Related Blogs

February 7, 2023 | Avalon Team

If there’s anything I’ve learned in my 30-plus years of following the markets, it’s that the market is going to do what the market is going to do.

Those who try to make sense of it will surely give up in despair at some point because there will be a time it defies conventional logic.

One of several reasons that I prefer managing money using a rules-based strategy is that the narrative doesn’t matter.

A good system will often spot the narrative well before it becomes obvious to the crowd. I simply follow the model output.

A recent example is how systems I run were beginning to select risk assets such as international stocks over U.S. stocks late last year, which we now know, has been the exact right call.

To onlookers, the performance of the U.S. market is a bit of an enigma.

Last week the Nasdaq Composite gained 3.31% posting its fifth straight winning week as it rode a tech-fueled rally to outperform the other major indexes.

Apple shares jumped 2.4%, reversing earlier losses after the company missed estimates on the top and bottom lines in its most recent quarterly report. iPhone sales, a key metric for the company, dropped 8% year-over-year to $65.8 billion, a meaningful miss from estimates of $68.3 billion.

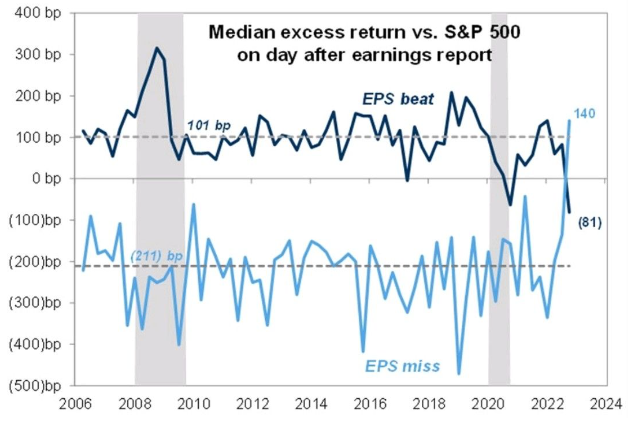

In fact, EPS misses are being bought so far this earnings season in a historic way with stocks outperforming 140 bps after a miss.

This is an all-time best performance dating back to 2006… stocks have literally never outperformed before on EPS misses. (Source: Goldman Sachs)

So the new normal is to reward poor performance?

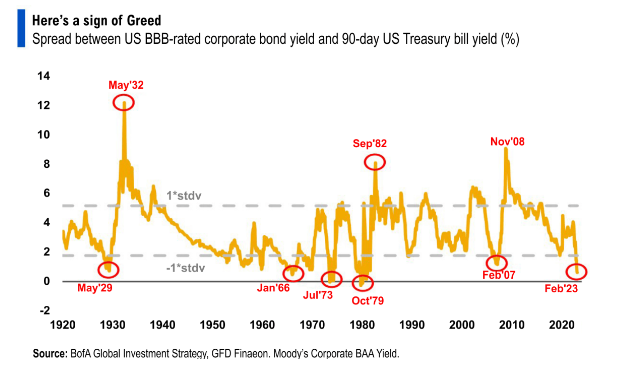

And investors’ bizarre behavior is not limited to stocks. The spread between corporate bond yields and T-Bills is near a record low implying that investors are earning very little risk premia.

This is not what one would expect if we are heading toward a recession where credit risks should increase.

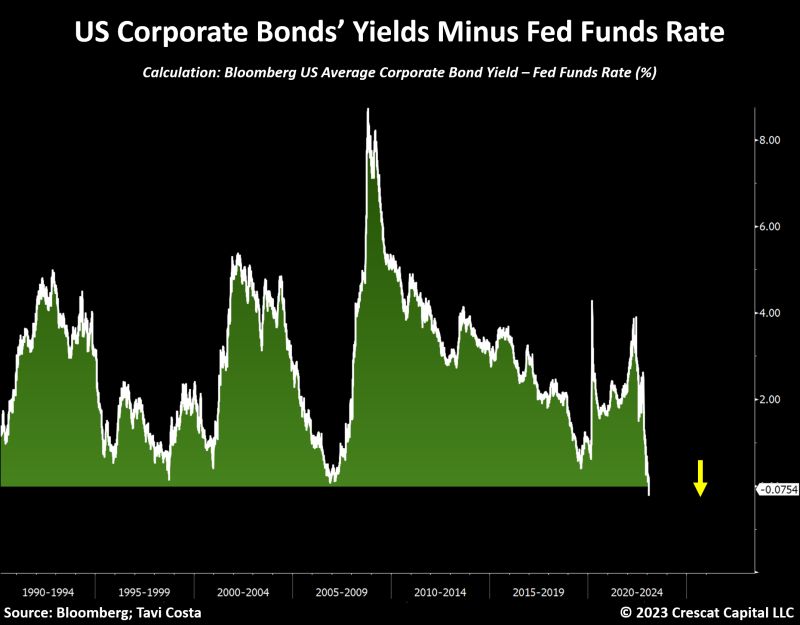

In fact, corporate bonds are now arguably, the most expensive part of the market as corporate bond yields are less than Fed Fund for the first time in 30 years.

Why is this happening?

Can You Smell the FOMO (Fear of Missing Out)?

Stocks have been on a tear to start 2023 as investors bet that weakening economic data will prompt the Federal Reserve to end its rate hiking cycle sooner than expected.

That view was bolstered by remarks from Federal Reserve Chair Jerome Powell last Wednesday who suggested signs of “disinflation” are building in the economy as the U.S. central bank raised interest rates by a smaller hike of 0.25% – even as he asserted more increases were ahead.

Old habits die hard.

It is difficult to break the psychology of market participants who have been conditioned to buy the dip without consequence for the last 15 years. So, in that respect, I’m not surprised the market is rallying despite the economic reality.

When you constantly have somebody at the ready to bail out the market the first half second one person feels discomfort, it creates a foundation of irrational expectations from investors, namely that things are always better than they seem.

In 2019, the Fed pivoted hard and the economy managed a proverbial soft landing. The 2018 hiking cycle which Powell abruptly reversed with his early 2019 pivot slowed the economy down, but not nearly enough to result in a hard landing.

But 2023 isn’t 2019.

The reality is that we have just experienced the greatest and longest period of monetary recklessness in history. How could it be followed by a soft landing?

As the era of QE and ZIRP unfolded, policymakers have attempted to solve the problem of debt… with more debt. By the way, this was tried very unsuccessfully in the 1920s.

When central bankers become rock stars, as they have now, you know it will end badly.

As Peter Drucker said: “The heroes of the boom become the villains of the bust.”

The central bank policies of the past did well at the time to defer the risk of the present into the future, but the future is now. Now we must deal with the record amount of government and corporate debt.

And when rates were at or near 0%, it was easy to continue to kick the can down the road. But when rates are 4-5%, the cost of money becomes an impediment to future growth.

Powell pronounced that “we are going to become data dependent” and the market immediately FOMOed everything as if a soft landing is all but guaranteed.

But as I often say, context is everything.

In 2019, the Fed managed a soft landing with risk-free rates of around 0%. Today, rates are positive and the Fed has had to keep rates tighter for longer.

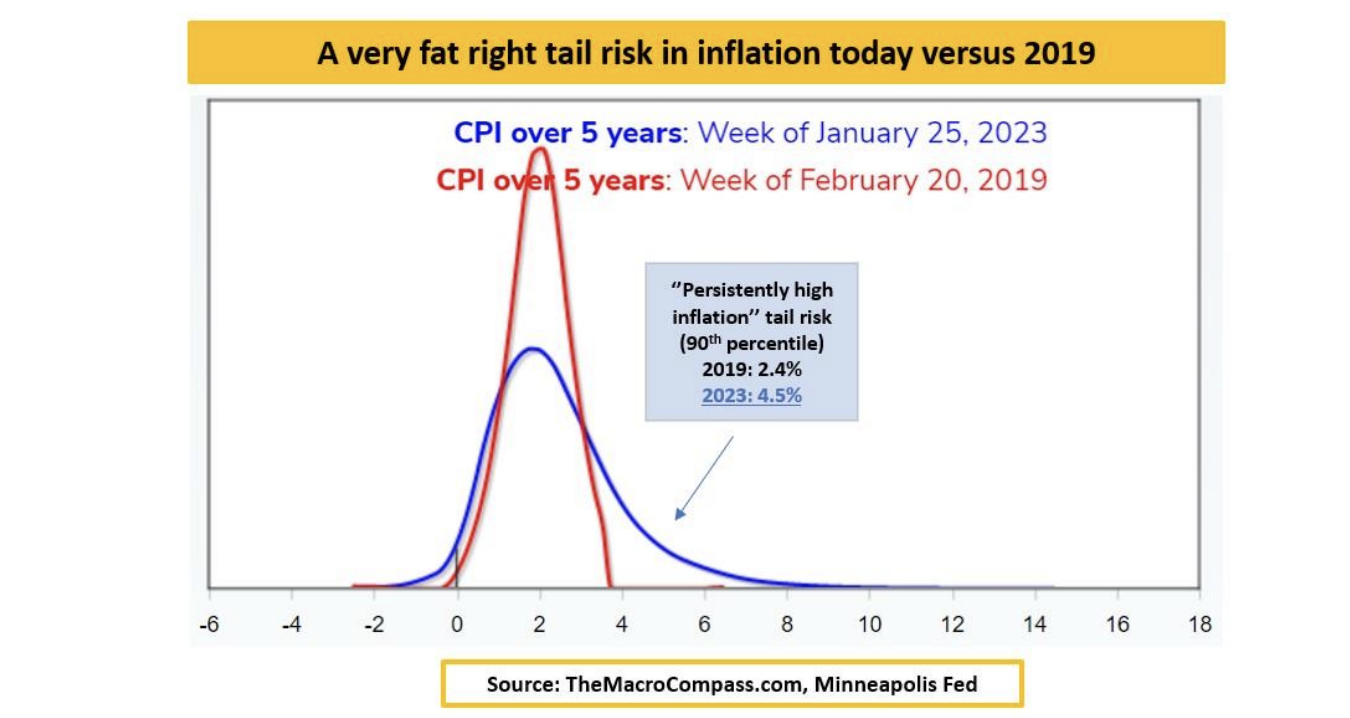

Further, there is no assurance that inflation will reach the target zone of 2-2.5%.

Contrary to 2019, today’s markets still price a 10% chance that on average CPI will print at 4.5% in 2023-2028! Such a fat tail for upside inflationary risks limits the Fed ability to pivot. Loosen financial conditions too much, and the risk of a second bout of inflation dramatically increases.

In 2019, an early pivot made sense. Today, from a risk management perspective an early pivot is a poor decision.

Powell’s credibility is all about staying the course and keeping at it.

Animal spirits are the worst enemy of a Central Banker trying to get inflation under control. Powell’s priority is to manage these risks, not to validate market and economic euphoria.

Investors are pricing in La-La Land.

- Inflation back to 2.50% in 9-12 months,

- Fed cutting to 2.75% and real yields back to zero in 18-24 months,

- Tighter credit spreads; and

- Lower implied volatility.

Basically, an immaculate disinflation with no recession. History teaches us that’s a low probability event: over the last 100 years, lowering inflation by 6-7 percentage points always required a recession.

No recession? Ok, but then it means a tighter Fed and more volatility ahead.

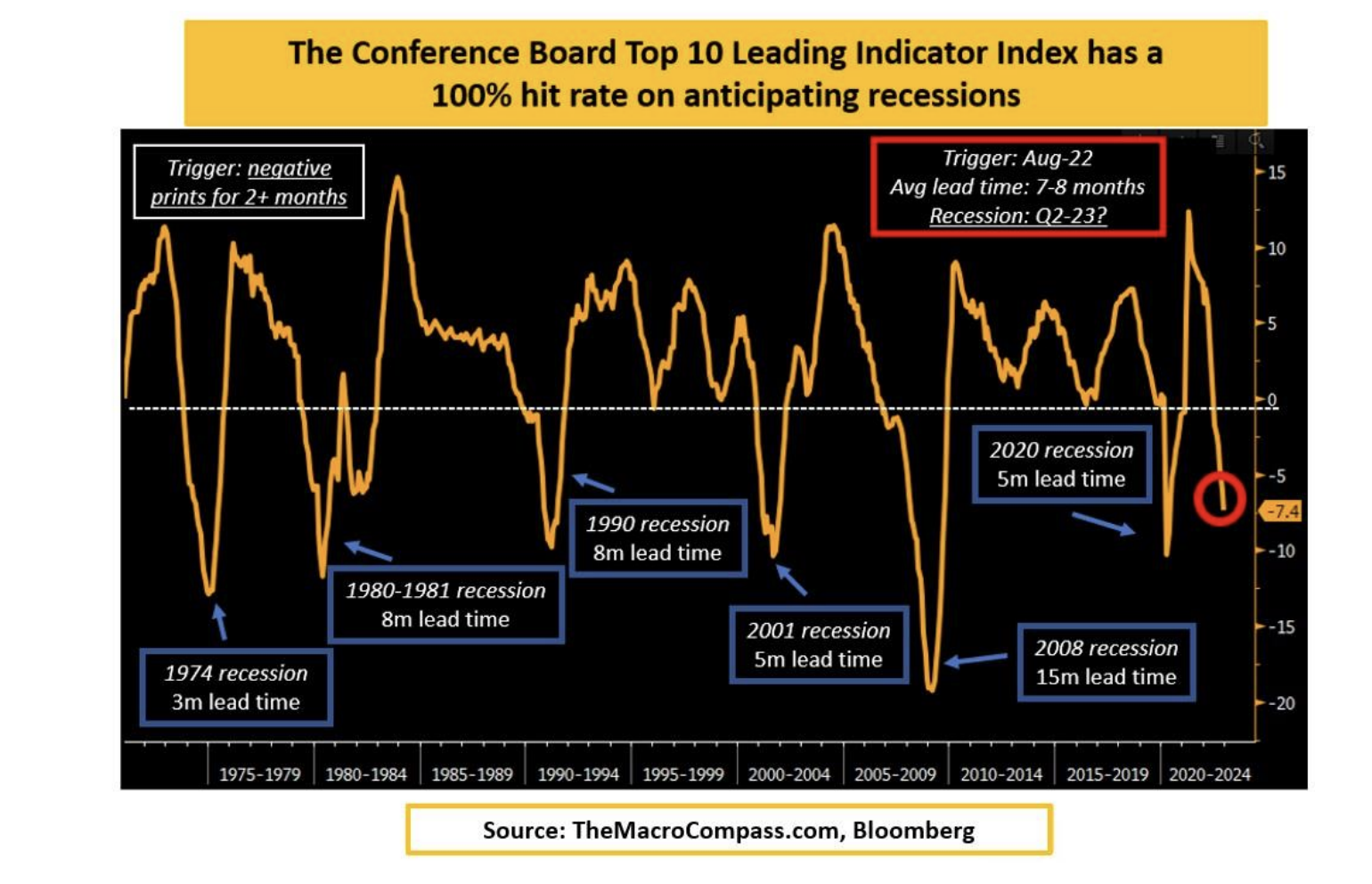

With 100% hit rate, the Conference Board Leading Indicator Index is still anticipating a recession.

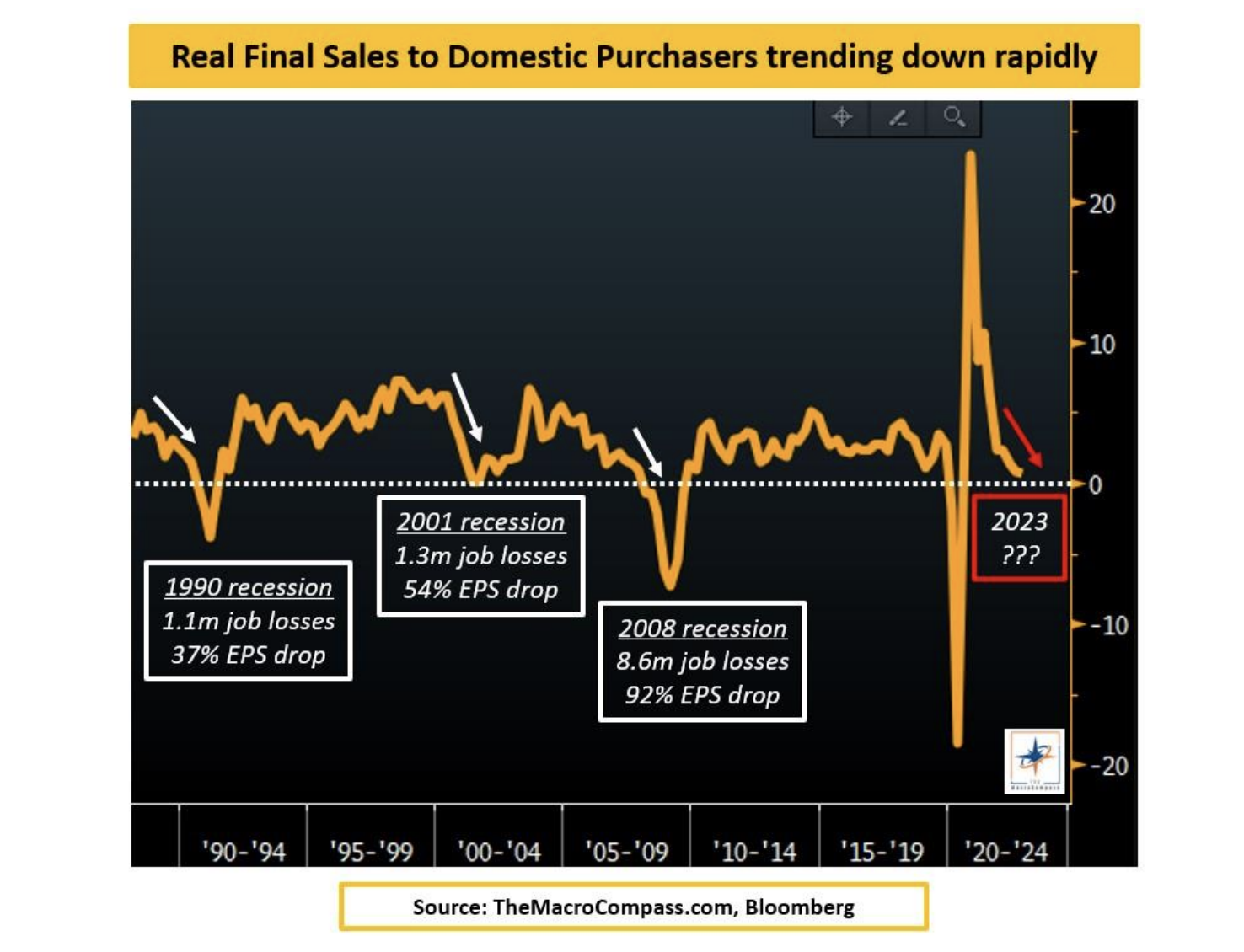

There is more hard data is showing clear signs of deterioration now.

Real sales to domestic purchasers are an effective way to assess the strength of US consumer demand, as they strip away inventory boosts/drags, government net spending and volatile net trades.

This core component of US GDP growth is rapidly trending to zero.

I would caution investors not to chase the current rally as the market may be getting ahead.

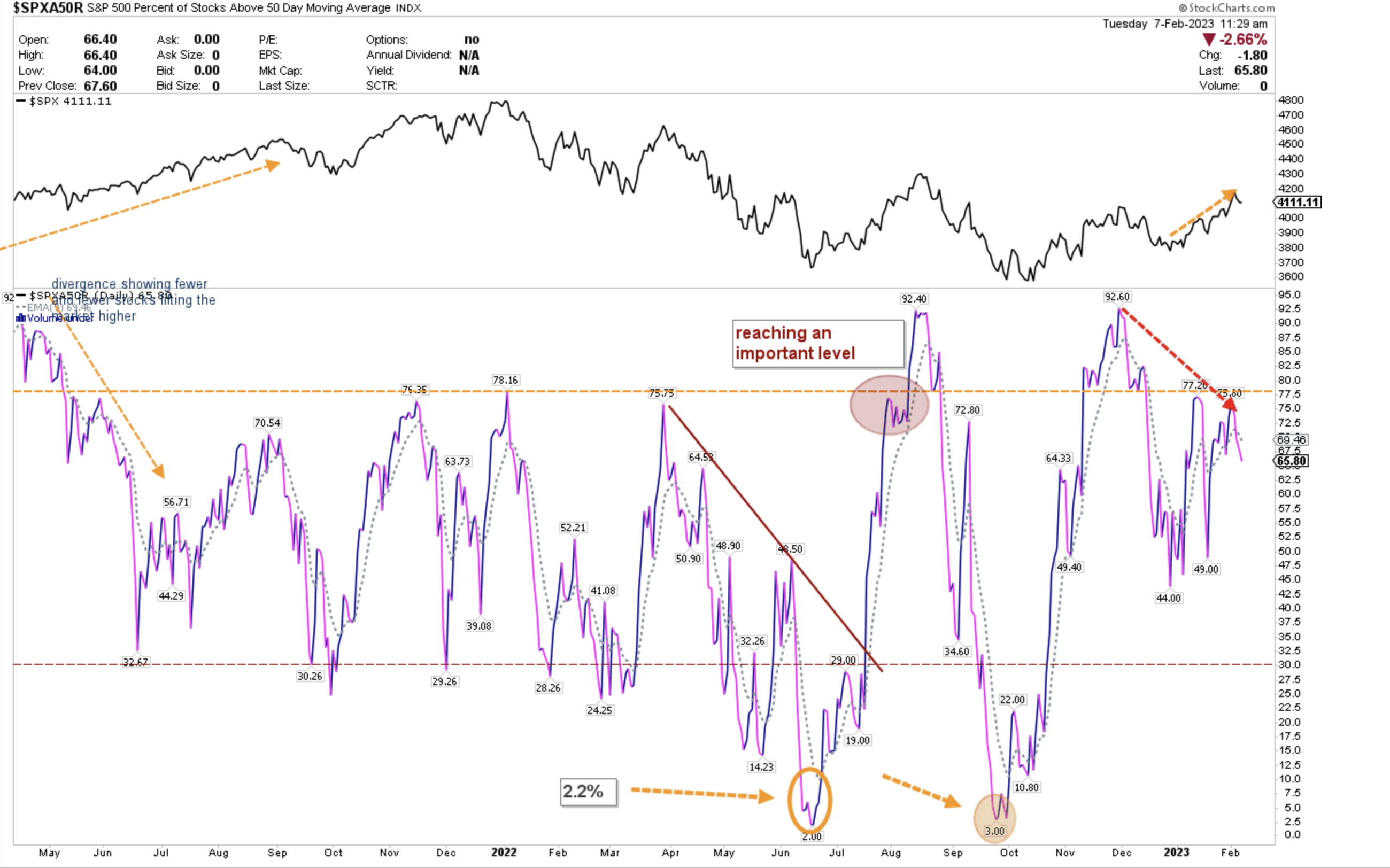

Internally, I am seeing some evidence of deterioration of the quality of the trend. Take for instance the Percentage of Stocks Above their 50 Day Moving Average. It has been slipping while the market was making recent highs creating a divergence.

For now, this is a yellow caution light.

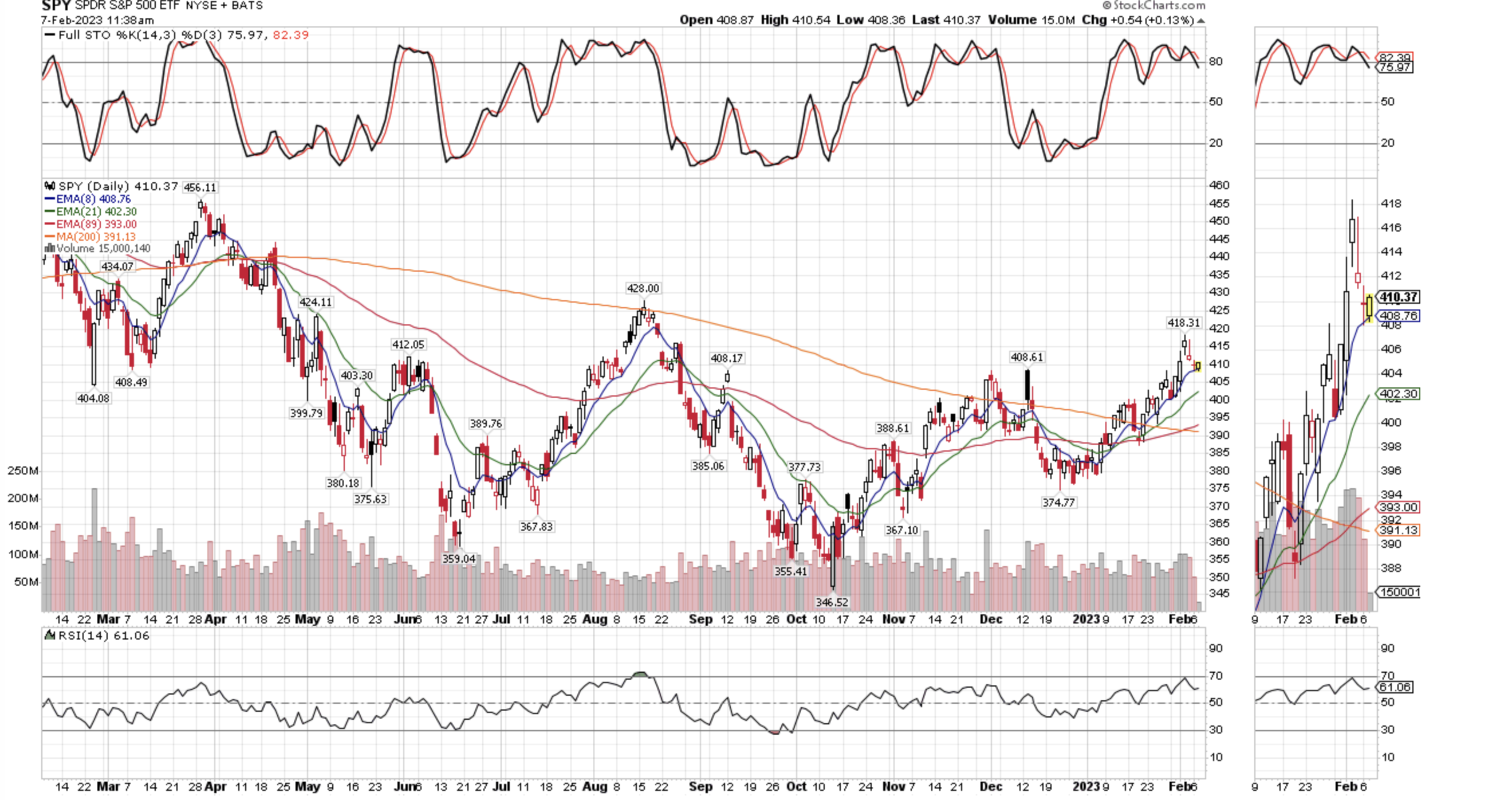

At the current time, the trend remains positive in the general market with price above all key moving averages. It would take a close back below the recent breakout levels to turn the tape decidedly bearish.

But do note that the yield on the 10-Year has not convincingly reversed lower. This is definitely something to watch as an increase would not be helpful to stock prices.

While the current phase of the market is rewarding bad news as good on the hopes of the fabled “soft landing,” investors would be wise to heed caution.

Soft and hard data continue to point to macro conditions that do not favor investors taking aggressive risks.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.