Related Blogs

June 15, 2023 | Avalon Team

So far in our Rules-Based Investing series, we’ve discussed several advantages of using a systematic approach to investing.

Today I’m going to outline some of the exact rules used by some of the world’s top money managers.

In fact, some of the world’s best-performing hedge funds use systematic approaches.

The Medallion Fund, managed by Renaissance Technologies, is a highly successful and renowned hedge fund known for its impressive returns and enigmatic nature. Founded in 1988 by mathematician Jim Simons, the fund has gained a reputation for utilizing sophisticated mathematical models and algorithms to trade in financial markets.

The Medallion Fund’s exceptional performance has led to its recognition as one of the most successful investment portfolios ever. It has achieved significant growth, with $100 invested in the fund since its inception growing to an estimated $398.7 million by 2018, representing a compound return of 63.3%

While the inner workings of the Medallion Fund are secret, the good news is that many of the most successful techniques of systematic and quantitative investing are available for free.

One of the best locations to find such research is at the Social Science Research Network (SSRN) where thousands of papers are archived and available for download.

As many readers already know, relative strength and momentum are the favored approaches used by Avalon. Hedge funds have been producing astounding returns for decades using momentum/price-trend following techniques.

And fortunately, there are dozens of papers that discuss and support the success of using such approaches.

A quick SSRN search reveals some of the most popular papers.

As a matter of fact, the #2 most popular paper, “Absolute Momentum. A Simple Rules-Based Strategy and Universal Trend-Following Overlay” serves as the basis for Avalon’s popular Volatility-Resistance Model.

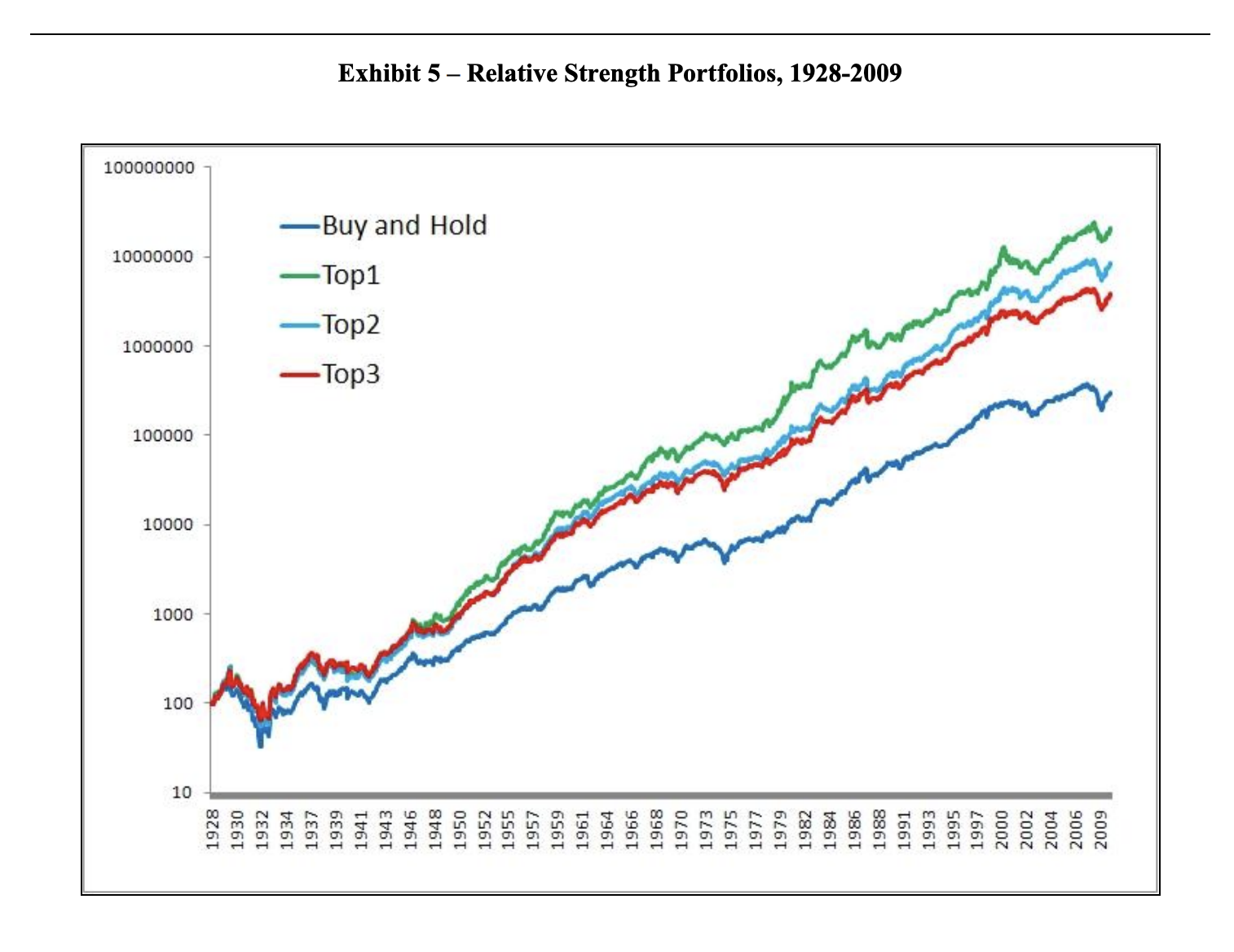

From one of the most downloaded papers, “Relative Strength Strategies for Investing”, author Mebane Faber shows that investing in the top sector (as ranked by relative strength) has consistently provided above-average performance for a very long time.

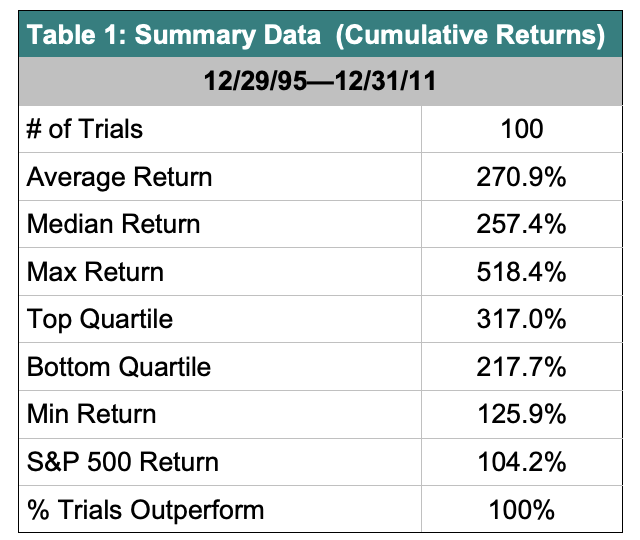

Another paper that can also be found in the SSRN library is “Relative Strength and Portfolio Management” by John Lewis which provides a brief history of relative strength research and then introduces a robust testing process.

In the tests, a portfolio was constructed by randomly selecting stocks from the top decile as ranked by relative strength. Stocks are sold only if they fall from the top quartile. 100% of the time, out of 100 sample portfolios, the relative strength portfolio outperforms the S&P 500.

It’s worth noting that even the bottom quartile of relative strength stocks outperformed the S&P 500 as well.

Systematic, rules-based investing strategies, while not mainstream, provide investors with the ability to capture more return, and if well constructed, minimize downside loss.

The basis for such strategies are grounded in academic research readily available to everyone.

Now that you’re intrigued by the immense potential of rules-based investing, it’s time to take the next step.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.