Related Blogs

June 30, 2022 | Avalon Team

I spent last week with family, vacationing at a Minnesota lake my parents first took me to in the sixth grade. I immediately fell in love with the fishing and the beautiful outdoors.

I spent last week with family, vacationing at a Minnesota lake my parents first took me to in the sixth grade. I immediately fell in love with the fishing and the beautiful outdoors.

I would go there five more times with my parents, and once my career settled in, I started visiting again. And now that I have kids of my own, we’ve started the tradition of going up for a week of vacation every year.

The lake and the area have changed very little, and each time I am there it feels as though it was just “yesterday” since the last time.

Familiarity can be great, and I am sure many investors are wishing that this market would feel like its old familiar self, but that isn’t the case nor is it likely to be.

That is, after all, the nature of a regime change.

I witness seemingly intelligent people operating as if nothing has changed. It is symptomatic of the deeply entrenched Bull Market psychology from the previous regime.

In Bull Markets, investors accept risk to pursue gains, and the masses are trained to buy the dips. In Bear Markets, risk MUST be managed to preserve capital.

In other words, the rules of the game have changed.

While holding cash may feel dissatisfying, each dollar preserved in your account buys more assets as prices decline. You win by not losing.

Assuming you do manage to protect your portfolio from losses, there remains one challenge: With inflation running high, the cash on hand will buy less food, less energy, and so on.

That is what makes this era so challenging…

The Fed’s Wile E. Coyote Moment

On Wednesday, Fed Chairman Powell stated that the Fed’s biggest mistake would be to let high inflation persist, suggesting that it must accept higher recession risk to bring down prices.

We also learned in macro news, the U.S. Q1 GDP print was finalized at -1.60%, slightly below the last revision of -1.50%.

Additionally, we found out what consumers already knew… that Real Disposable Income collapsed 12% in the first quarter, making three quarters in a row that it has fallen.

This decline is worse than what occurred in the 2008 recession.

As we’ve discussed previously, the Fed is tightening at a time when we are likely speeding toward a recession.

The script that we can expect the Fed to follow goes like this: They will raise rates until the immediate economic consequences are worse than the inflation.

Stated another way, they will raise rates until they cause a recession or some other financial crisis.

The impact of these decisions will be felt for a long while by investors.

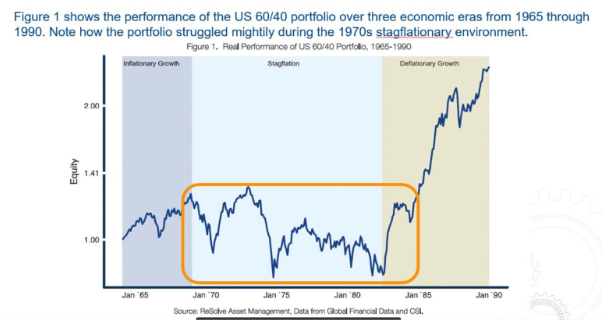

The chart below demonstrates what investors are now experiencing. During periods of stagflation, traditional asset mixes simply do not perform well (as detailed in my series, “The Death of 60/40”).

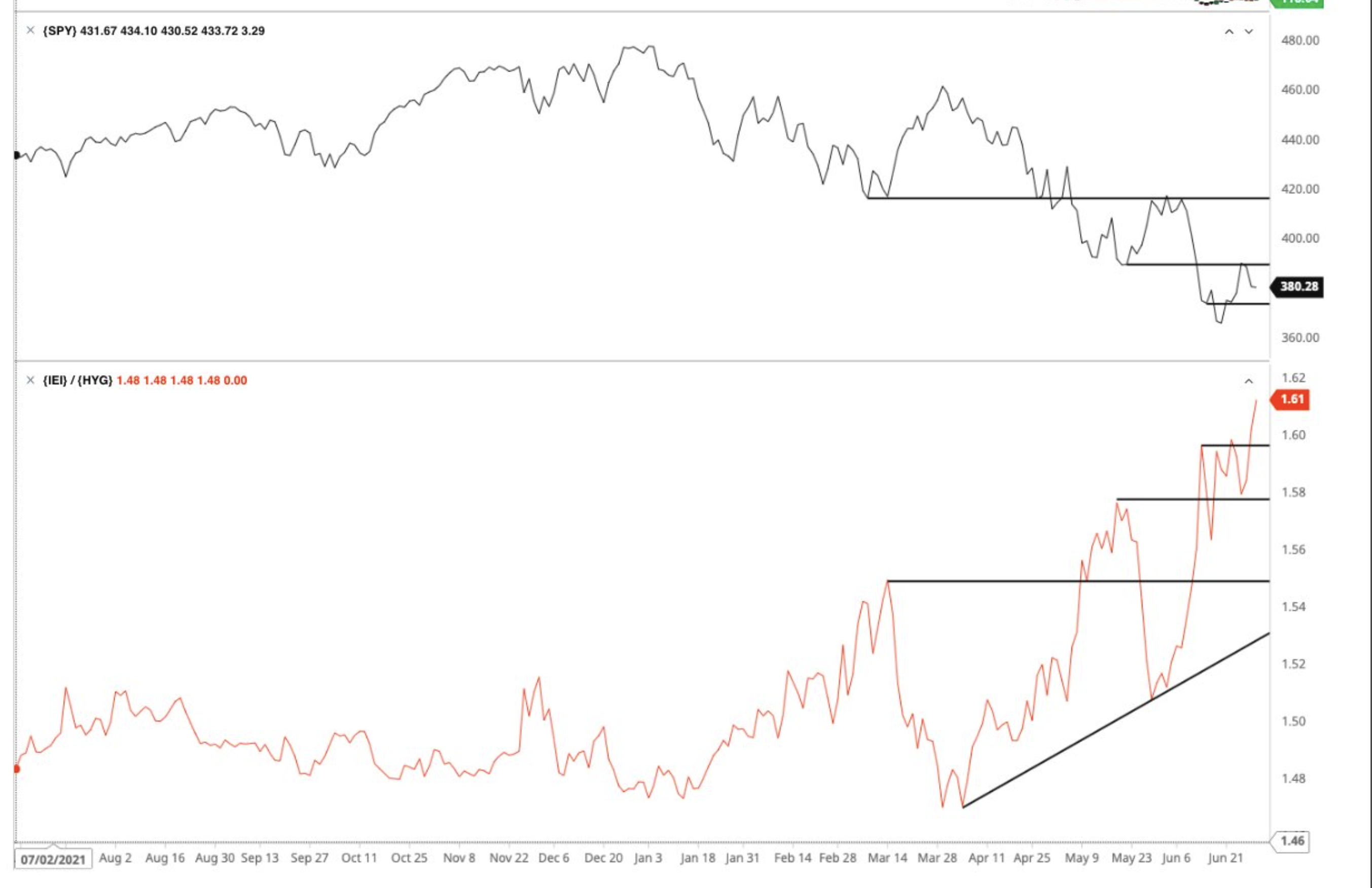

I continue to monitor the high-yield market with growing concern. The spread between high-credit quality and low-credit quality bonds is continuing to widen. This suggests a growing concern for default risk.

I know I have said this in the past but it bears repeating: The credit markets lead the stock market and the message here is clear – stock prices are not finished on the downside.

The high-yield market is also worth mentioning because in recent years, many investors have reached for high-yield as a way to deal with low to no yields available in more traditional products like bank CDs, Treasuries, and investment-grade corporates.

The temptation is understandable: high-yield bonds have offered an average of 566 basis points of option-adjusted spread (OAS) above U.S. Treasury yields since the 1980s.

The problem with this, however, is that high-yield bonds tend to behave like equities, especially in bad markets.

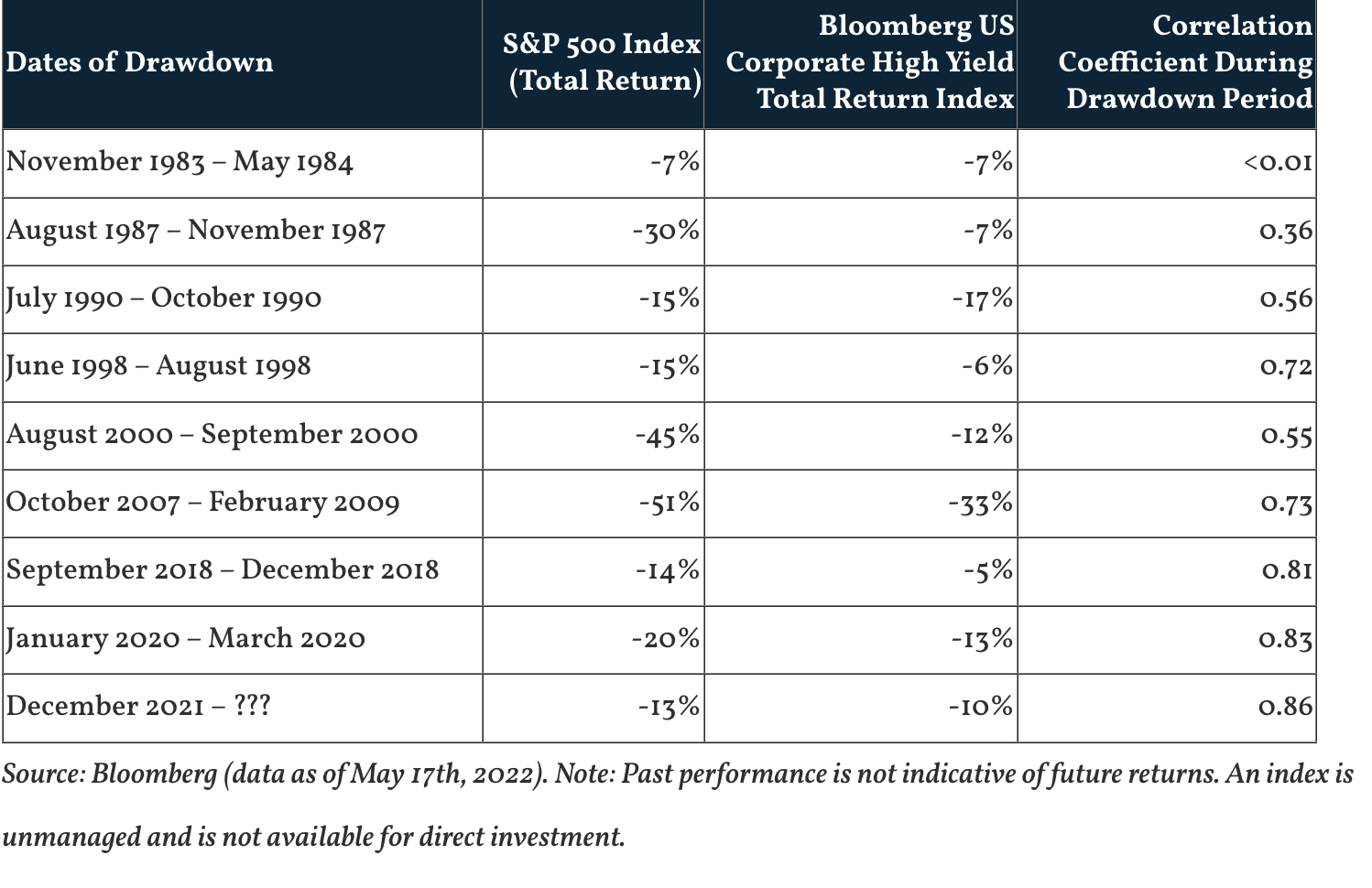

High-yield bond allocations have a higher correlation to equities when the S&P 500 sells off – of nine major stock market sell-offs since 1983, the high-yield index posted negative total returns nine times and double-digit negative total returns five times. In two instances (1983-1984 and 1990), the high yield index lost as much or more than the S&P 500.

The reason for high-yield bond losses is simple: During periods of economic stress, defaults increase.

For example, in 1991, 2001, and 2009, high-yield bonds defaulted at a rate of more than 2.5x their normal rate, in one case hitting double-digit default percentages in 1991.

So far in 2022, high-yield bonds (as measured by the ETF HYG) have lost over 13%.

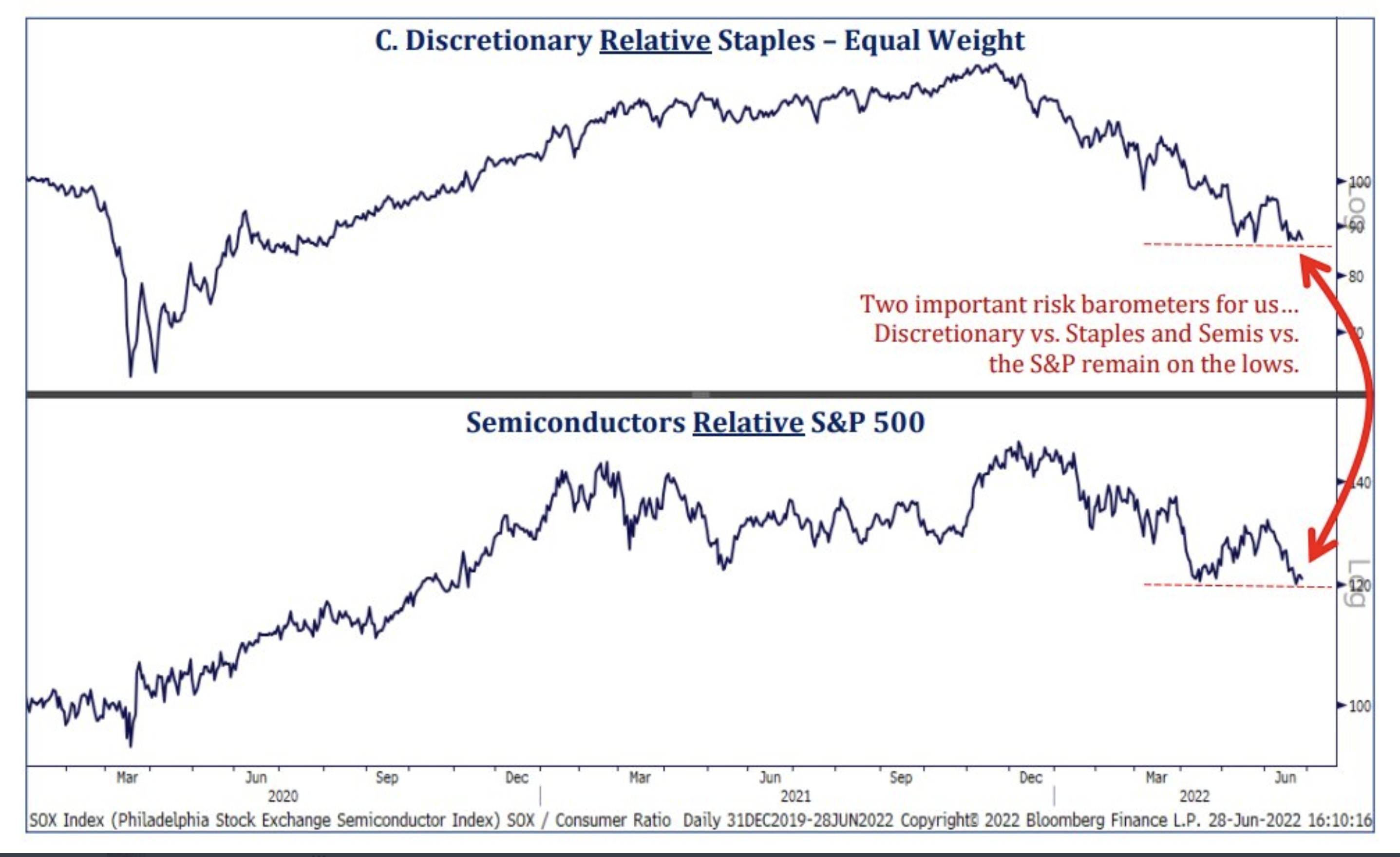

Consumer Discretionary relative to Consumer Staples, and relative to the S&P 500 are both at recent lows and trending lower.

The first speaks to the cutback in spending by the beleaguered consumer. The second speaks to the ongoing downward pressure on technology, as semis are considered a leading gauge.

Last week, I pointed to the defined trend channel that the stock market has been following. I had suggested that the market was poised for at least a short-term bounce.

We got that. The S&P 500 was up 4% last week, but has since started showing signs that the rally may be coming to an end.

The trend channel continues to define price movement as this update shows.

Note that the 50-DMA also coincides with the top of the channel, presently slightly above 4,000. This will likely be stiff resistance should prices even reach that level.

Here are the similar levels and channel, for the Nasdaq 100 (NDX).

While the U.S. markets certainly do not look inviting, the many foreign markets look even worse.

Take for instance, the German DAX, considered a leading index for Europe. This “engine of Europe” has not closed here since November 2020.

The most important thing for investors to understand now is that rules to the investing game have been replaced with new ones.

The sooner investors stop playing by the old rules of “buy the dip” and embrace the new rules of “manage the risks,” the sooner to some sense of stability.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.