Related Blogs

April 25, 2023 | Avalon Team

The U.S. housing market is beginning to show signs of slowing down, as affordability has become a key issue. This is the result of home prices growing way faster than incomes.

Recently, we’ve discussed the contracting credit impulse as well as the leading indicators that each point to softening in the U.S. economy.

Today, we’ll take a closer look at the U.S. housing market given its importance to economists and investors who closely watch it as a key indicator of the health of the economy.

Changes in the housing market can often serve as leading indicators of broader economic trends.

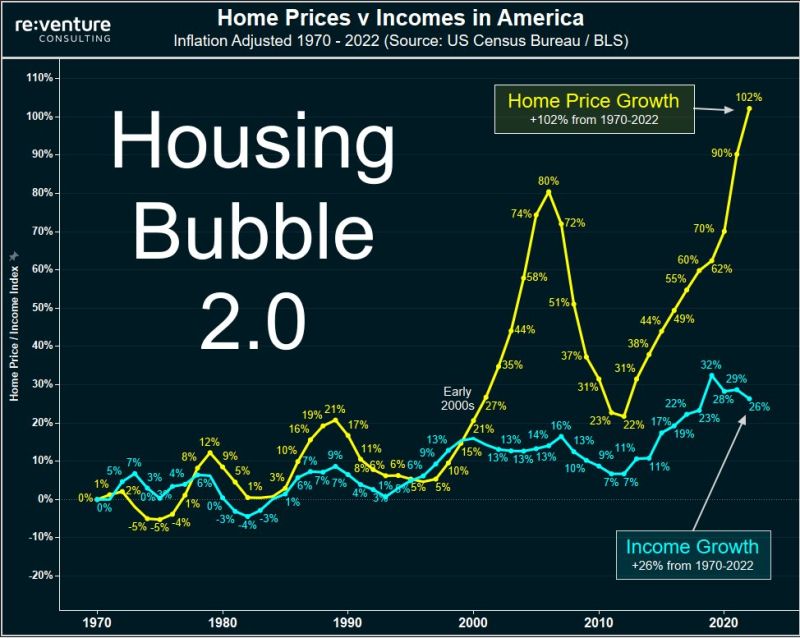

Let’s start off with the fact that home prices have been on an upward trajectory since 2010 and they now exceed levels of the housing bubble in 2005.

The housing bubble that popped with such devastating consequences in 2007–2008 was the result of the vast expansion of subprime mortgage lending, which began as a progressive goal of expanding home ownership to the lower-middle class by lowering credit standards.

This time around, the source of the bubble isn’t subprime buyers.

Today, there are a lot more strict rules and regulations around mortgage underwriting, and borrowers generally have more equity.

However, by keeping interest rates artificially low, the Fed has allowed mortgage applicants to borrow greater and greater amounts of money, which has led to an increase in demand, sending prices higher.

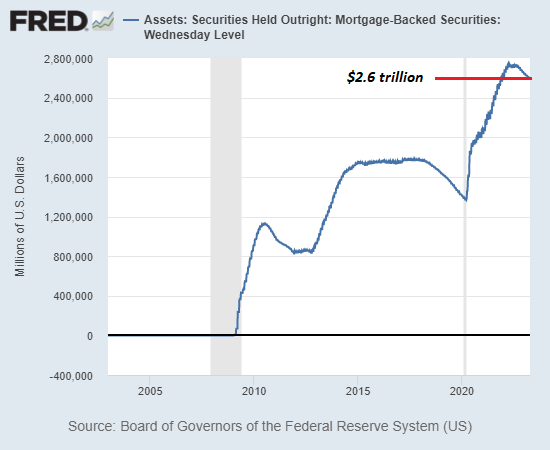

The Fed’s direct intervention can be seen here.

The Fed went from owning zero mortgage-backed securities (MBS) prior to the bursting of the first housing bubble in 2007–2008 to owning roughly 20% ($2.6 trillion) of the entire US mortgage market for conventional single-family homes ($13 trillion).

In effect, the Fed has been propping up real estate to maintain the “wealth effect.”

This has led to the second factor of the current excessive home price, which is wealthy investors and corporations are using “excess savings” and easy credit to snap up homes and rental apartments as “safe” places to park their excess capital.

Excess savings is in quotes because the “excess” money isn’t savings per se, it’s unearned gains generated by buying assets long ago at low rates of interest. As valuations soared, the wealthy owners of capital have been “burdened” with the task of where to park all these massive gains.

Real estate is a favored place to park “excess capital” globally, as it’s a stable, lucrative source of income via rents, typically has a lower risk profile than assets such as stocks, and typically increases in value as supply is inherently limited by geography and other factors.

The net result of these pressures to park excess capital in real estate is artificial scarcities in long-term rentals and “homes for sale,” jacking up rents and pushing valuations to the moon.

Finally, a third factor is the no-win situation that many homeowners are faced with.

Roughly half of the 50+ million home mortgages in the U.S. were refinanced in 2020 and 2021 to lock in historically low-interest rates of less than 4%, with many around 3%.

Think about it – why would a person sell and surrender a 2.75%, 3.00%, or 3.25% 30-year mortgage, only to move into another house with a loan at 5.5%–6.5%?

Many are locked into their house and loan for years, if not decades.

The artificially low rates of 2020–2021 have at least semi-permanently (and permanently in millions of cases) removed many millions of housing units from the market.

Indeed, one of the biggest challenges is the shortage of available homes for sale. According to recent data, the inventory of homes for sale in the U.S. is currently at a historic low, with only 1.2 million homes available for sale in March 2023. This shortage of inventory is causing bidding wars and driving up prices even further.

But the problem is that the price of homes has completely decoupled from income growth.

Since 1970, Real Home prices are up 102% but Real Income is only up a paltry 26%. Thus, it has only been the availability of artificially low rates and the rapid expansion of the Fed’s balance sheet post-Covid, that has allowed for the recent exponential growth.

But this may be coming to an end.

Distortions eventually have consequences and ultimately, all bubbles re-connect to reality.

One of the results of the SVB meltdown is that banks have become much more stringent in terms of lending. With both the rising costs of mortgages and the tighter lending standards, mortgage affordability/availability is diminishing.

And this means housing prices may be heading significantly lower.

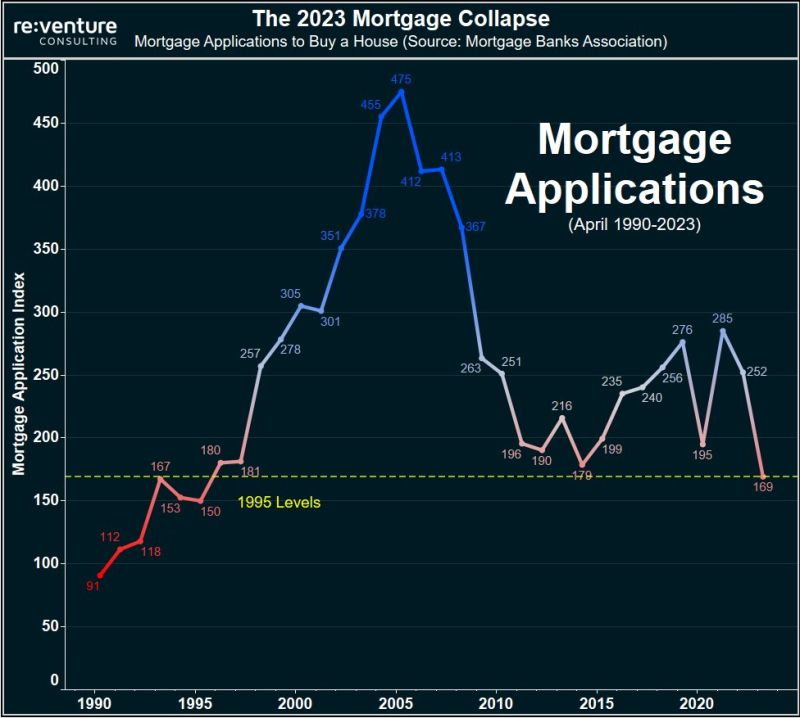

First, mortgage applications have just hit a 30-year low and are in the tank.

And housing affordability is now worse than it was in the early stages of the 2008 housing bubble.

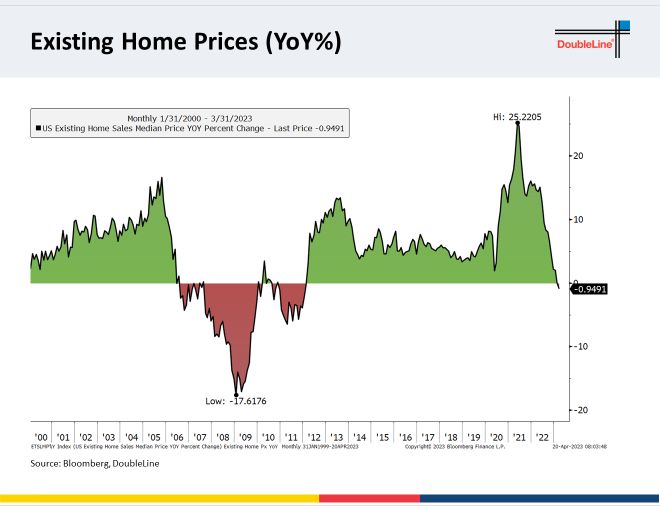

So it should be no surprise that the following graph shows Existing Home Prices have just recorded their first decline since January 2012 as the median existing-home sales price fell 0.95% from a year earlier to $375,700.

Once prices of houses and apartments start dropping, owners can no longer count on appreciation. Suddenly, a low-risk asset acquires a different risk profile: It’s losing value, not gaining value.

To lock into gains, the current owners will need to sell… but to whom?

And this suggests that other parts of the building and materials sectors will also begin to feel the effects too.

The next graph shows how commercial building activity normally follows the leading economic index with a several-month lag.

It is projecting lower.

And the volume of building material orders is now NEGATIVE in the first three months of 2023.

Since building materials like more housing-related series lead the economy, this suggests that future GDP is going to be weak.

In general, the Fed’s rate hikes have worked to cool the housing market, at least a bit.

But while buyers are seeing prices soften, there’s little inventory in many markets as sellers stay on the sidelines, worried it’s a bad time for properties to hit the market.

But, the real question is who’s left to buy overvalued houses?

Too few to prop up bubble valuations.

Bottom line?

The great imbalance between home affordability and current costs will probably be the catalyst that pops the current housing bubble.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.