Related Blogs

January 25, 2024 | Avalon Team

According to the Natixis Investment Managers global survey of individual investors, investors expect over 12% after inflation.

Expectations versus reality… quite the divergence.

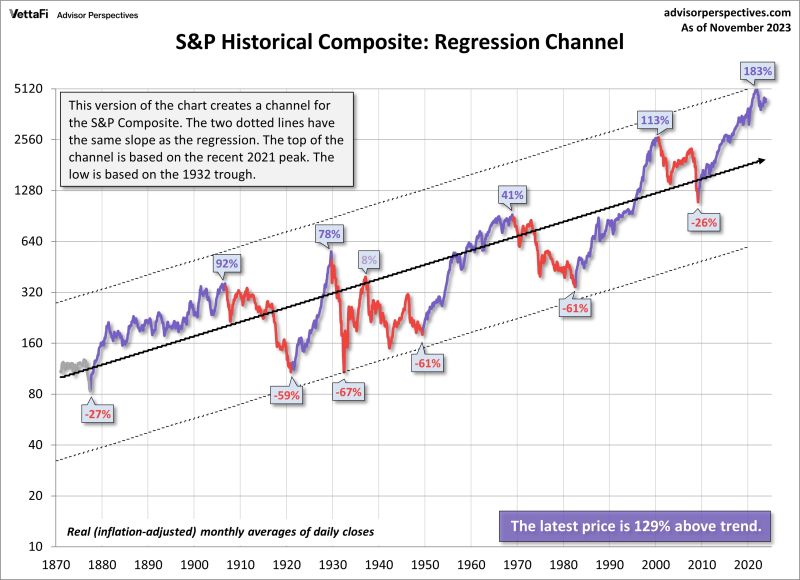

Since 1871 (Shiller Dataset) after inflation, the S&P 500 has compounded at around 7% with several 60%+ drawdowns historically.

Because of how well the market has done LATELY, it’s easy for investors to suffer from “recency bias” and fail to understand the historical perspective.

The performance of the past 10-15 years has reinforced in investors’ minds that stocks don’t go down (and if they do, they don’t go down too much or stay down for too long).

History says otherwise and the idea of 12% after inflation is a fantasy reflective of a prime example of irrational exuberance and cyclical retail market participation.

I believe this message is extremely relevant given how far the current market is above its historical trend and given how the returns have become concentrated among a small handful of mega-cap stocks.

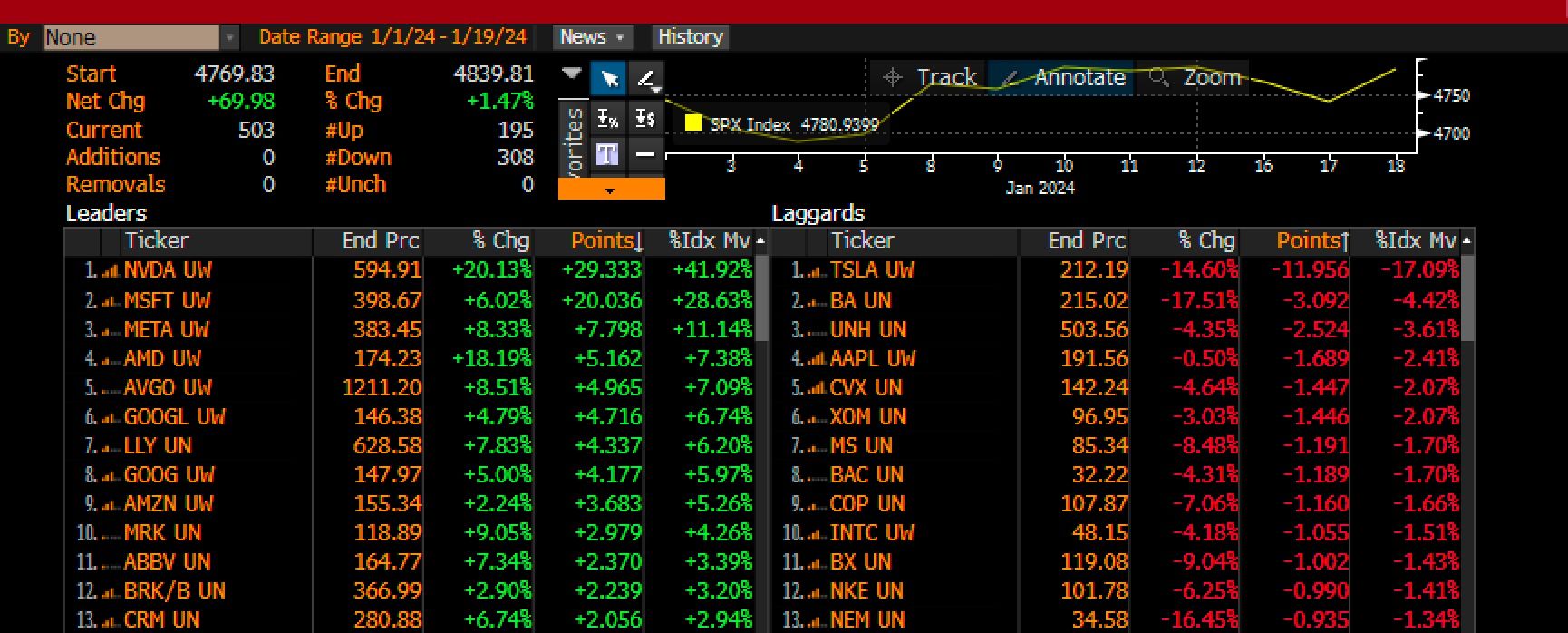

Last year the Magnificent Seven were responsible for 76% of the S&P 500 gain. And this year, the concentration has become even greater.

Year-to-date until last Friday’s close, Nvidia was responsible for 42% of the S&P 500 upward move, Microsoft 29%, and Meta 11%. That is 82% of the index’s upward move.

The S&P 500 is up 1.47% YTD, hitting its record high levels, which it was at in Q4 2022.

Meanwhile, the equal-weight S&P 500 is -1.25% for the same period.

Speaking of the Magnificent Seven, is it now the Magnificent Six as Tesla seems to have left the party?

Last night, the company reported a miss on earnings which has sent the stock price lower, now down -25% YTD.

Tesla warned of a lower growth rate this year because of price cuts in 2023 impacting profits.

The bulls are capitulating and the share price looks as though it could head much lower.

Some of the current enthusiasm for stocks has been based on investor expectations for a “soft landing” where the Fed begins to lower interest rates and earnings rebound.

Once again, reality paints a different picture.

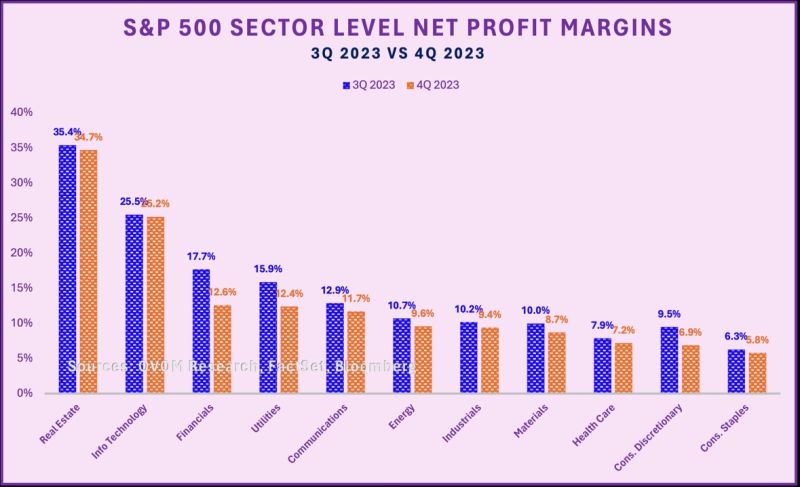

All 11 of the 11 segments in the S&P 500 are observing a quarterly net profit margin % decrease.

Fundamentals are transparently breaking down and we are still in the early stages of the “higher for longer” Fed regime.

Risk assets are not priced for a potential economic disappointment as some keep insisting, they’re priced for a robust earnings rebound.

Sadly, this is crystal clear evidence that this shouldn’t be the baseline expectation.

Finally, today’s report on GDP, a measure of all goods and services produced, showed an increase of 3.3% annualized, well above the Wall Street consensus of 2%.

The expansion was driven by strong consumer spending and government spending.

While so far there has been little reaction in the bond market, good news is bad news for those hoping that the Fed eases rates sooner rather than later.

Time will tell how long the economy can continue to show such resilience.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.