognize.

I continue to focus on 10-year rates as they remain persistent in trading at new cycle highs.

10-year rates are extremely important as this is the bond used to determine mortgage rates as well as pricing all longer-duration assets (tech stocks).

Thus, the higher this rate climbs, the more potential damage to the economy this is going to cause.

The trouble with bonds is that debt is becoming a real problem.

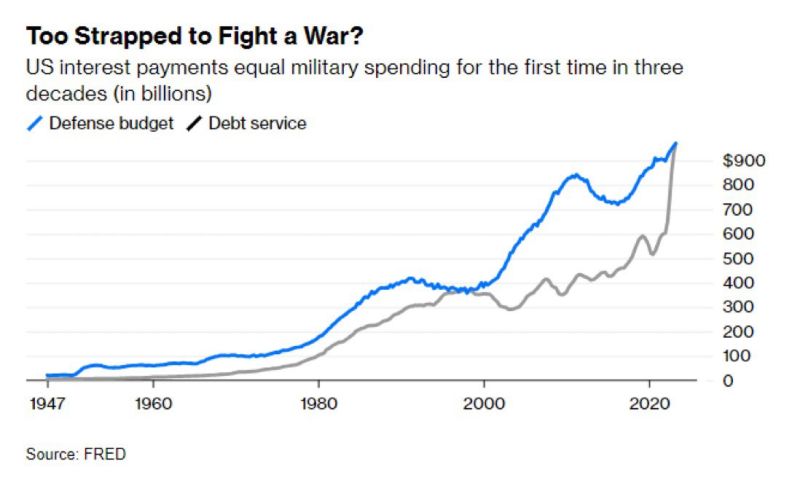

U.S. interest payments just eclipsed defense as the biggest expense…

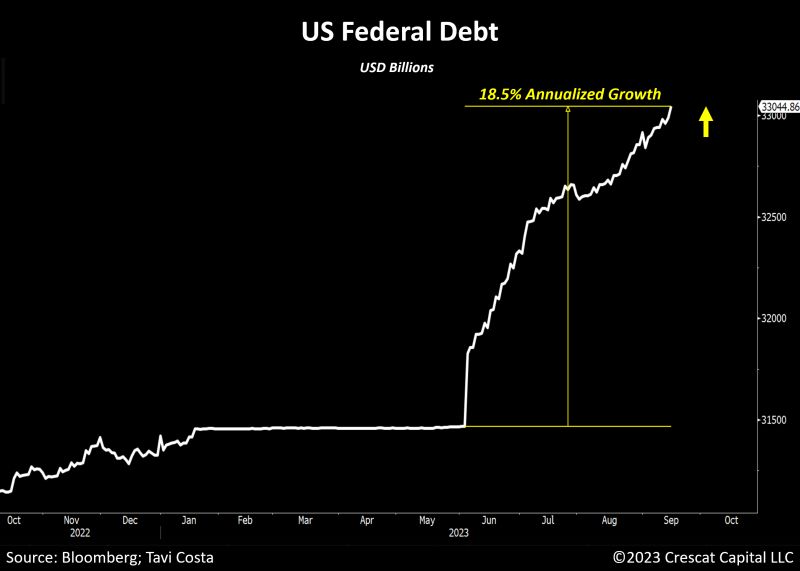

U.S. national debt is about to hit $33 trillion.

It was *only* $31 trillion on October 2nd of last year.

That’s $2 trillion of additional debt in less than 12 months.

In fact, the debt seems to be piling up ever faster.

After America’s birth in 1776, it took 205 years to accumulate $1 trillion in sovereign debt – that was in 1981.

Now, it only takes 5 weeks…

With the debt ceiling no longer in effect, federal borrowing increased by over $1 trillion between June 2nd and July 6th. On June 3rd, the national debt jumped by more than $350 billion in a single day!

This is becoming expensive in today’s interest rate environment, with debt service now exceeding defense spending for the first time in 30 years.

The Congressional Budget Office projects that in 20 years the interest costs will be nearly three times the amount of spending on infrastructure, education, and R&D combined.

This is obviously unsustainable.

And impacts all of us.

Personal interest payments in the U.S. hit a record $506 BILLION in July.

During the first seven months of 2023, Americans paid a total of $3.3 TRILLION in personal interest.

This is up a staggering 80% since 2021 and nearly above the entire 2022 total. And these numbers do NOT include interest on mortgage payments.

Americans are drowning in interest.

As I stated earlier, context is key.

The current monetary policy in the U.S. is starkly misaligned with the surge in Treasury issuances and the prevailing levels of fiscal irresponsibility…

And this is the trouble with bonds.

To be clear, short-term U.S. Treasuries (maturities 90 days to five years) do offer investors a better opportunity for stashing cash… but the duration risk of owning long-term bonds seems to outweigh potential reward.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.