Related Blogs

October 11, 2023 | Avalon Team

For many investors, 2023 has been a challenging market unless you were fortunate enough to own the handful of mega cap stocks that have been responsible for most of the market performance.

Diversification has hindered performance, not helped.

The uneven performance can be seen in this chart which shows how the mega caps have returned nearly three times the return of the S&P 500.

Small caps have not even been a contender and bonds are suffering their second consecutive year of losses.

Even more striking is the disparate performance between the market-cap weighted S&P 500 (blue) and the equal-equal weight S&P 500 (green) in which the latter is up only 2.07%.

The performance of the large caps has masked the underlying weakness of the market.

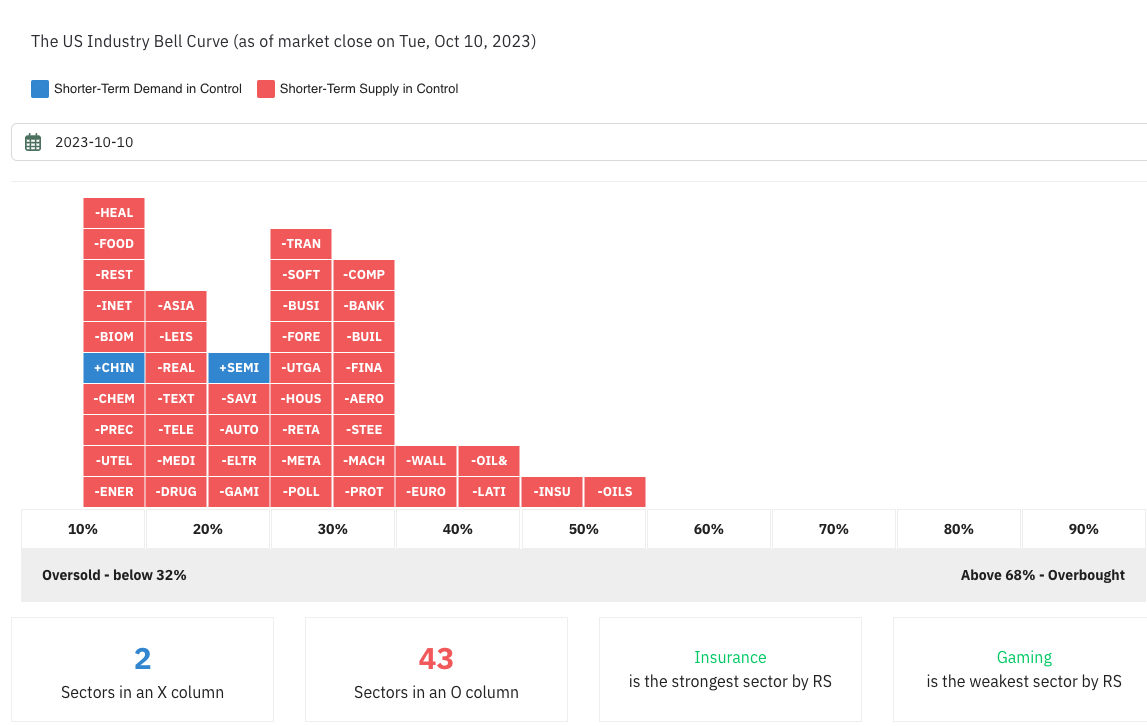

The sector bell curve shows a market in which every sector, up to a couple of days ago, was controlled by selling pressure.

Also notable is how the sector curve has skewed to the left, which again, demonstrates the intensity of the selling.

One of the primary reasons behind the selling has been the rise in interest rates. But, as Mike Reilly correctly pointed out, rates look ready to take a breather.

Recently, the 10-year UST reached 4.80% but has since declined to under 4.60%.

And this, despite today’s report that the producer price index increased 0.5% for September, against the Dow Jones estimate for a 0.3% rise.

Inflation pressures came primarily from final demand goods, which surged 0.9% on the month, while services increased 0.3%.

While soaring Treasury yields keep causing pain for bond investors, the recent surge may also be serving to do the Fed’s work for it.

Fed members are starting to take a more dovish tone in recent comments, which helped risk asset prices stage a late Monday rally despite the heightened risk of developments in Israel.

With stocks sitting 7% off of all-time highs and trending mostly negatively over the past two months, investors may look for any kind of positive news as a buy-the-dip moment.

This would confirm what we’re seeing from the risk signals right now, which suggest a short-term risk-on opportunity even though the intermediate- and long-term pictures look more cloudy.

Monday’s price action was interesting because it showed that investors might be thinking about a safe haven trade.

Following the political unrest in the Middle East, investors sent Treasury prices across all durations significantly higher, while gold added 2%.

It’s far too early to extrapolate much from such a small data set, but the Israel conflict coupled with the Fed’s potentially new dovish lean, could be enough to finally take some pressure off of bond yields in the near-term.

As technology stocks have been especially sensitive to increasing interest rates, it is interesting to note that one of the first sectors to turn positive is semiconductors (see sector bell curve above).

As this industry group is often viewed as a bellwether for technology stocks, it will be important to see if this can lead to further follow-through.

If the Fed is indeed taking a more neutral stance on policy compared to its position a month ago, it could potentially make this week’s CPI and consumer sentiment reports less consequential to the markets.

For the better part of the past two years, both stock and bond prices have been driven by interest rate changes and the expected path of the Fed’s monetary policy conditions.

For now, we’re still seeing a positive correlation between stocks and bonds, which means that even if we’re seeing some flight-to-safety activity here, it isn’t strong yet.

One wild card for inflation is oil.

Despite the Mideast tensions, the oil market has shown little reaction.

Prior to last weekend’s horrible events, oil had begun to pull back after its recent surge.

Until oil can close above $88-$90, it would appear that oil will not add any additional pressure to inflation. However, a potential catalyst would be that this conflict spreads to Iran.

Indicators such as the Percent of stocks above their 50-day moving average and the Mclellan Nasdaq Summation Index suggest that the market is firming up.

A further meaningful backup in interest rates may be the only catalyst needed to send stocks higher from current levels.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.