Related Blogs

February 9, 2018 | Michael Reilly

The saying about Brazil is that it’s the country of the future — and always will be.

The saying about Brazil is that it’s the country of the future — and always will be.

Despite enormous natural resources, it has long shown the ability to waste its potential.

But recently, the Brazilian economy has been on a tear. Despite political dysfunction and corruption scandals aplenty, the country has seen a boost from US and global economic growth, as well as political shifts back home.

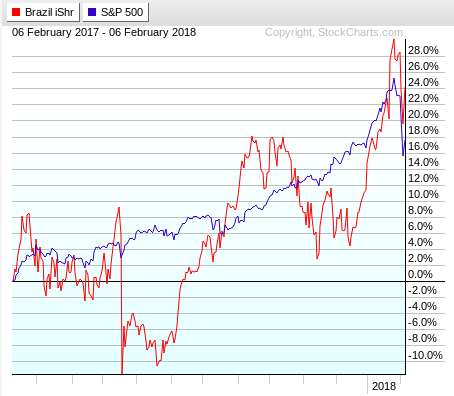

The country’s benchmark Bovespa stock index has more than doubled since hitting a seven-year low in early 2016. And in the past year, the iShares MSCI Brazil Capped ETF (EWZ), the largest ETF that tracks Brazilian securities, has seen an increase of 24.15%.

Here’s EWZ compared to the S&P 500:

Brazil is carrying out reforms on a grand scale, including a 20-year spending cap tied to inflation, which has helped pull the economy out of a deep recession and bolstered confidence in the markets. Pension reforms are also underway. And earnings growth is accelerating.

Politics play a big role. When an appeals court upheld ex-president Lula’s corruption conviction last month, stocks surged. EWZ spiked 6.2 percent higher, its biggest one-day gain since May.

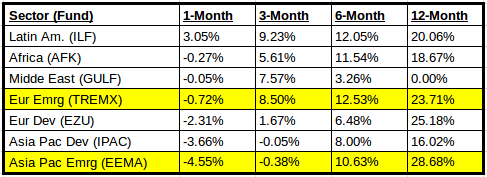

Brazil is not alone. Latin America as a whole has been on the upswing. In fact, over the last three months, the sector has outperformed all other international sectors:

It is not the strongest sector in terms of relative strength. Emerging Europe and Asia Pacific Emerging (highlighted in yellow) are the strongest. As usual, we will follow those trends until the trends end and new trends begin.

But when new trends emerge, as they always do, it pays to be aware.

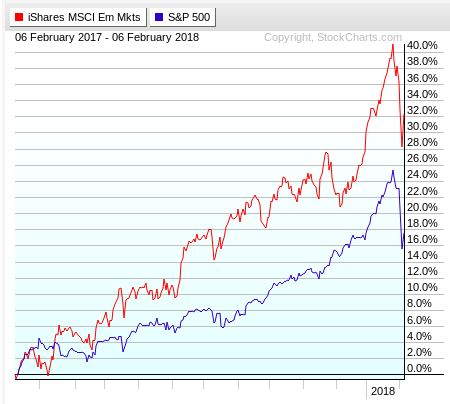

Emerging international markets as a whole are outperforming even U.S. Equities over the past year.

Here’s a chart comparing the growth of the S&P 500 index to the iShares MSCI Emerging Markets ETF (EEM).

While the S&P has gained 17.56% over the past year, EEM grew 32.34%.

Rowe Wealth Management continues to maintain strong exposure to both Latin America and Asia Pacific equities.

I can remember when most U.S. investors I spoke with were not at all interested in International Stocks, especially emerging markets.

Investing abroad used to be much more of a valid concern. It was harder to trust foreign stock markets, back then. The U.S. financial markets were more heavily regulated. And International Stock markets were known for higher volatility than the U.S..

But investors are becoming more and more educated on how to reduce volatility. Investing in foreign countries has also become much safer over the last two decades.

In July, Rowe Wealth Management launched an International Model so that investors can capture gains from the strongest markets outside our borders.

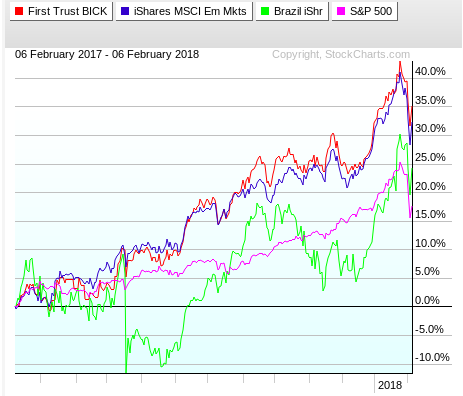

19.64% of our International Model’s funds are currently allocated to The First Trust BICK Index Fund (BICK), a Diversified Emerging Market fund with exposure to four countries: Brazil, India, China, and South Korea. The trend chart of this ETF remains positive, and has a strong fund score at 5.80:

BICK uses an equal weight allocation, so the countries in the index — Brazil, India, China, and South Korea — each represent 25% of the index at each rebalance.

The fund had a double top on January 2nd, and a long tail up on January 24 — two bullish chart patterns.

BICK has gained 32.93% in the past year, outperforming EEM by a hair — and with less volatility than a Brazil-only fund like EWZ.

Three out of four countries held by BICK fall into the Asia-Pacific Emerging sector, now the second-strongest sector within the International Equities asset class. While the fourth country, Brazil, doesn’t fit into our strongest international sectors by geography, Diversified Emerging Markets as a whole are extremely strong with regard to RS.

We continue to encourage our investors with an appetite for volatility and tactical allocation to explore the International Equity arena, but only the strongest parts, which by geography are Emerging Europe and Asia Pacific.

And looking at International Equities as a whole, ignoring which continent they’re on, we also see Relative Strength in Diversified Emerging Markets.

The U.S. Stock market won’t always remain the dominant asset class. In fact, as International Stocks grow stronger, they’re getting very close to beating the U.S. in terms of long-term relative strength.

Emotional trading is one reason investors underperform. Another is that investors always forget that the current trend will eventually end and a new one will begin. Don’t be one of those regretful investors.

As a relative-strength-based money management firm, we use studies to determine where to invest our clients’ capital.

There’s no emotion in the decision making process. There’s no “reason why” needed. We just find where the strength is, and we invest in it until the strength goes away.

We include tables at the bottom of every ADAPT issue to show the strongest asset classes, U.S. Equity sectors, and International Equities sectors, so you can see where the trends are. We encourage you to use these when making investment decisions.

To put our International Model to work in your accounts, schedule a consultation here.

Tags

Get Our FREE Guide

How to Find the Best Advisor for You

Learn how to choose an advisor that has your best interests in mind. You'll also be subscribed to ADAPT, Avalon’s free newsletter with updates on our strongest performing investment models and market insights from a responsible money management perspective.