Related Blogs

March 1, 2023 | Avalon Team

There’s an old saying that the only certainty is uncertainty when it comes to the financial markets, and it couldn’t be more true.

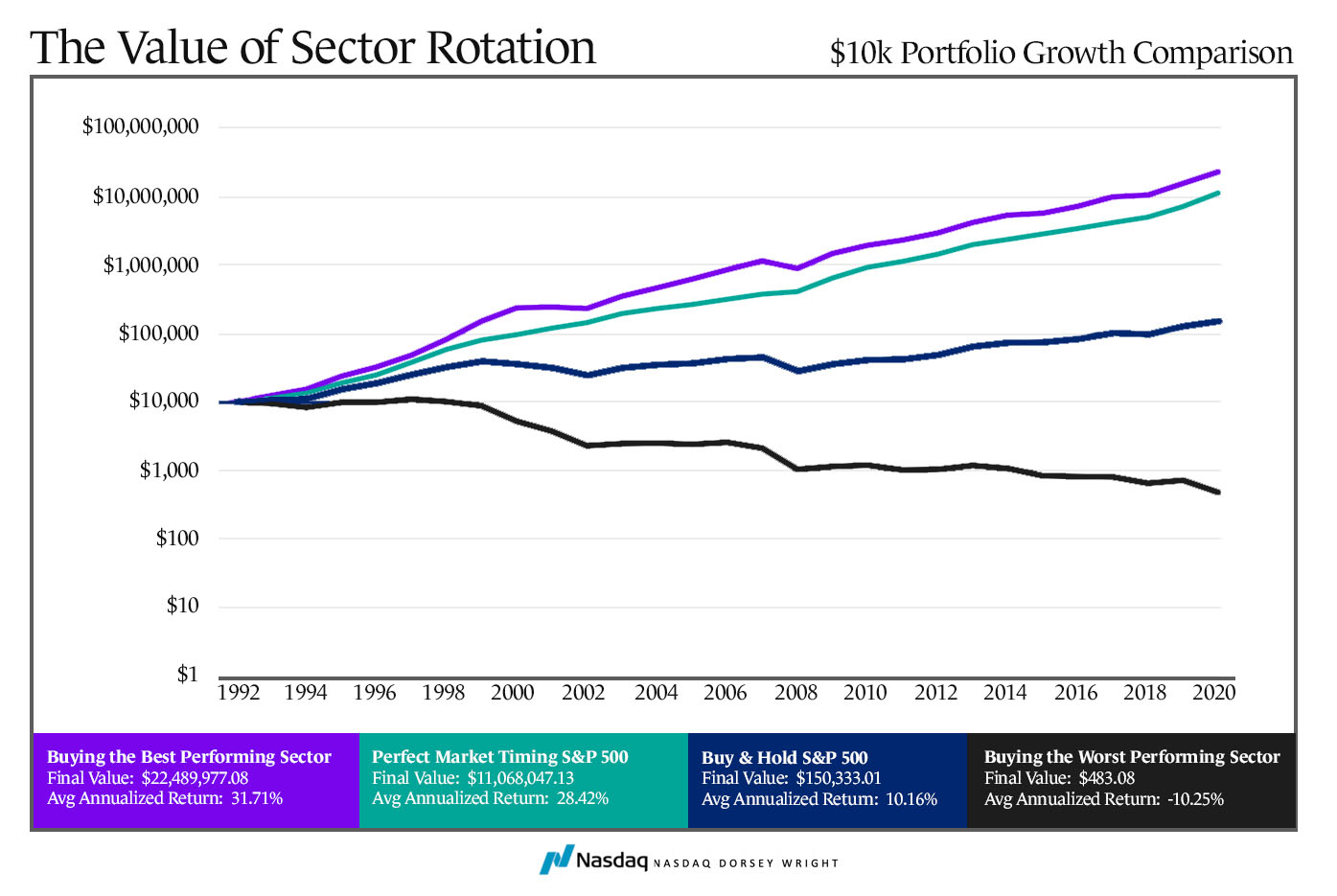

For Avalon, the North Star that guides us through the markets has been and always will be Relative Strength. For over 20 years, we’ve researched and tested the Relative Strength strategy we offer our clients.

The simple process of avoiding what is weak and only allocating to what is strong can mean a sizeable difference in return.

The economic debate de jour is whether or not the U.S. economy is about to experience a soft landing, a hard landing, or no landing at all.

While the future is unknown, the good news is that by using relative strength, we don’t need to know as it will signal the portfolio changes that we need to make at the appropriate time.

The result is a portfolio that adapts to changing market conditions.

Contrast this to the route of most advisors, which is to use a static portfolio allocation regardless of the market or the economy. This approach takes much less effort to implement, but can often lead to large, protracted drawdowns that can forever derail a financial plan.

The message presented to us by Relative Strength is that risks are increasing.

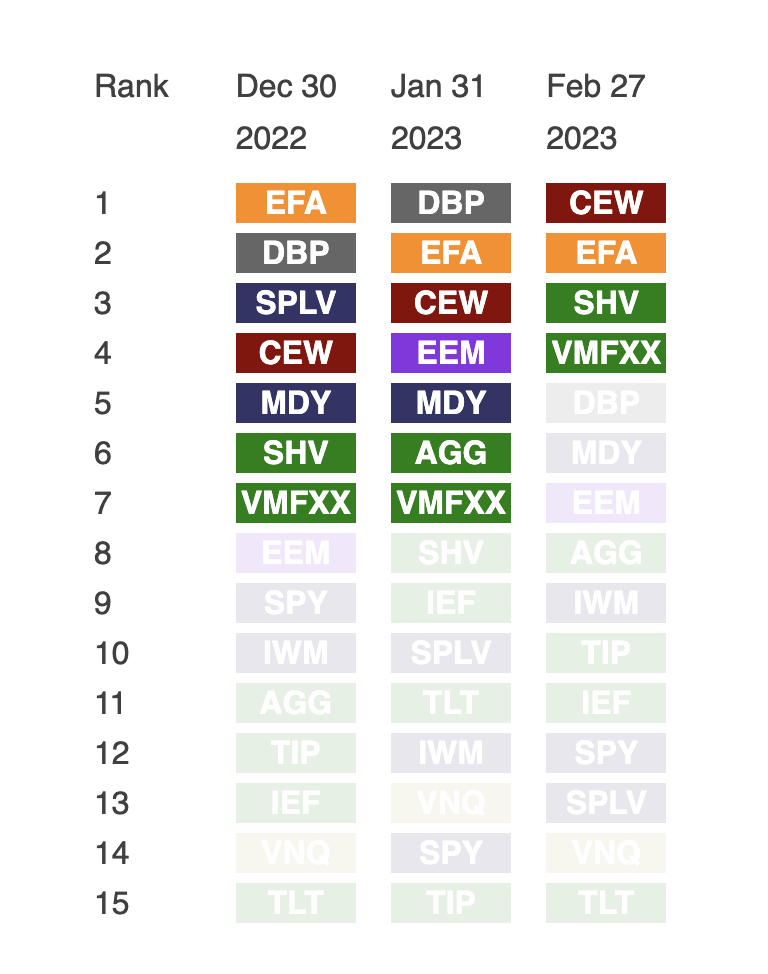

First, our absolute momentum screen, after a few months of improvement, is beginning to show fewer attractive asset classes.

Emerging Market Debt (CEW) has recently climbed to the top spot in our ranking followed by International Equity-ex U.Ss (EFA) but notice that TBills (SHV) and cash money markets (represented by VMFXX) now occupy the number 3 and 4 spots.

This represents a clear shift to a more “risk-off” environment than what we saw in December and January.

Noticeably absent from the current absolute ranking is any U.S. equity asset class.

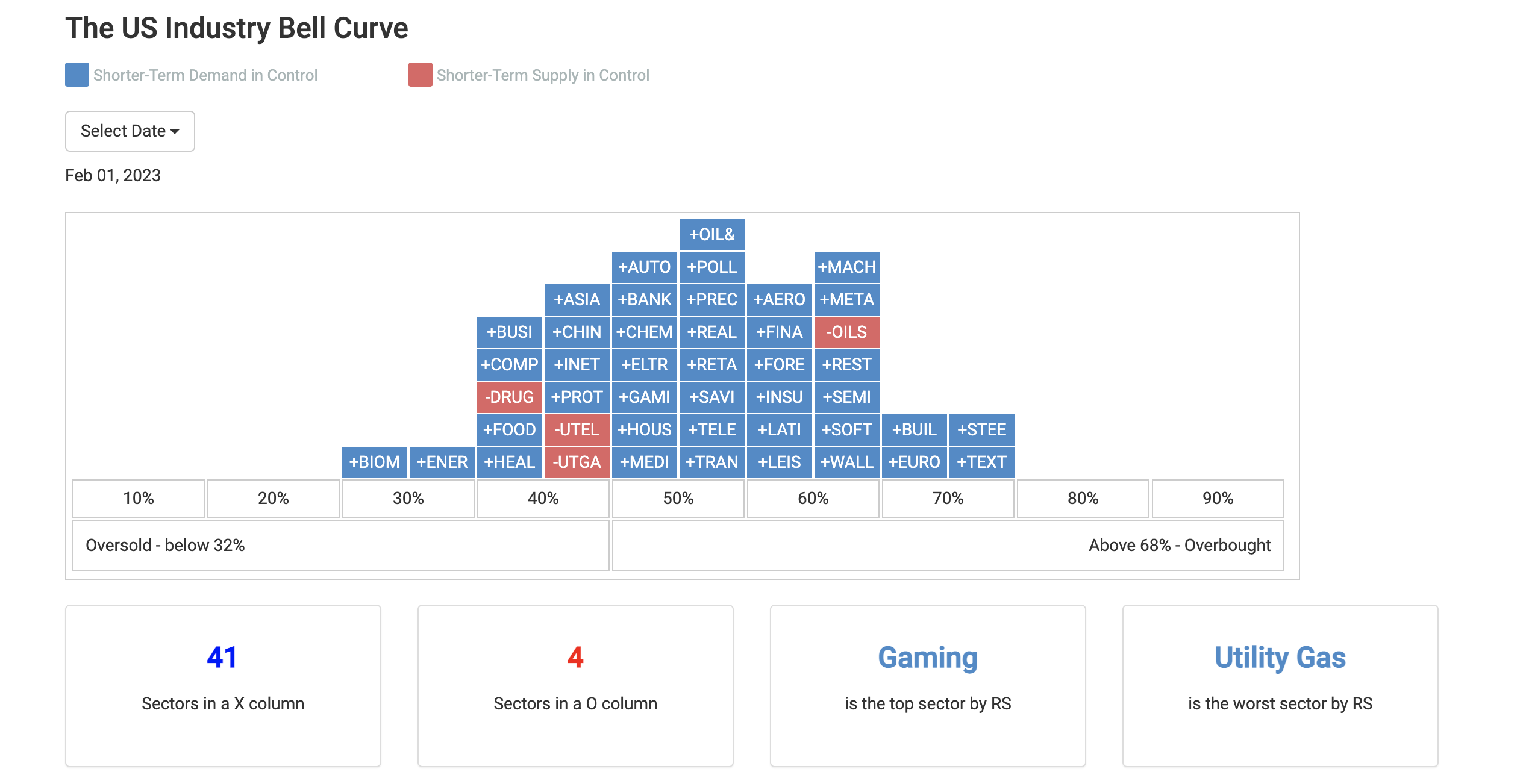

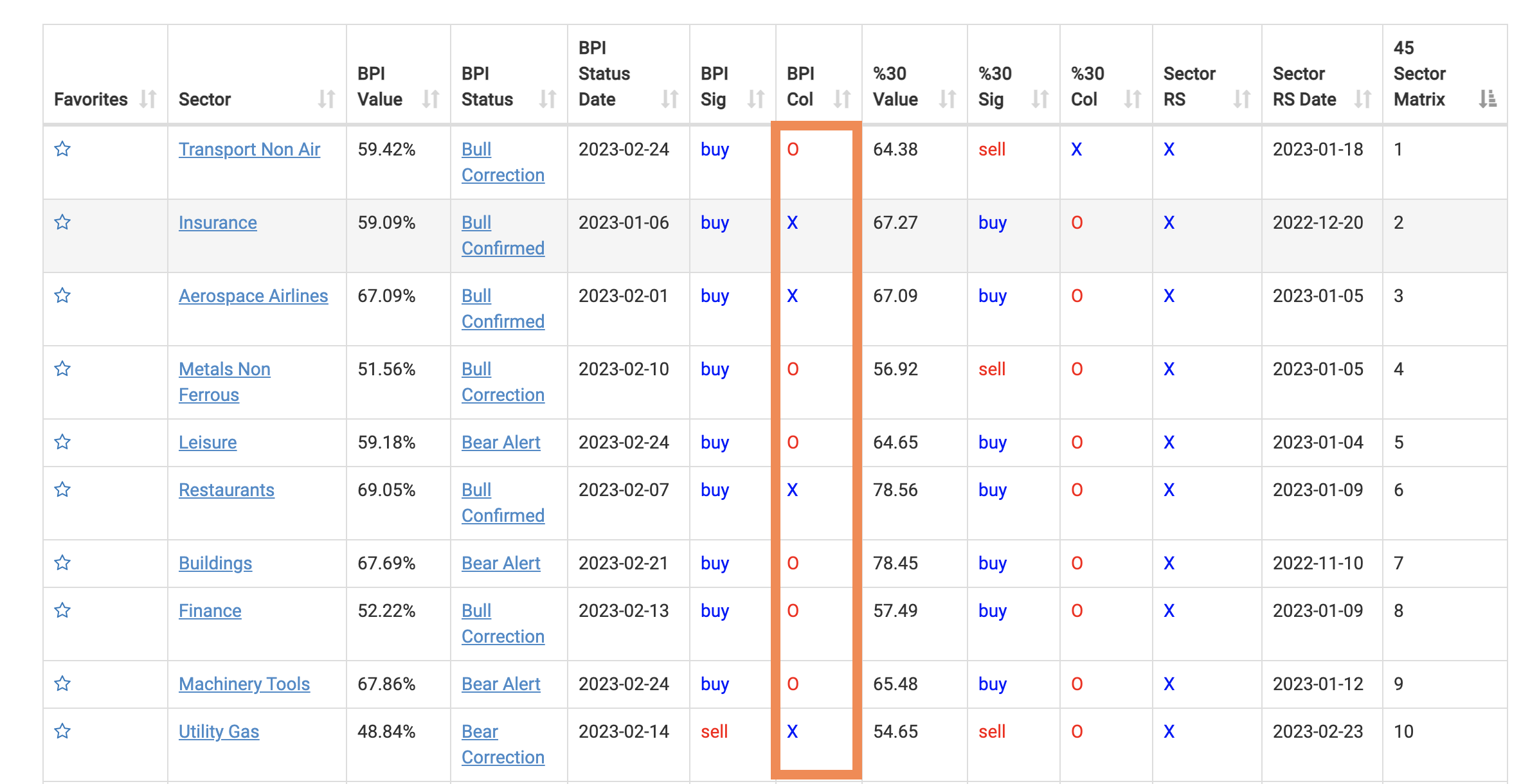

Following that up, here then is looking at the market through the lens of the U.S. Industry bell curve that organizes sectors on the basis of relative strength.

The month of February began with 41 sectors controlled by buying demand.

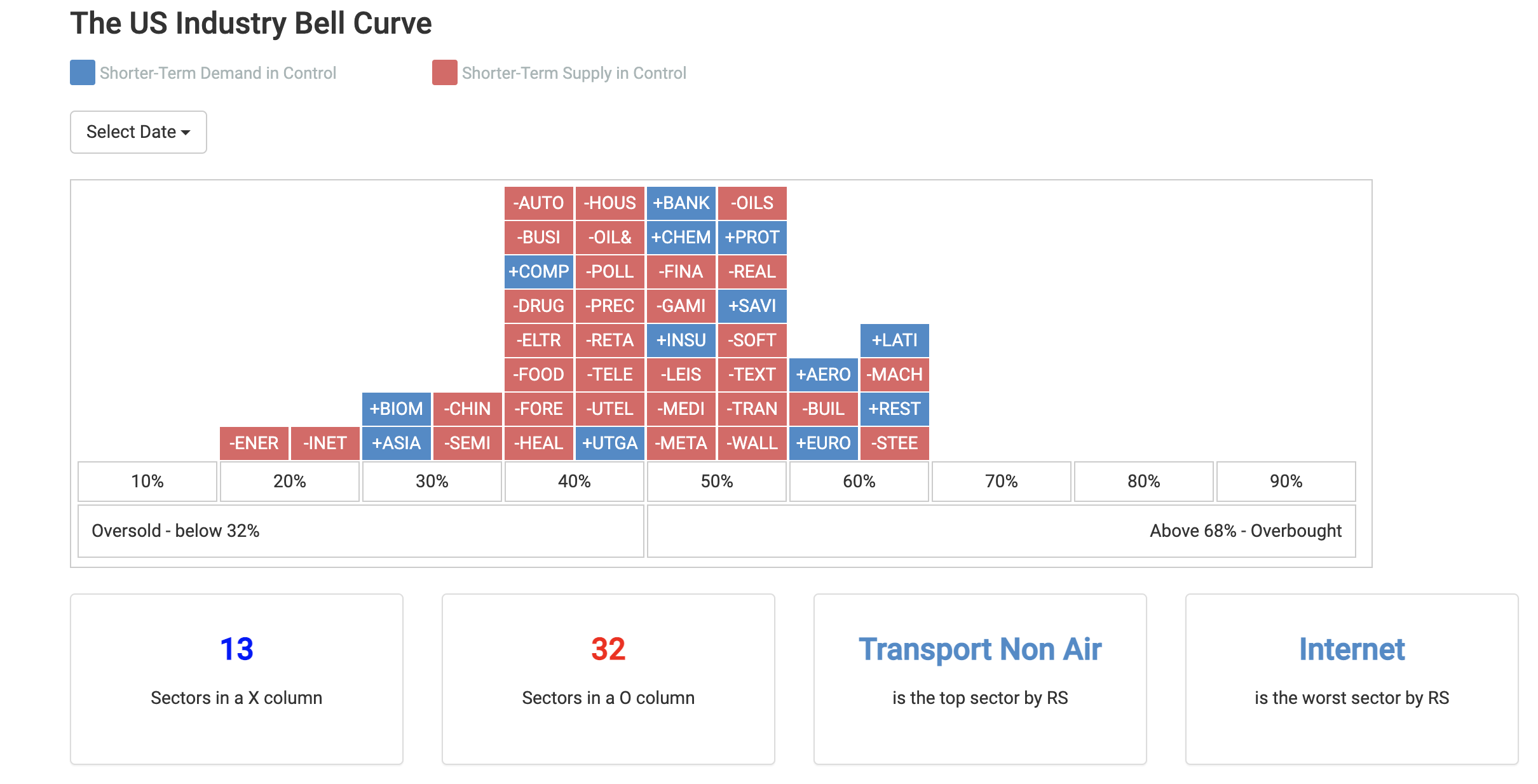

The current view shows only 13 sectors being controlled by demand.

Now see the contrast when compared to the current status of the US market. Only 13 sectors are now bullishly controlled.

But even among the current top sectors that still are bullishly controlled, notice in the table below that only 4 of the top 10 are in a column of Xs, informing us that even the strongest U.S. sectors are showing at least some short-term weakness.

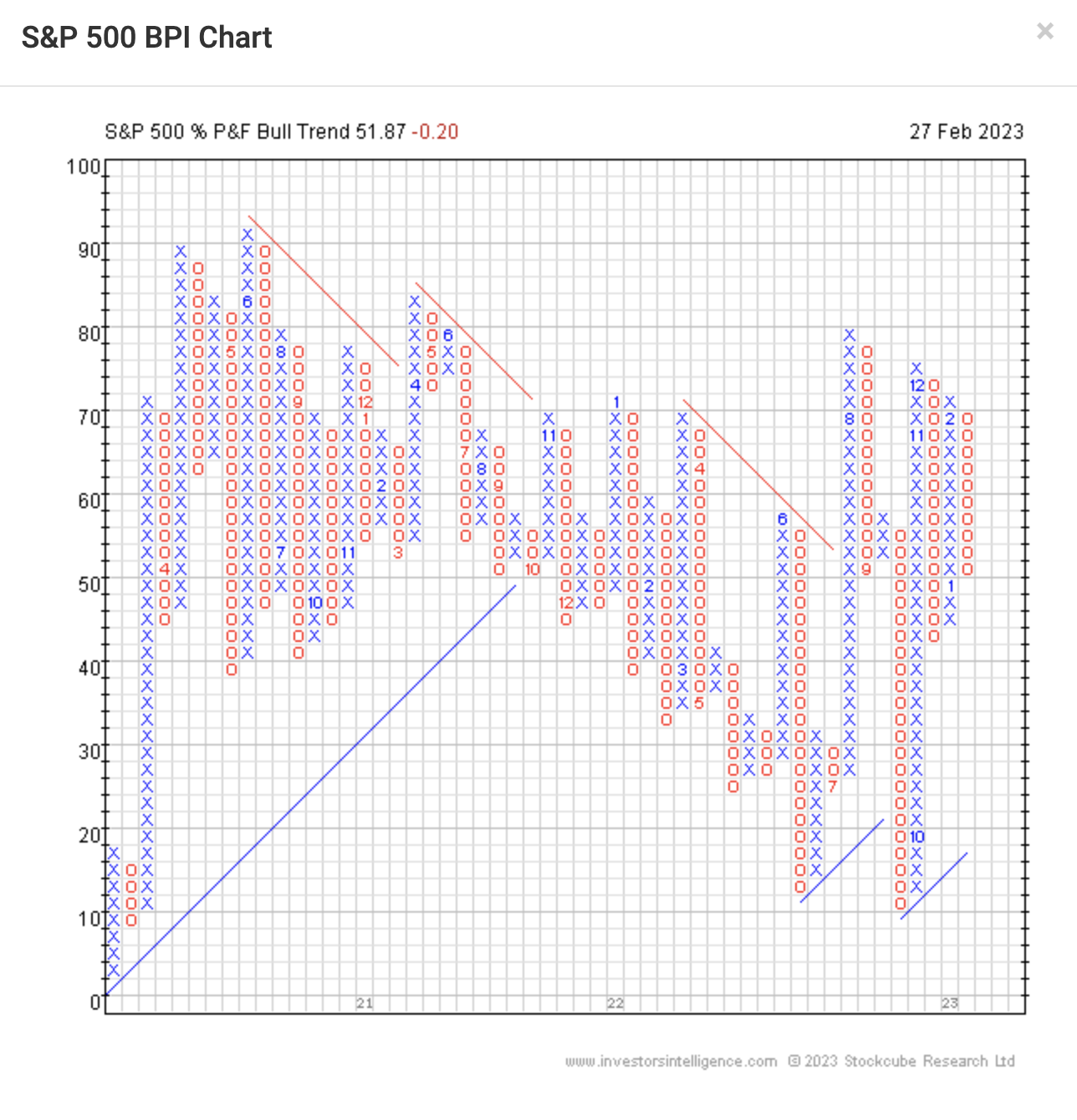

Technically, looking at a monthly chart of the S&P 500 Index, we had an inside bar with a chance to go up and over the downtrend line.

But the market has failed.

The dominant trend lower appears to be in sync with what both our absolute momentum is telling us and our sector relative strength studies.

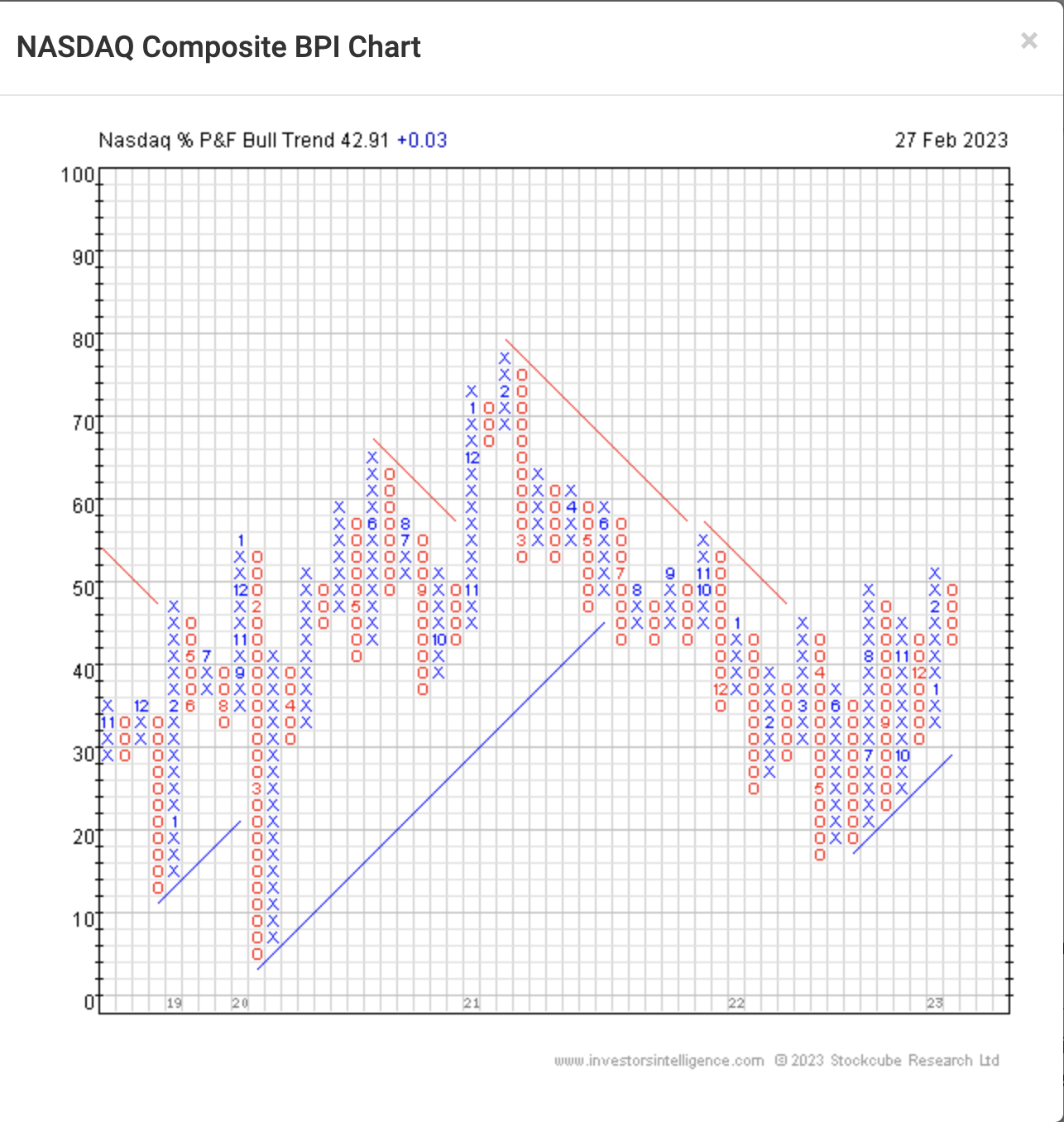

Looking deeper “inside” the market, at our supply/demand bullish percent indicators, we are presented with the same defensive message that the U.S. market is currently controlled by sellers.

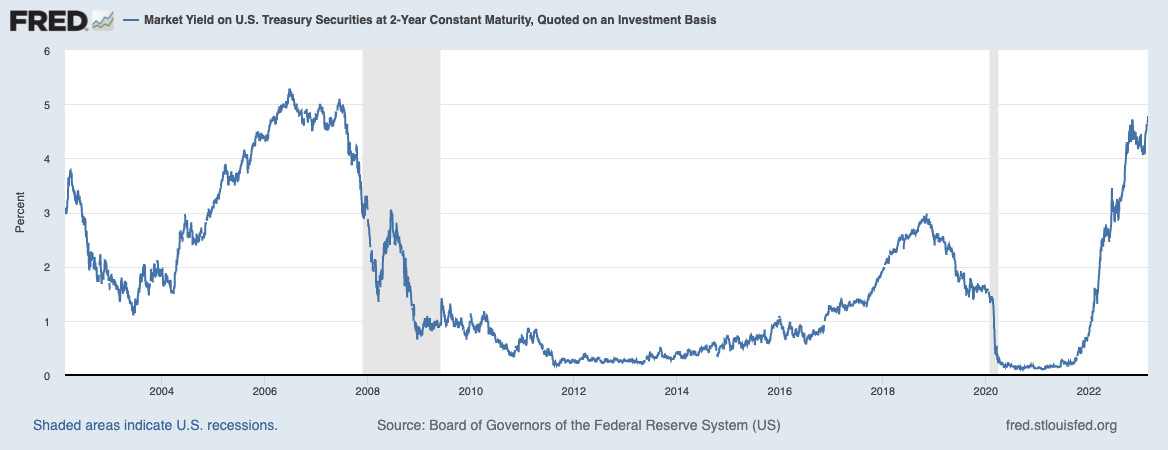

Perhaps one reason money is leaving the stock market is for the first time since 2007, investors can now earn nearly 5% on 2-Year Treasuries.

For the first time in a long time, bonds and bank CDs are once again competing for investors’ cash.

While investors may be uncertain as to the outcome of the economy, what is certain is the clear and unambiguous signals that our research is showing us.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.