Related Blogs

February 2, 2024 | Avalon Team

This has been a busy week with both earnings reports from Big Tech and a FOMC meeting. In today’s issue, I walk you through the week’s biggest highlights and what it could mean for investors.

Let’s start with Federal Chairman Jay Powell. On Wednesday, Powell stated that the Fed is not going to lower interest rates this month and is unlikely to do so in March as well.

“Inflation has eased from its highs without a significant increase in unemployment. That’s very good news,” Powell said. “But inflation is still too high and ongoing progress in bringing it down is not assured—and the path forward is uncertain.”

The Fed’s comments are interesting for one very simple reason: The Fed’s favorite indicator for inflation is not CPI, but PCE (Personal Consumption Expenditures) for which the Fed’s target is 2.0%.

Here is a chart of PCE inflation year over year (YoY).

On January 26th, Core PCE was reported at 2.9% for the full year. This now puts the six-month annualized PCE at 2.0% and the six-month annualized core at 1.9%. (Core PCE is PCE but excludes food and energy, which are driven by commodity prices and are not within the purview of monetary policy, per se.)

It would seem as though the Fed is just inches from achieving its stated goal.

Is the biggest risk now that the Fed reacts too slowly on the way down, just as they failed to recognize how the inflation genie had left the bottle on the upside?

For a market that had been pricing in rate cuts, this came as a disappointment sending stock prices lower.

Stocks were already weak after earnings reports from AMD, Google, and Microsoft failed to impress investors on Tuesday. The hawkish tone of the Fed just added more reasons for sellers to emerge.

Regarding equities, the Nasdaq futures were pounded, dropping -346.25 points, while the S&P 500 fell -80.50, the Dow -332 points, and the Russell 2k, the weak link, dropped 2.5% losing -50 points on the day.

However, the reaction in the bond market was anything but as expected, as yields plummeted all across the yield curve.

As an example, the yield on the Ten-Year U.S. Note fell from 4.10% to under 3.70% now placing the daily trend in rates again lower.

Either, (a) the bond market doesn’t believe Mr. Powell or (b) some things are going on behind the scenes that have yet to become apparent.

Two things that come to mind are the rising geopolitical risks and what seems to be an announced escalation of tension and war between the United States and Iran. Or, there is something close to breaking in the system and smart money is front-running to safety.

Along those lines, we learned this week that New York Community Bancorp posted a troubling quarterly report as Q4 results showed a massive 796% QoQ increase in provisions for credit losses.

This bank could be a tell on other banks as this is the parent company of Flagstar Bank, the very bank that took over all the assets and liabilities of Signature Bank during the March 2023 banking crisis.

It shouldn’t be too shocking as investors have known for over a year that there is trouble in MF and CRE loans and banks are taking large write-downs. NYCB’s loan book is made up of 56.4% of these types of loans.

Not only did NYCB shares get hammered, dropping by over 50%, but investors quickly dumped other regional bank shares as well as the chart of the S&P SDPR Regional Banking ETF (KRE) shows.

Whatever the case, gold has caught a bid and is now pressing its highs and looks quite bullish.

What many investors may not realize is that gold has also been doing well on a relative basis versus stocks for the last several years.

While much of the attention has been focused on AI and stocks, gold has been improving its relative performance since the beginning of 2021.

Now back to earnings.

On Thursday, Amazon (AMZN) reported earnings, and they were excellent.

Free cash flow (FCF) blew out estimates and the operating margin in North America was nearly 40% higher than estimates, all while the largest cloud service provider in the world (Amazon Web Services – AWS) reaccelerated growth again, and the advertising machine puts GOOGL to shame.

The company delivered its highest quarterly operating income ever and noted that it expects AWS revenue growth rate acceleration to continue as customer cost optimization efforts have “attenuated significantly.”

Shares of AMZN are trading higher in the pre-market (as I write this) and are close to ATH levels last seen in 2021.

Meta Platforms (META) also reported. It announced a tripling of profits in the fourth quarter and issued its first-ever cash dividend.

The 25% gain in revenue for the quarter was the fastest rate of growth for any period since mid-2021, but more impressive is that net income tripled to $14B, up from $4.65B a year earlier, reflective of the company’s ability to cut costs.

Shares are set to trade at ATH today.

Price action in the major market-cap weighted averages appears positive with the Nasdaq 100 and the S&P 500 trading at ATHs. However, beneath the surface, I want to call attention to the diminishing number of positive sectors.

Back on January 2, 43 sectors were controlled by bullish demand.

One month later, with the S&P 500 nearly 3% higher and the Nasdaq 100 close to 5% higher, the number of positive sectors has declined to just 19.

I hate to throw cold water on the market bulls, but this is not supportive and waves a big yellow caution flag to me.

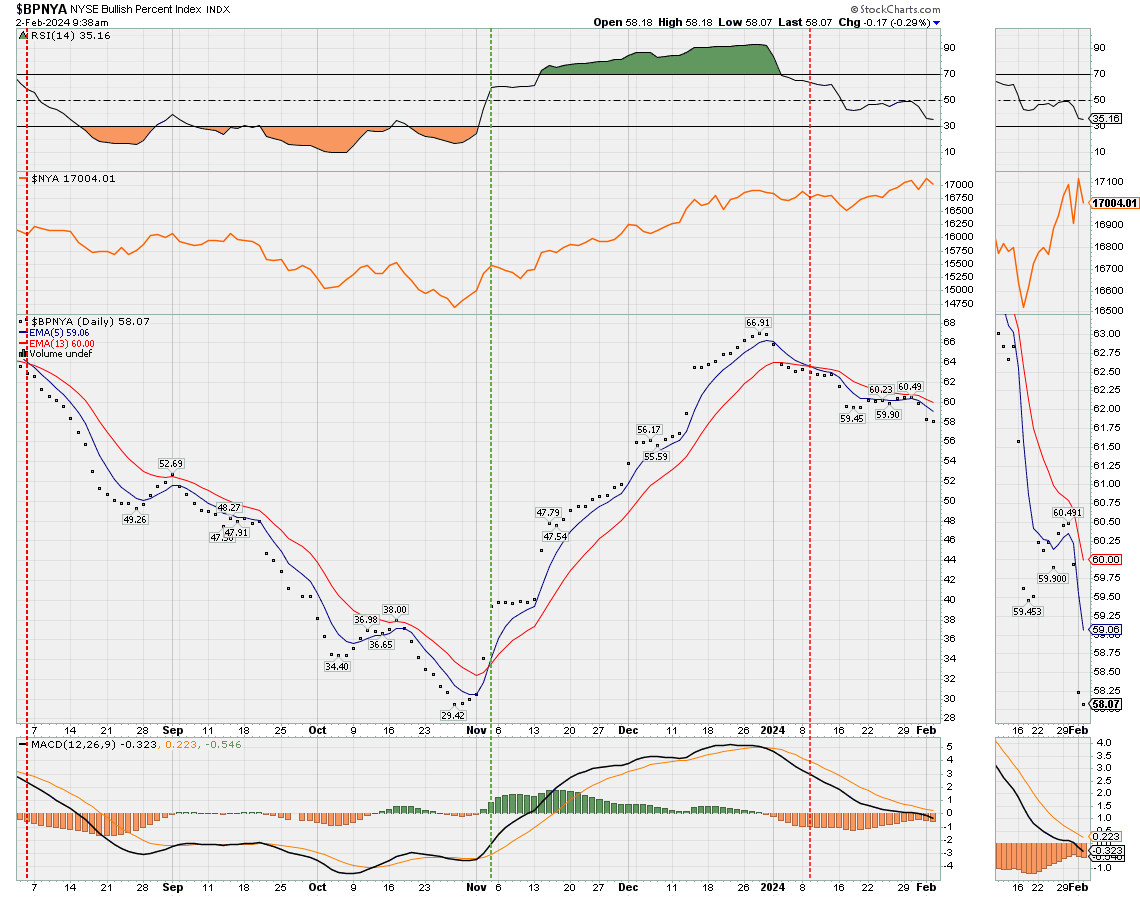

Among other market breadth indicators I follow, the NYSE Bullish Percent is also beginning to accelerate back to the downside after a brief pause.

In my experience, the major market averages ultimately reflect the direction of market internals such as breadth and participation.

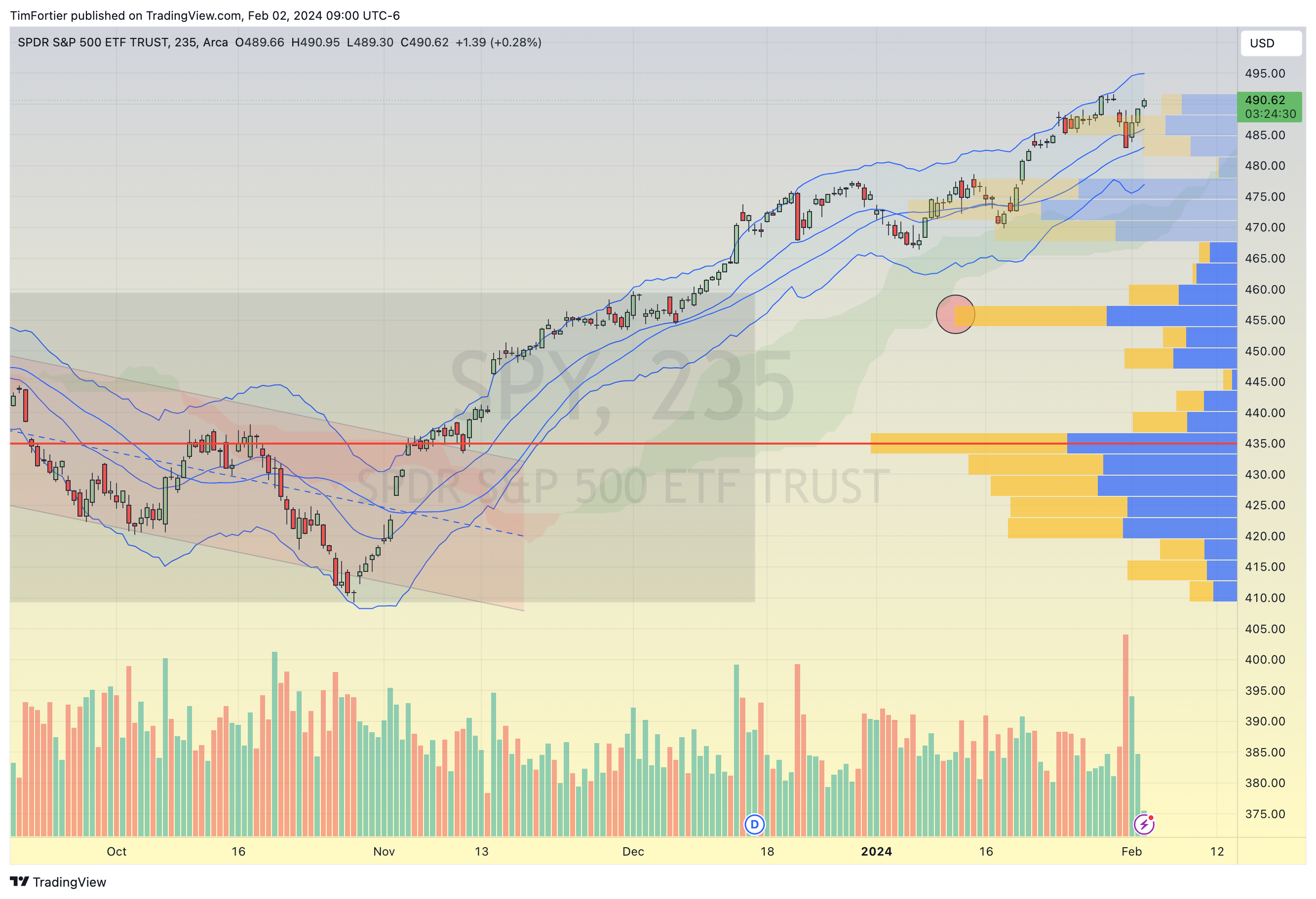

For now, the trend of the S&P 500 SPDR (SPY) remains positive, with expected support in the $477 region.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.