Related Blogs

September 21, 2023 | Avalon Team

Bonds are having a bad day.

In the aftermath of yesterday’s meeting of the Federal Reserve, rates are moving higher causing both stocks and bonds to move lower.

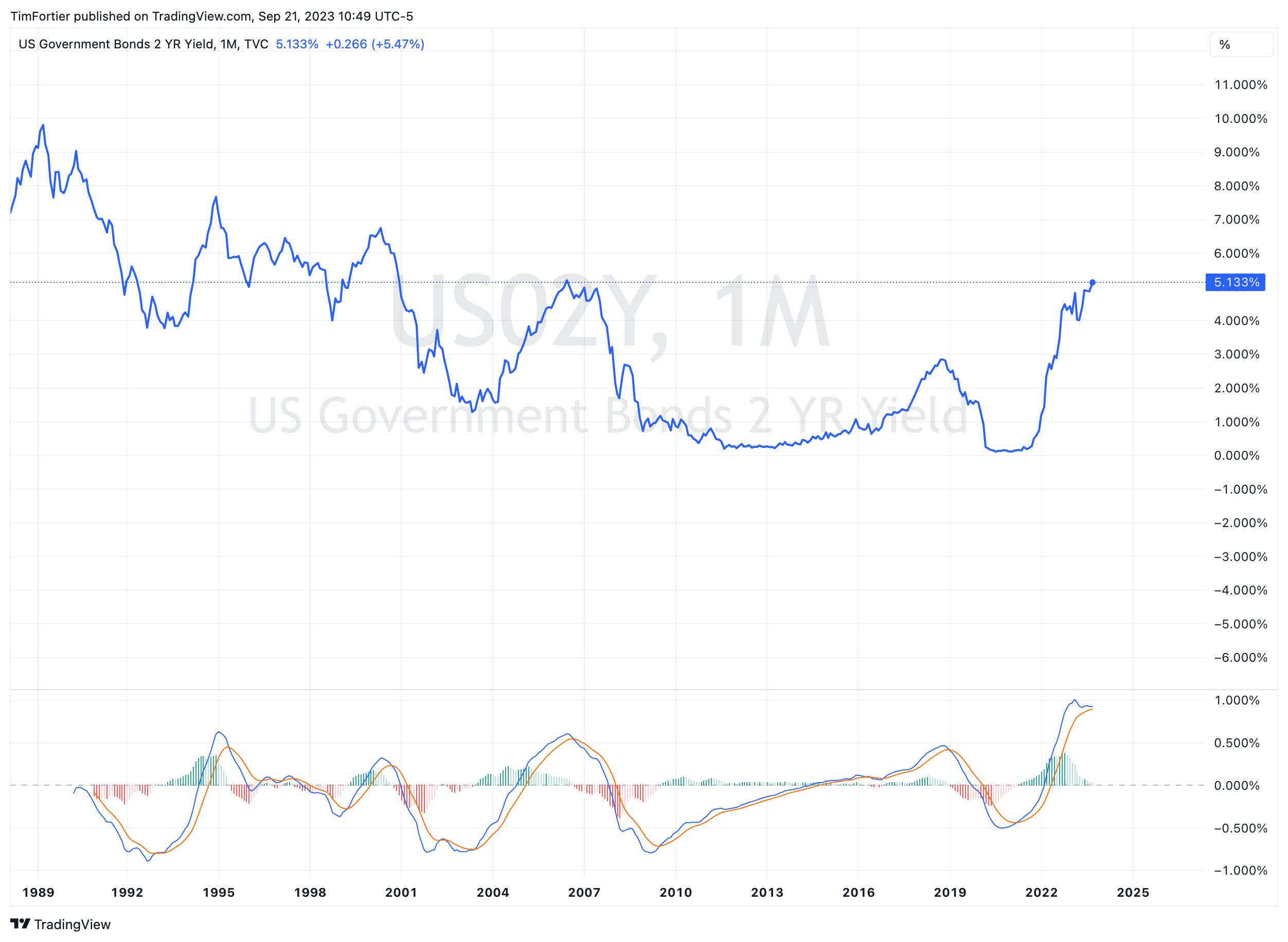

U.S. 2-year yields hit their highest level since 2006.

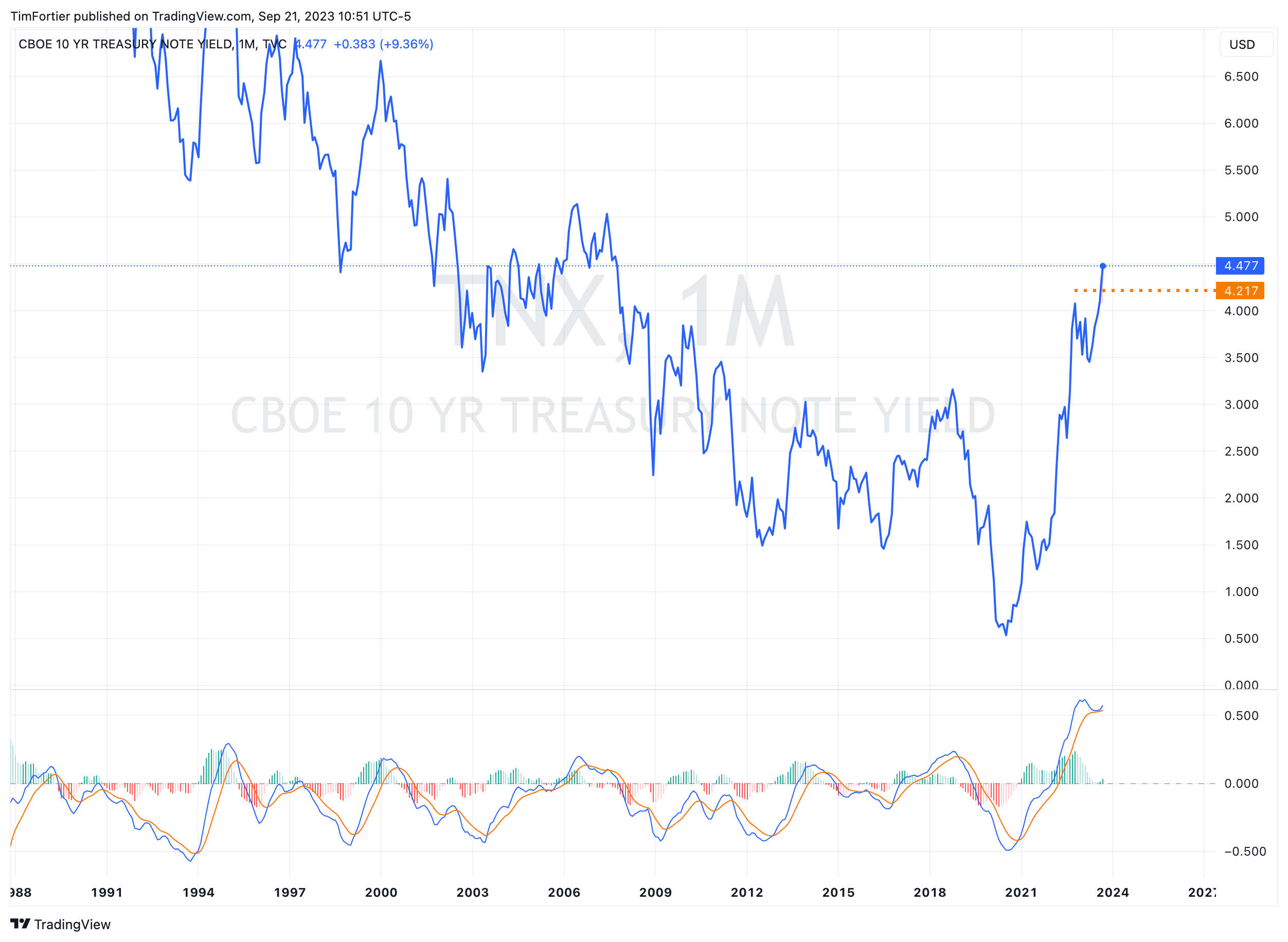

As is the U.S. 10-year.

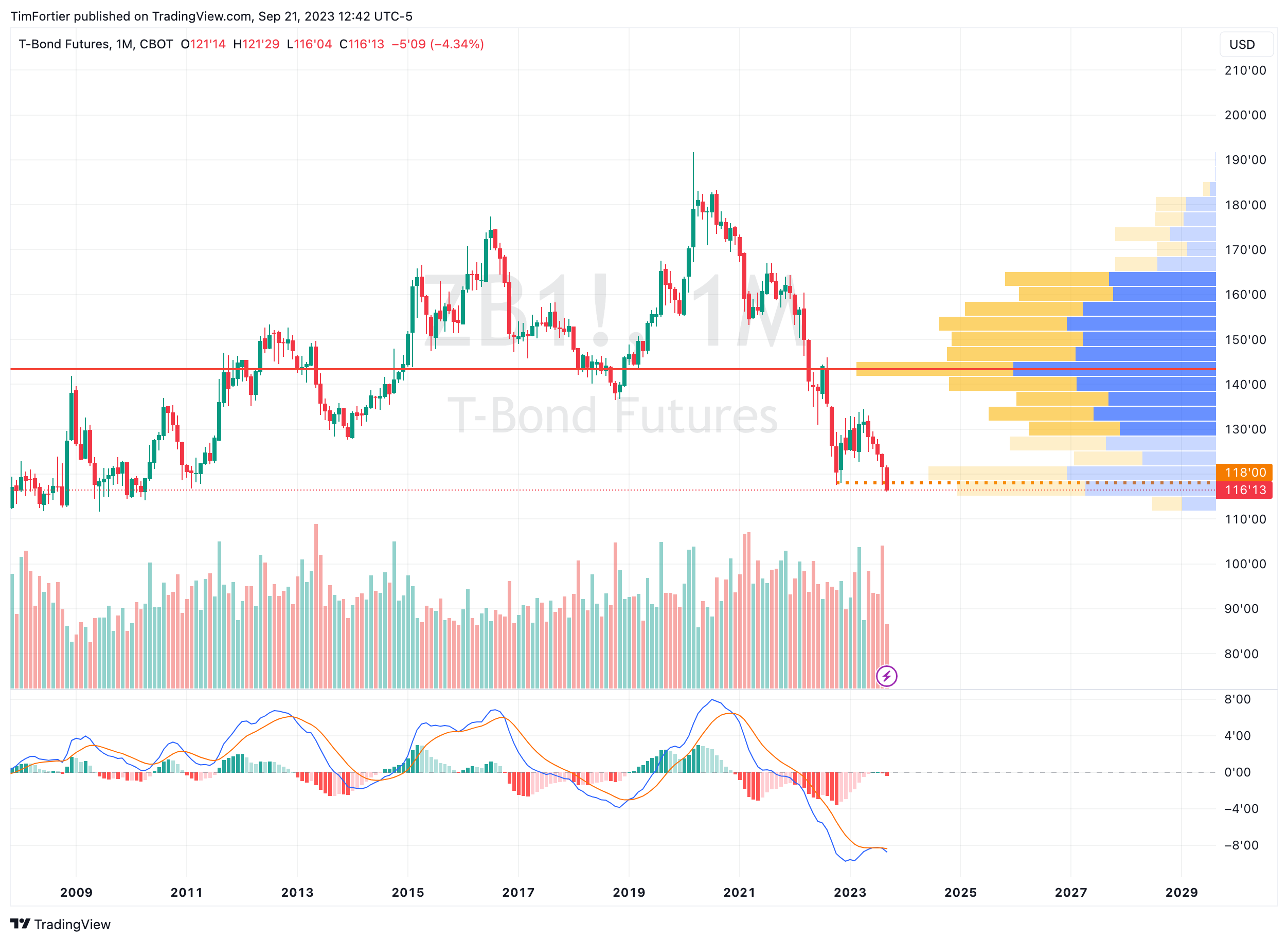

And the T-Bond futures, which represent long-duration bonds, are breaking to new lows.

Here is a summary of yesterday’s meeting:

- Fed PAUSES rate hikes leaving rates unchanged. Holds benchmark rate in 5.25-5.5% target range.

- Fed officials see one more rate hike, seven Fed officials see no more rate hikes. (One Fed member is projecting a 6.125% end-of-2024 rate.)

- Fed sees rates higher for longer -> Dot plot of rate projections shows policymakers still foresee ONE MORE HIKE THIS YEAR but 2024 and 2025 rate projections EACH ROSE by a half-percentage point, a signal the Fed expects rates to stay higher for longer.

- Fed sees inflation at 2.6% in 2024. Median projection for economic growth in 2023 jumps to 2.1% from 1% in June; officials significantly reduce unemployment forecasts and now expect jobless rate to peak at 4.1%, rather than 4.5%.

- Statement repeats prior language saying officials are considering “the extent of additional policy firming that may be appropriate.” Fed acknowledges job gains have “slowed” but says they “remain strong.”

Bottom line: Fed = futures now no longer show rate CUTS beginning until September 2024.

To put this in perspective, three months ago futures were expecting four rate CUTS in 2023. Now, interest rates are expected to PAUSE for at least one year…

This is a BIG DEAL.

Stock investors have been heavily discounting the idea that the Fed may actually CUT rates. That’s not happening.

And now comes the reconciliation with growth stocks priced at historically high valuations, that such multiples may not be justified in the current environment.

Remember, the higher rates go, the lower valuations are driven.

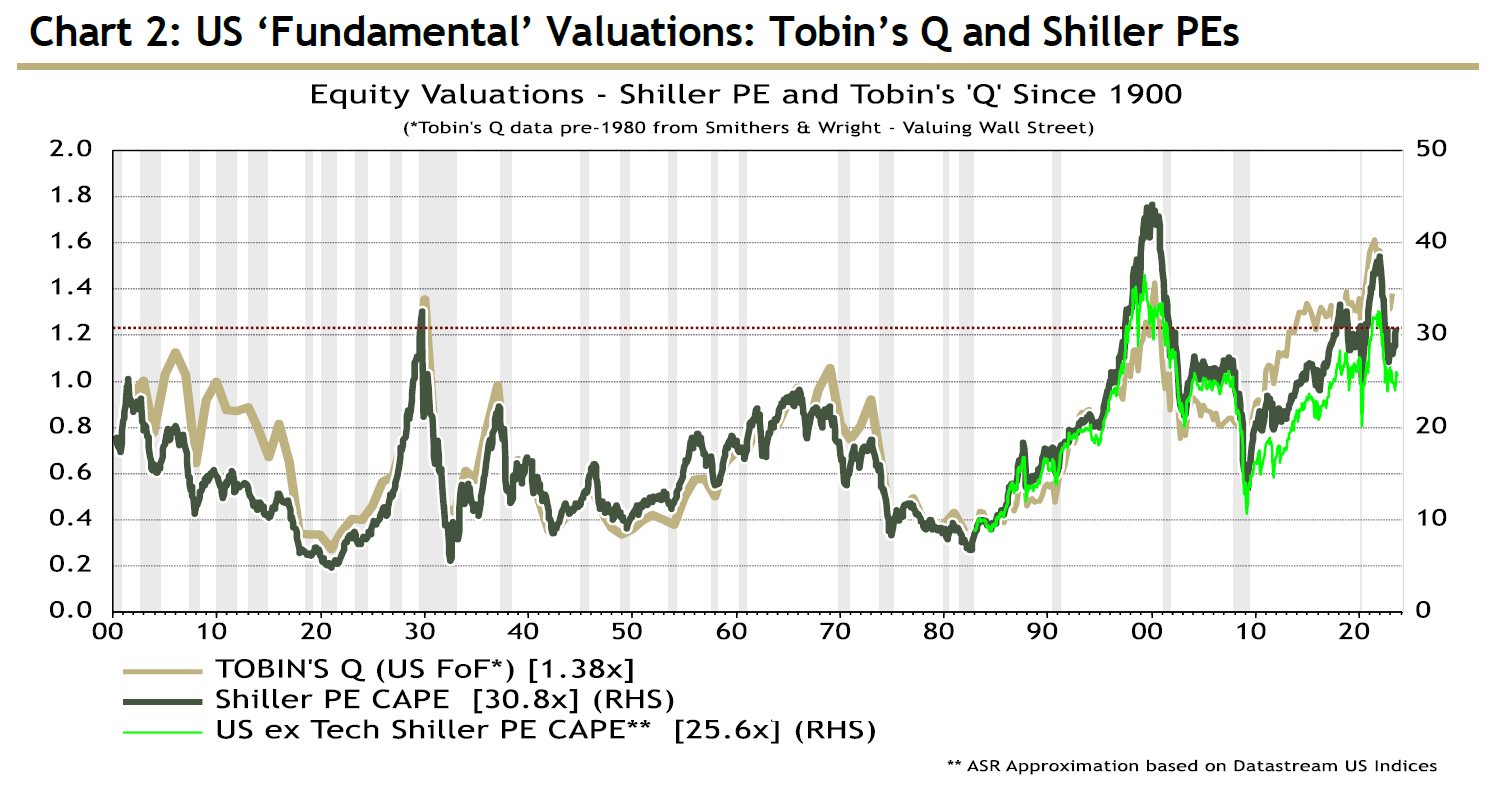

I will share again this chart to serve as a reminder that stocks are priced at historically high valuations.

Remember, this is based on current earnings. Should the economy contract, then earnings will likely decline from current levels and could create a double whammy of both falling earnings and declining valuations.

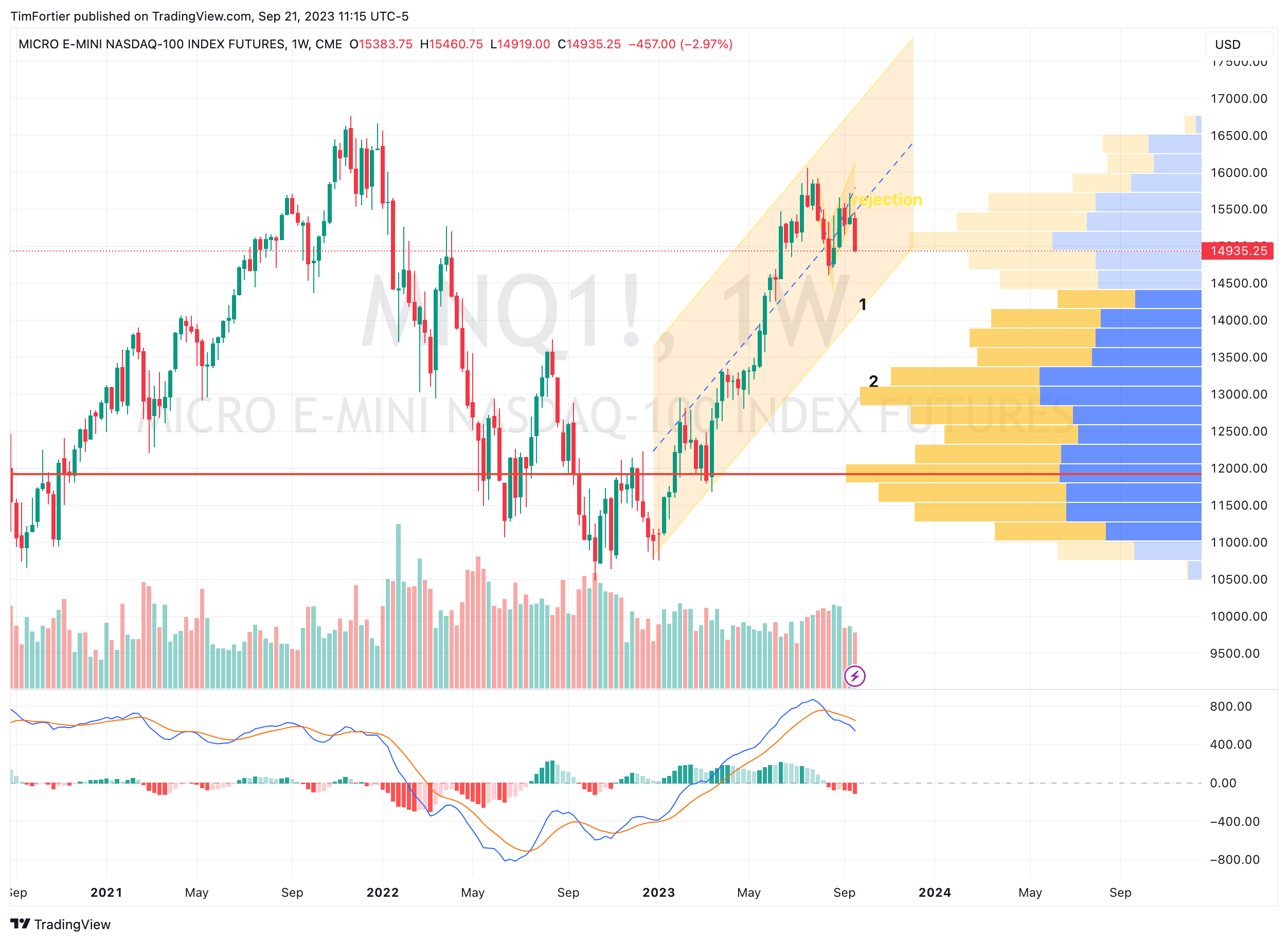

Here is a chart of the Nasdaq, where many of the popular growth stocks trade.

From the October 2022 low, price has formed a well-defined channel.

I have numbered two potential immediate targets. #1 defines the bottom of the current channel and #2 defines a potential support identified from the volume profile.

I need to stress, that much lower levels would be indicated if the market were to decide to price stocks at valuations closer to the historical average.

As I communicated over 18 months ago… rising interest rates would usher in a new regime leaving many investors unprepared and traditional portfolios at risk.

It is happening.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.