Related Blogs

June 30, 2023 | Avalon Team

This week marks both the end of the quarter and the mid-year mark for the financial markets.

It’s the perfect time to see where we have been and where we may be heading.

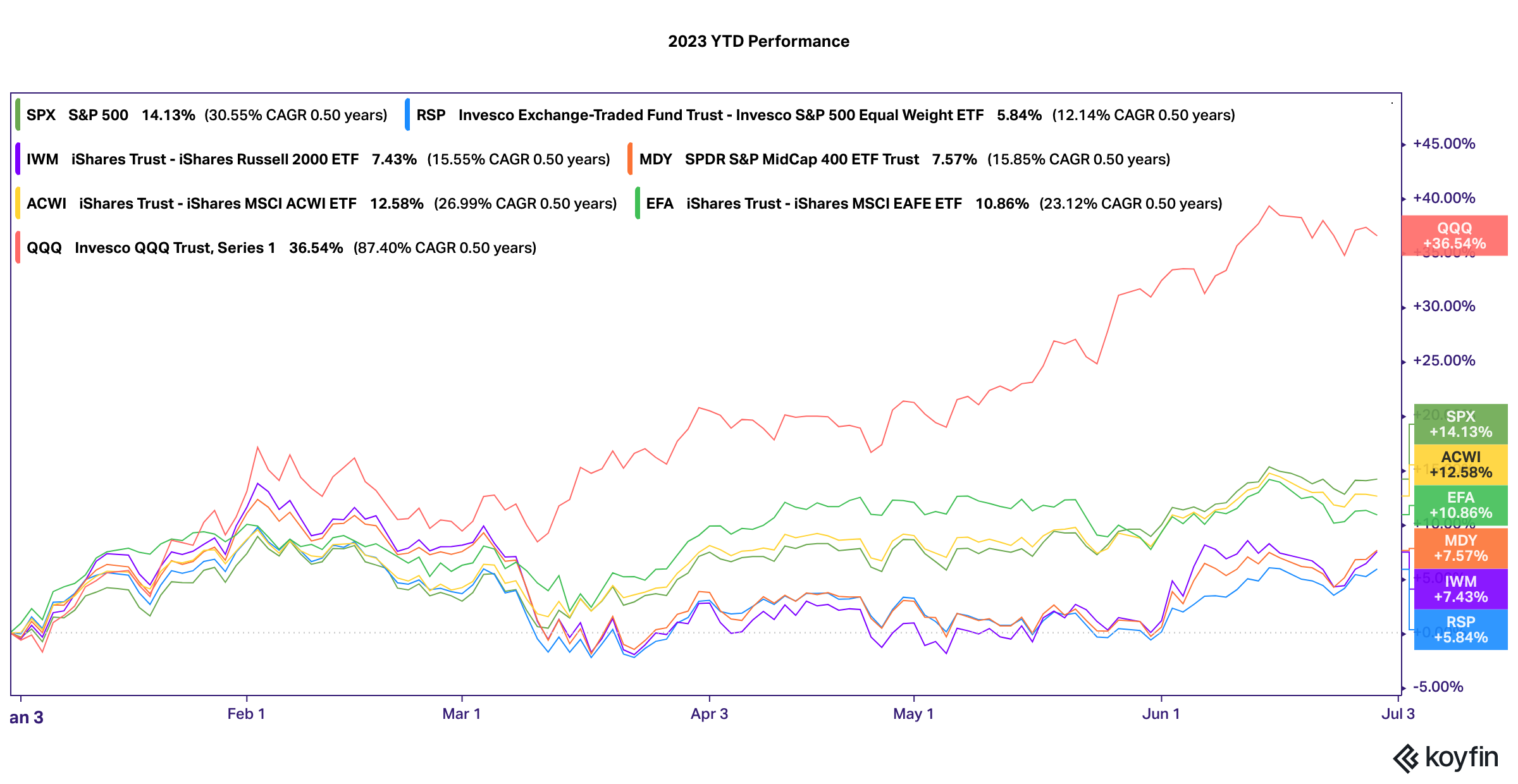

First is the scorecard.

This is no secret for our ADAPT readers, but 2023 has been mostly about technology and AI in particular.

The technology-laden QQQ has so been the standout winner with performance measured in multiples of the other dominant indices.

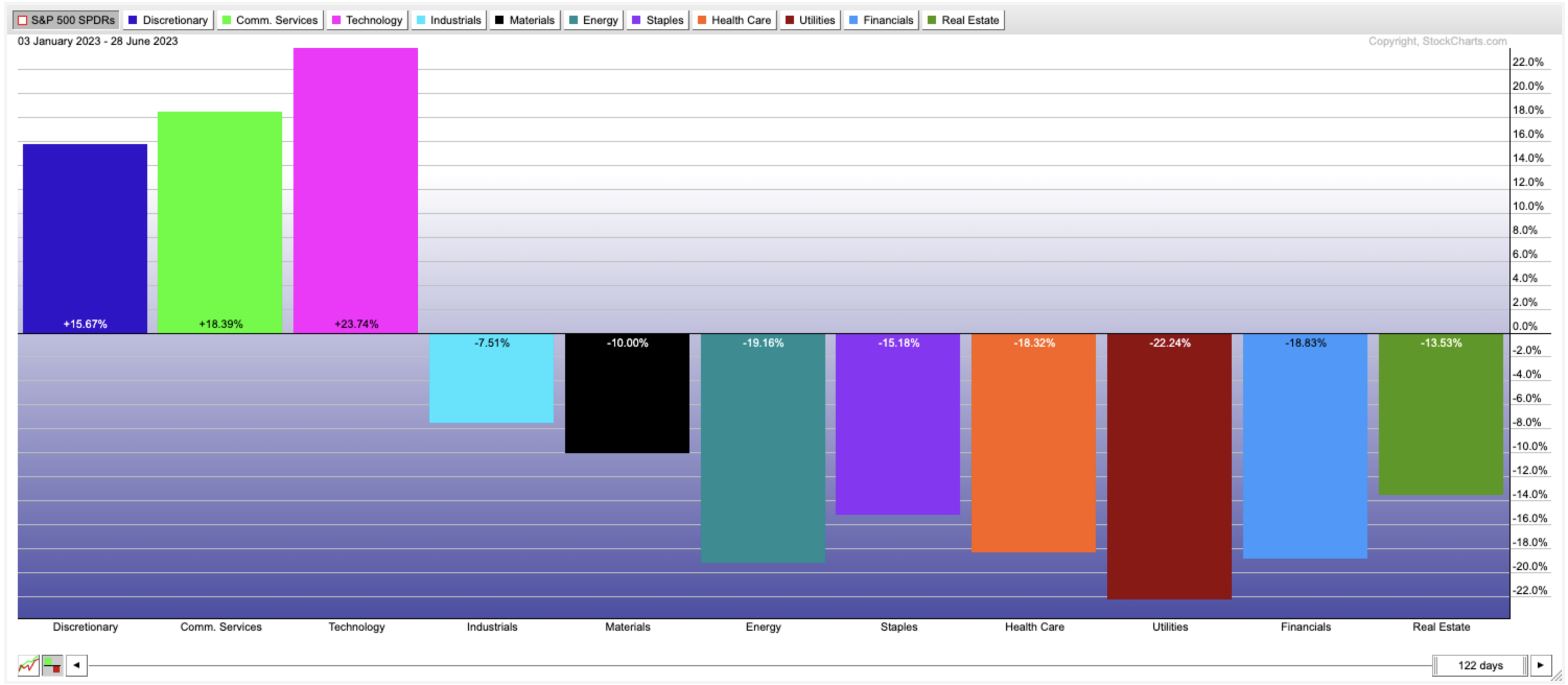

In fact, only 3 out of 11 major sectors are positive on a YTD basis.

The narrow leadership in U.S. equities, driven by quality mega-cap names in the Tech sector, has intensified. It raises questions about the sustainability and durability of the rebound.

Additionally, the valuation for the current leaders looks stretched by almost every measure.

Consider this year’s tech darling NVIDIA. It trades at 233 times earnings and 41 times sales.

A valuation of 41 times sales means that the company must return every penny of revenue (not profit… but sales) to investors for 41 years to justify its valuation.

That’s 41 years of revenue forked out to investors. Insane, right?

Here is a look at the big winners from the first half:

- VDA +193%

- META +133%

- TSLA +111%

- AMD +85%

- CRM +60%

- ORCL +54%

- AAPL +43%

- MSFT +43%

- GOOGL +40%

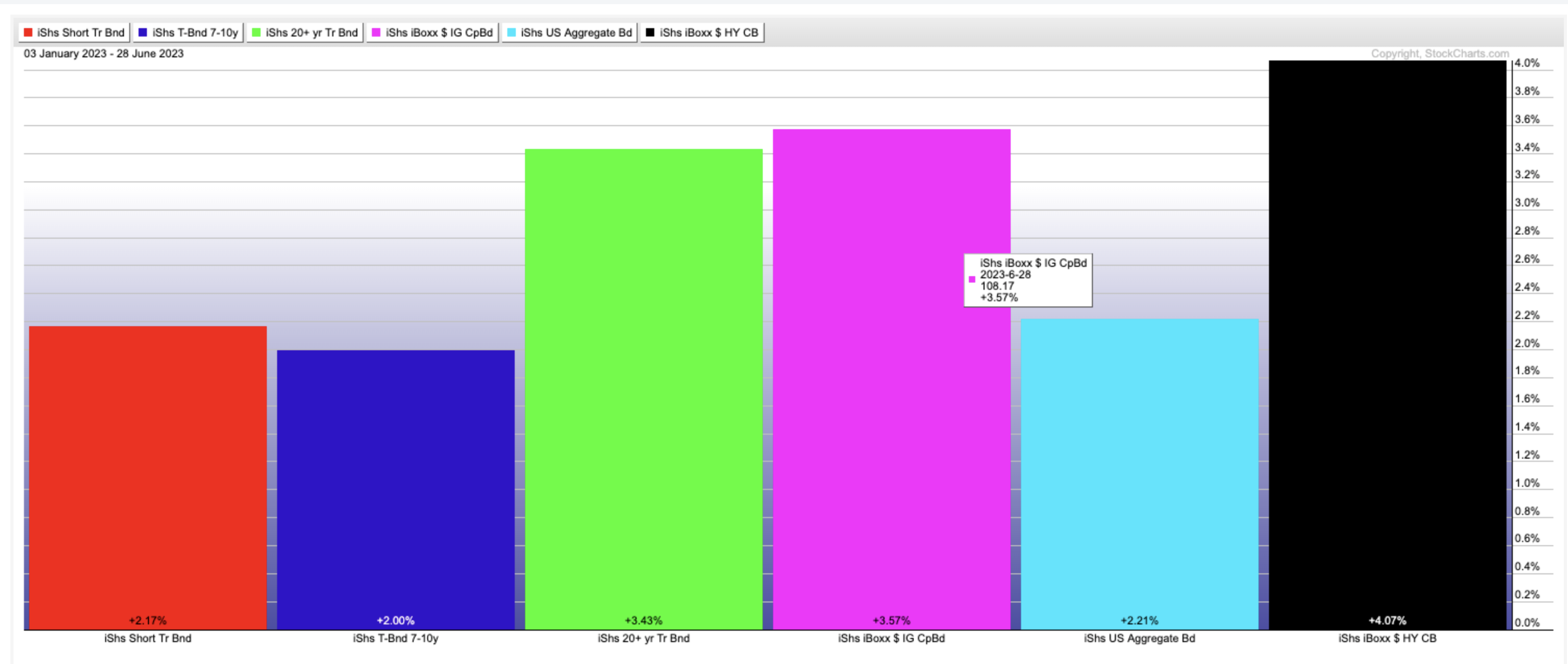

Fixed Income

After suffering some of their worst-ever losses in 2022, bonds are having a better year albeit the returns have so far been subdued. The Aggregate Bond Index, often used as the benchmark for bonds, is up 2.21% YTD, in line with other popular bond benchmarks.

High-Yield bonds are the best performing with a return of over 4% YTD.

Bonds are currently caught between two narratives.

The positive is that inflation, as measured by CPI, is now about half of what it was a year ago, providing bond investors with an opportunity for a positive real rate of return.

But on the other hand, core inflation has remained stubborn, and as a result, Fed Chairman Powell has indicated as recently as last week, that more rate hikes might be necessary.

This has (and will likely to continue to) dampened any bond rallies.

So what does the second half have in store?

Historically, a strong first half often leads to strong performance in the second half as well.

Let’s crunch the U.S. stock data for the past 95 years. When looking at the past 95 years there have been 28 times U.S. stocks have been up +10% or more in the first 6 months of the year.

Of those 28 years, 22 years were positive, delivering a second-half return of ~6%.

But before I get too far ahead of myself, let’s take a look at my forecasts from late December of last year.

My first forecast was that Central Banks remain hawkish and interest rates remain high.

Check.

Federal Reserve Chair Jerome Powell has recently said that they expect the need to raise interest rates at least twice more by year-end with U.S. inflation well above the 2% goal and a labor market that’s still very tight.

The Fed is especially focused on Services inflation ex-Shelter, and the PCE-equivalent shows that is very much stuck at high levels…

For this reason, rates will likely stay higher for longer.

My second forecast was that Valuations are “fair” but not cheap.

Check again. But now they are no longer fair and have once again gotten expensive.

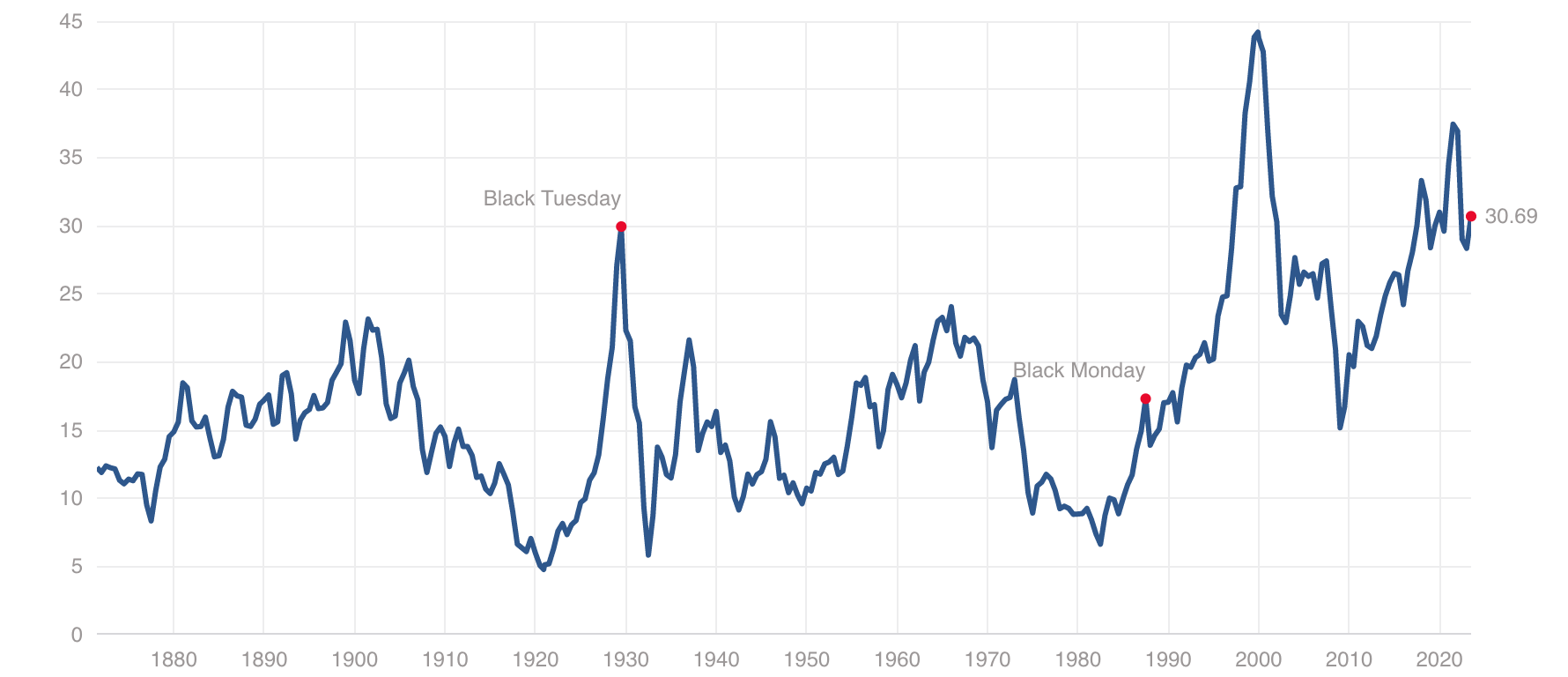

The current CAPE Shiller P/E (Price earnings ratio is based on average inflation-adjusted earnings from the previous 10 years,) ratio is 30.69 which is high by historical standards and twice the median average.

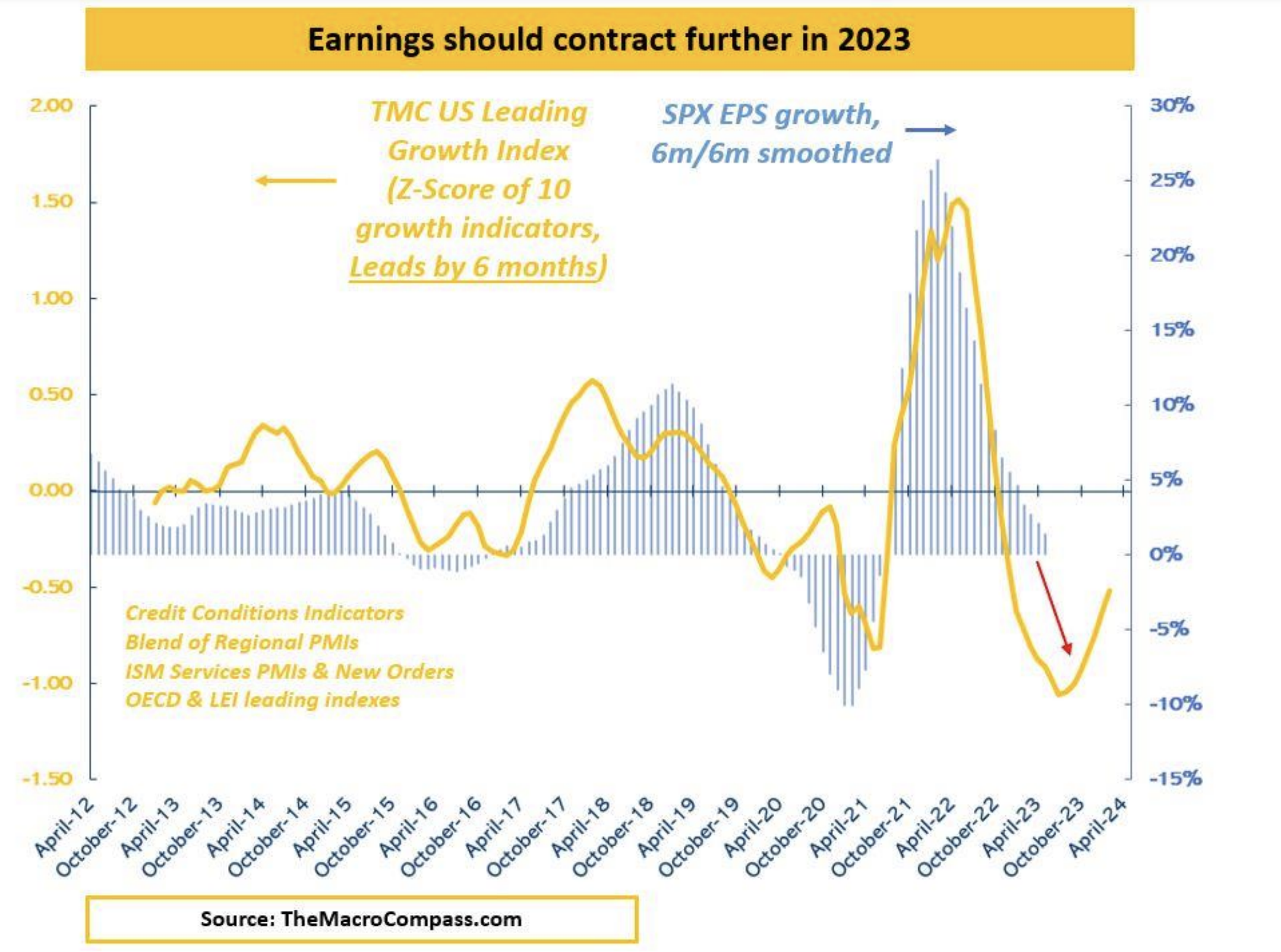

Additionally, it remains expected that earnings growth will contract in the coming months as a result of sluggishness in manufacturing and the increased costs to finance.

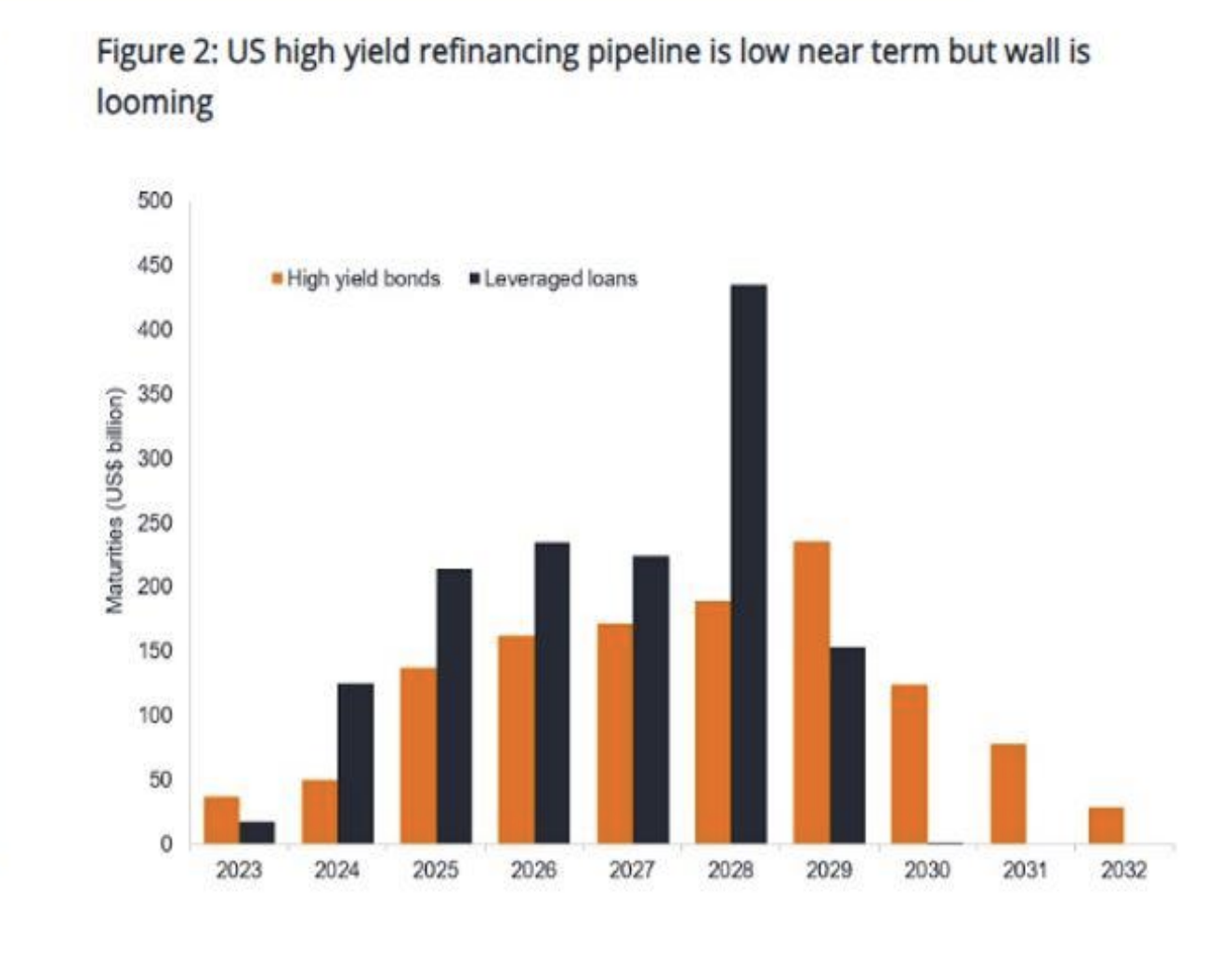

While many companies are locked into lower rates, a wall of refinancings will begin next year that could prove costly and begin to reduce operating margins.

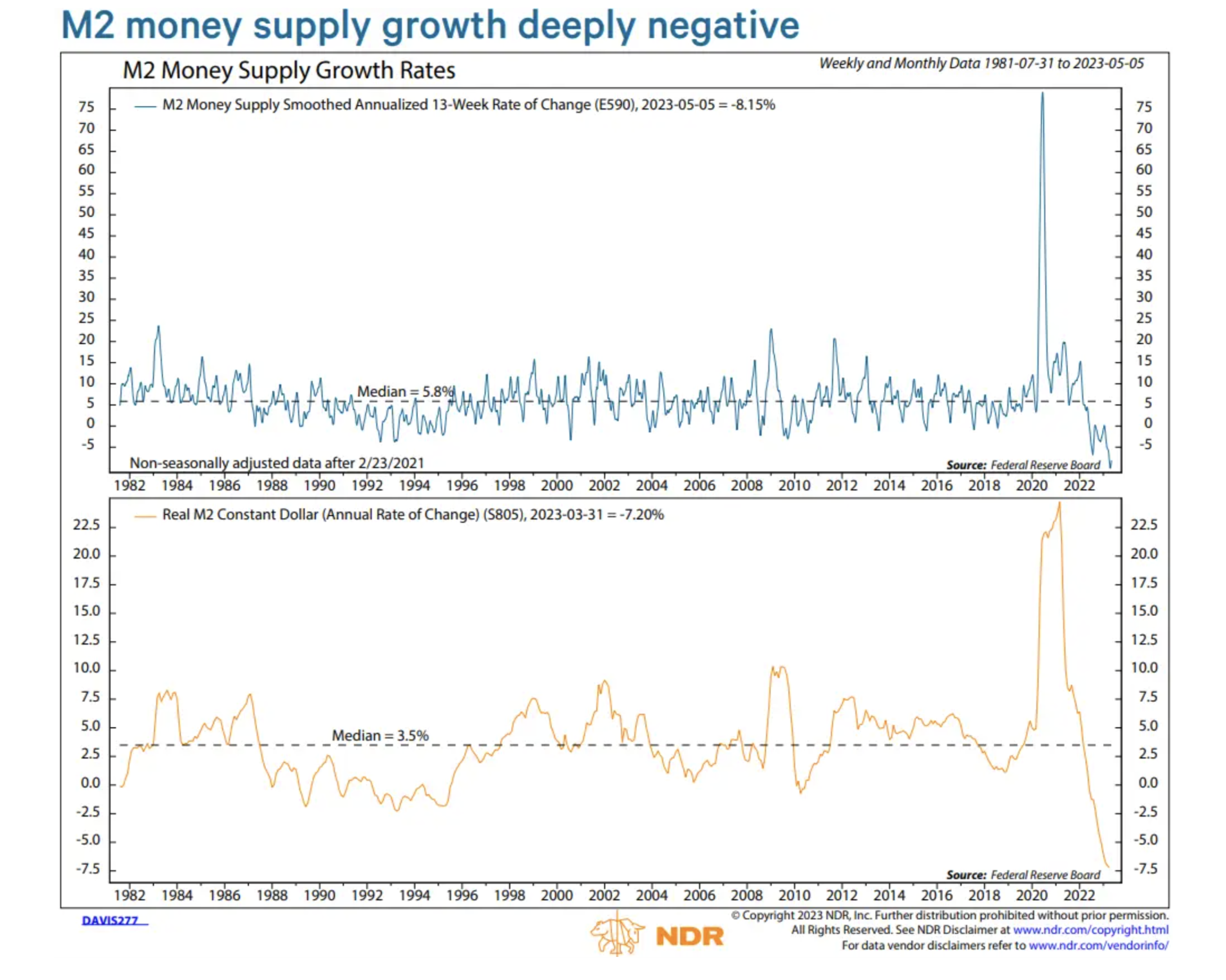

My third forecast was that Global liquidity will turn extremely negative next year.

Check again! The degree and speed at which this has happened is surprising.

I think this remains one of THE most important themes that investors should be focusing on. The implications for this are negative for both the economy and the stock market.

The Fed controls the yield on cash, but it also drives the availability of money.

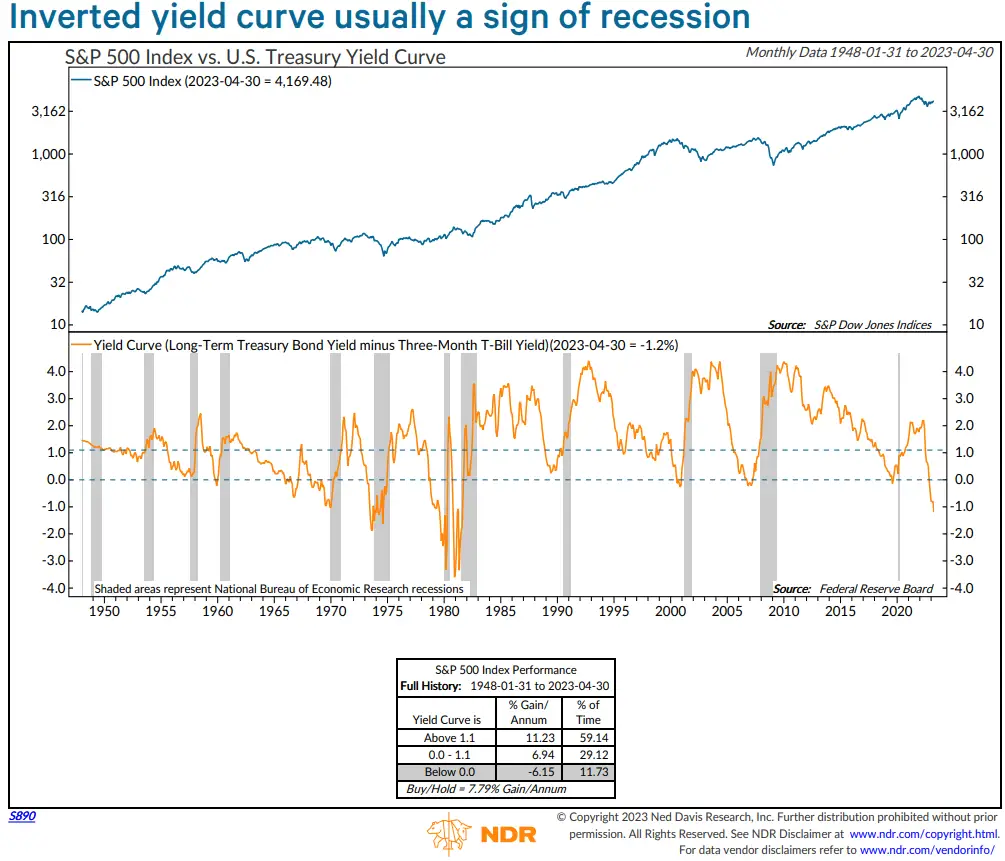

Finally, my fourth forecast was that Leading indicators point to a recession.

This remains as true today as it did six months ago.

Perhaps the most cited leading indicator for a recession is the inverted yield curve which continues to point toward a recession.

In Summary

Interest rates remain high and pose unintended consequences.

The last time that rates were this high, the banks began to break and nothing has changed. Additionally, CRE risks remain high and an area of additional risk to the banks.

After a reasonable bounce, financial stocks are showing signs of coming under pressure again.

Many money market funds are yielding above 5%. All Treasuries with maturities under a year are yielding above 5% also.

Can banks compete with that? Will banks be as willing to lend? Can we avoid a recession?

It’s hard to see how.

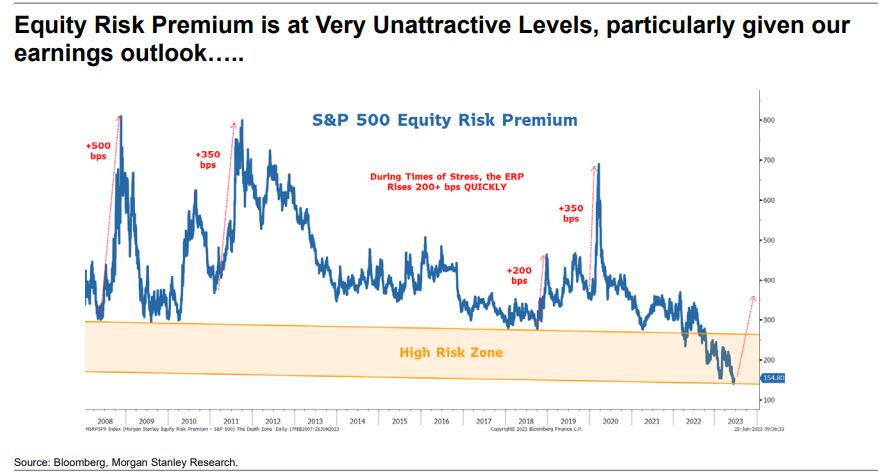

A final point is that bond yields make stocks less attractive.

Equity risk premium predicts how much a stock might outperform risk-free investments over the long term. Calculating the risk premium can be done by taking the estimated expected returns on stocks and subtracting them from the estimated expected return on risk-free bonds.

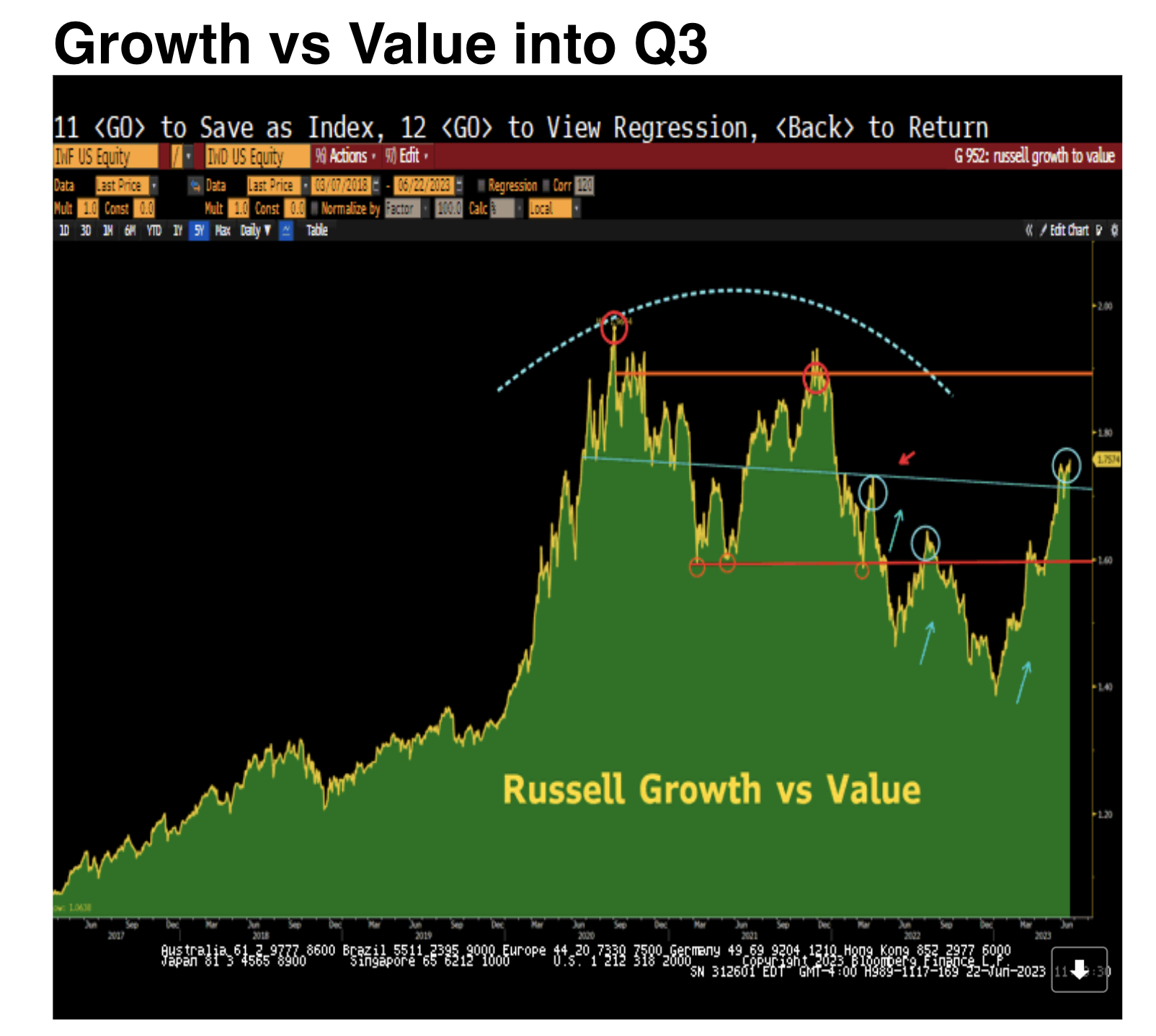

Finally, growth stocks are expensive and growth stocks have trounced value stocks in the first half of 2023. It would not be surprising to see a reversion to the mean in Q3.

Growth stocks have been priced for falling inflation and lower interest rates.

To the degree that inflation remains sustainable, the risk-free rate remains a threat to growth stocks and discounted cash flows, as sustained inflation hurts the value of future cash flows.

While historical data suggests that stocks may perform well in the second half of 2023, significant challenges remain.

In summary, the recent policy tightening is likely to have effects on investment, employment, and aggregate activity that are stronger than in most tightening episodes since the late 1970s.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.