Related Blogs

April 11, 2023 | Avalon Team

For decades, the U.S. Dollar (USD) has reigned supreme in global trade and capital flows.

However, this dominance is being challenged, as many countries seek alternatives to reduce their reliance on the United States.

Over the weekend, French President Emmanuel Macron joined the rhetoric as he stated that all of Europe should lower its dependence on the U.S. Dollar.

The comments follow Macron’s three-day trip to China and a high-profile meeting with Chinese President Xi Jinping.

It’s understandable why Russia would seek an alternative currency given how the U.S. seized $630B in Russian reserves because of the Russia/Ukraine war.

But France?

What’s going on and is this something that investors should be concerned with?

A Brief History

The U.S. Dollar’s ascent to the top of the financial hierarchy began after World War I when the country emerged as the leading financial power. As a result, the USD began to replace the pound sterling as the international reserve currency, and the U.S. became a significant recipient of wartime gold inflows.

The USD’s role was solidified in 1944 when 44 countries signed the Bretton Woods Agreement, which created a collective international currency exchange regime pegged to the USD, which was, in turn, pegged to the price of gold.

As European and Japanese exports became more competitive in the 1960s and due to the costs of funding the Korean and Vietnam wars, the U.S. began to run a trade deficit, making it difficult to continue to back the USD with gold.

President Nixon’s decision to cease the direct convertibility of USD to gold in 1971 ended both the gold standard and the limit on the amount of currency that could be printed.

In 1973, the petrodollar system was created through a deal between the U.S. and Saudi Arabia. The countries agreed to price and trade oil in U.S. Dollars.

With oil standardized in terms of USD, any country that purchased oil from Saudi Arabia would have to use dollars. This led many other oil-producing countries to standardize oil prices in USD – and the petrodollar system was born.

The petrodollar system gave the USD elevated status as the dominant currency in the global economy. This has many benefits for the U.S., including:

- Consistent trade deficits and source of liquidity.

- Inflow of foreign capital through petrodollar recycling.

- Ability to finance deficit with low-interest-rate assets.

- Decisive influence over global economic markets.

The same elevated status for the USD is also responsible for the downsides of petrocurrency. The petro system results in a catch-22 for the USD that could cause it to lose its status:

- The U.S. needs to run account deficits to maintain liquidity in a continuously expanding global economy.

- Stopping these deficits will slow down the global economy.

- Continuing the deficits may cause other countries to downgrade the value of the dollar.

Indeed, the USD’s purchasing power has steadily declined.

By 1981, after years of inflation, the U.S. Dollar had lost two-thirds of its purchasing power. And that trend has only worsened.

In response to the Global Financial Crisis in 2008-2009, the Federal Reserve began a program of Quantitative Easing (QE) that flooded the system with money.

Then, as a response to Covid, the Fed was again required to provide liquidity. In 2020 alone, nearly $4T was added to the money supply equal to 20% of the dollars created!

And it’s because of the flood of money in recent years, coupled with supply constraints, this has led to the current, sudden rise in inflation (too many dollars chasing too few goods).

With the U.S. continuing to run a deficit, the U.S. is required to continue to “print money.” This has led to a loss in purchase power for the USD, leading some nations to begin losing faith in the system.

In recent years, other nations, particularly Russia and China, have been taking steps to reduce their dependence on the USD. These efforts have included increased trade between Russia and China using their national currencies, as well as the development of a gold-backed cryptocurrency by Russia and Iran.

In fact, Russia, China, India, and Turkey have been buying gold hand over fist.

Gold can play an important role in the financial reserves of nations:

- Balancing foreign exchange reserves: Central banks have long held gold as part of their reserves to manage risk from currency holdings and to promote stability during economic turmoil.

- Hedging against fiat currencies: Gold offers a hedge against the eroding purchasing power of currencies (mainly the USD) due to inflation.

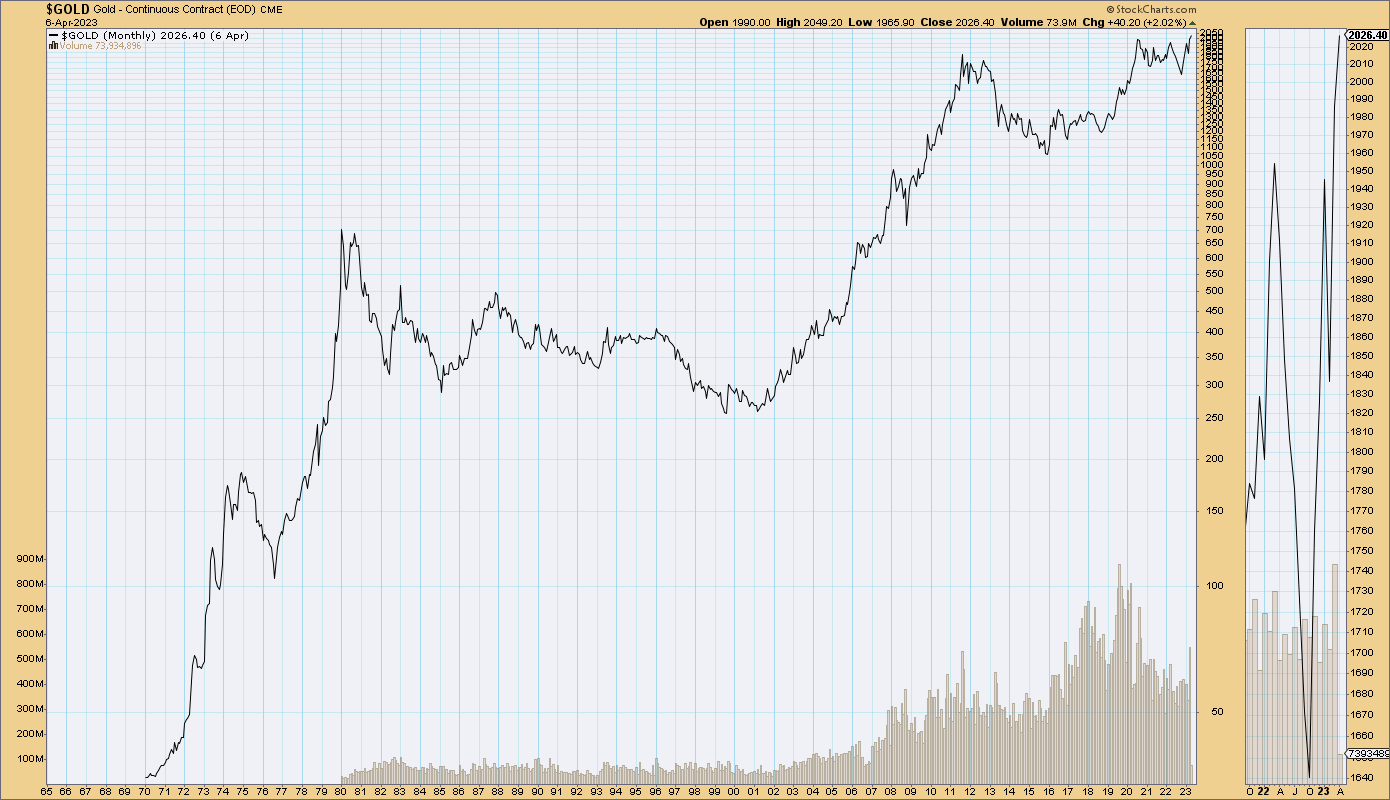

And right now, gold is one of THE most bullish charts on the planet.

Other countries are also exploring ways to reduce their reliance on the USD. For example, Brazil and Argentina have discussed creating a common currency, while Saudi Arabia has expressed openness to trading in currencies other than the USD.

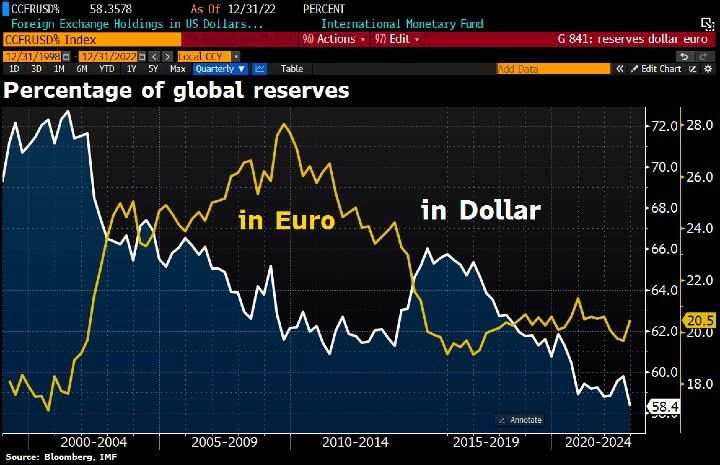

Despite these movements, the USD’s global sovereign status will unlikely end anytime soon. Central banks still hold approximately 60% of their foreign exchange reserves in USD.

While the dollar’s share of the central banks’ $12 trillion foreign exchange reserves has indeed declined since 1999, it is still nearly twice that of the Euro, Yen, Pound, and Yuan combined – the same as it was a decade ago.

Its nearest competitor for global currency status, the Euro, accounts for barely 20% of central bank reserves compared to the USD’s 58%, followed by the Japanese yen at 5%.

The trend away from the U.S. Dollar is an important one and one that investors need to follow.

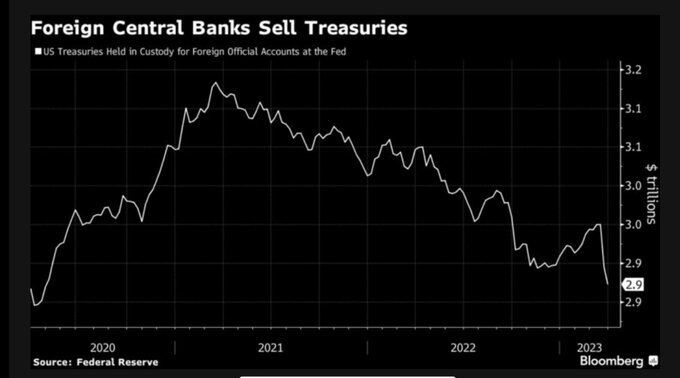

Concurrently, at a time when the U.S. is running record deficits and with the looming debt ceiling issues, foreign central banks are pulling back on their purchase of U.S. Treasures.

Russia has sold (almost) all. China still selling.

This could force the Fed to be a buyer again soon (its balance sheet already shows a $5.3 TRILLION treasury position).

This is actually far more serious as debt monetization means further dollar debasement and inflation.

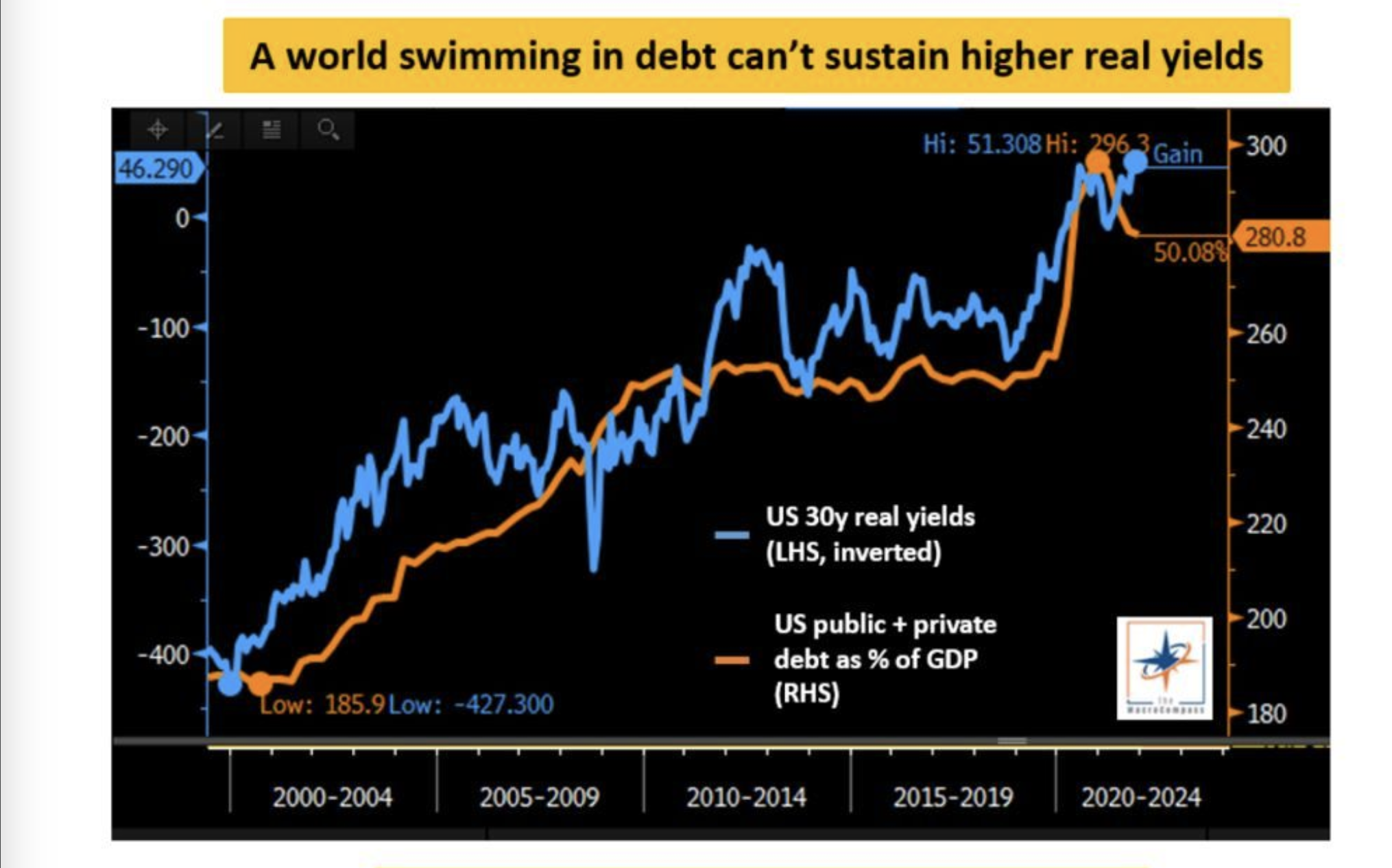

The next chart shows the tight relationship between economic debt levels (orange) and real interest rates (blue-inverted scale).

The higher the public and private sector debt levels, the lower the interest rates must be to sustain it.

Lower yields have incentivized more debt buildup as leverage was “affordable.”

Historically, no policymaker will willingly challenge the status quo. It has always been major geopolitical events that have led to changes in our monetary system.

Will this time be any different?

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.