Related Blogs

October 31, 2023 | Avalon Team

It’s Halloween and based on the price of candy this year, it’s more of a trick than a treat.

If you’ve bought candy, then you know what I am talking about – the price of candy has gotten scary expensive.

Take a look at the chart below. As you can see the CPI for candy is ripping higher.

Behind this is the price of cocoa, which is approaching a 45-year high on signs of stronger global cocoa demand despite a sharp rise in prices.

What could be scarier than a $20 bag of candy at Walmart?

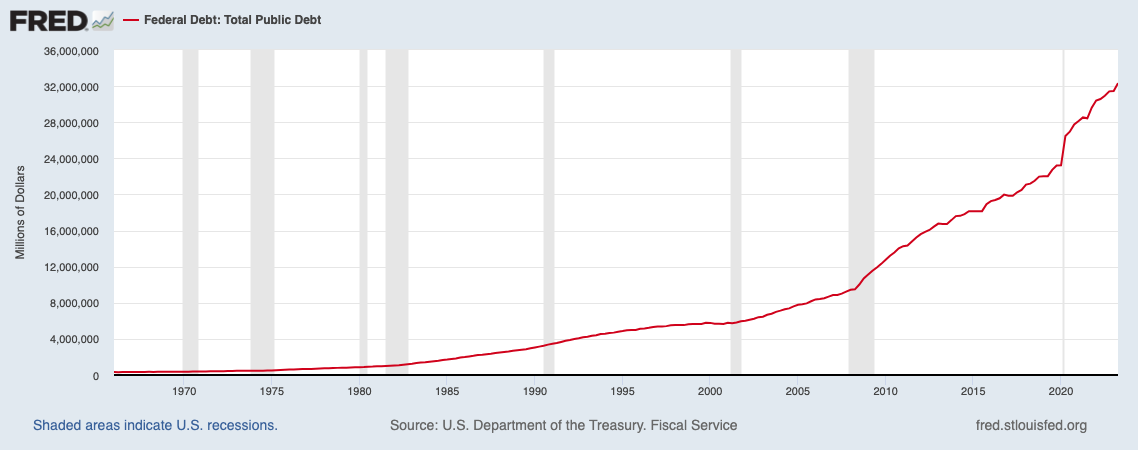

How about our out-of-control spending and U.S. deficit?

In a closely watched announcement Monday afternoon, the Treasury Department said it will look to borrow $776 billion for the final three months of the year and an additional $816 billion in the first quarter of 2024.

Yes, you read that correctly – nearly $1.6 trillion is to be added to the U.S. national debt.

And this is after the U.S. government borrowed $1.01 trillion between July and September… the highest amount ever during a single quarter!

In total, the U.S. has borrowed approximately $1.8 trillion YTD. Add in the new borrowings and it will put the 2023 total at around $2.5 trillion.

When the Treasury announced in July its heightened borrowing needs, it set off a frenzy in the bond market that saw yields hit their highest levels since 2007.

While over the past week, the yield on the Ten-Year U.S. Treasury note has backed off after reaching 5%, the big picture is what investors need to be focused on.

While many investors remain fixated on the short term and what the Fed’s next move will be, the big picture is that of a secular change in the long-term direction of rates.

As the following chart shows, rates are rising after breaking out of a multi-decade trend channel.

Is it a coincidence that this occurring as the Federal deficit is soaring?

I think not.

An announcement Wednesday on refunding, entailing the size of Treasury auctions and the duration mix of the debt that will be issued, is expected to draw more market interest than usual.

Auctions of government debt, normally routine events for the Treasury Department, have suddenly become very important to financial markets.

With debt, deficits, and bond yields all surging, investors are closely watching how the government will go to market with its borrowing needs as fears of oversupply are increasing when the Federal Reserve is keeping monetary policy tight.

As a result, investors are demanding a premium for interest rate risk, and geopolitics is posing various wild cards.

I fear it is no longer just the level of economic activity or the core inflation level that is driving rates.

While undoubtedly important, the continued massive borrowing causing the need for an excessive supply of bonds is now becoming an important factor, too.

Do High Interest Rates Fix High Inflation?

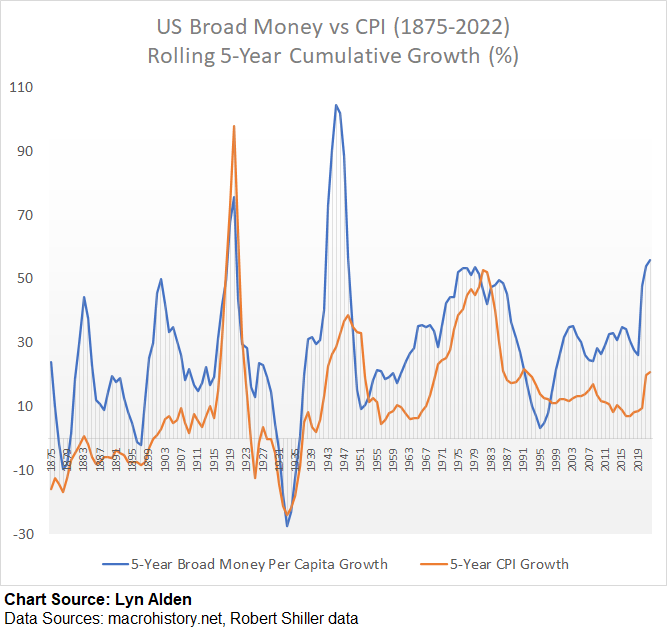

In short, the rate of consumer price inflation in an economy comes from a combination of 1) money supply growth and 2) significant changes in productivity and/or resource abundance.

Periods of fast bank lending or large monetized fiscal deficits (and thus rapid money supply growth) tend to create inflationary environments, while periods of fiscal austerity and/or private sector deleveraging events (and thus slow money supply growth or outright money supply contraction) tend to create disinflationary or outright deflationary environments.

Clearly, the reaction to Covid has been a case of the former as the Fed created a massive amount of money supply in response, leading to an increase in inflation.

With the Fed’s decision on interest rates looming on Wednesday, the question is do high interest rates fix high inflation?

The problem, of course, is that central banks can only affect a subset of the causes of inflation.

They can influence, albeit very imperfectly, how much private sector credit creation (bank lending) happens.

In the current financial system, the majority of broad money creation happens due to a combination of fiscal deficits and bank lending, and the magnitude of those two sources relative to each other changes over time.

In the 1940s and 2020s inflationary periods, most of the money supply growth was from fiscal deficits (related to the war and the pandemic stimulus respectively). In the 1970s, most of the money supply growth was from bank lending (related to demographics primarily).

This is an important distinction, and here is why.

Currently, Fed Chairman Jerome Powell is treating the 2020s (which is fiscal-driven inflation in a high public debt environment) as though it’s like the 1970s (which was lending-driven inflation in a low public debt environment).

He is sharply raising interest rates to try to quell bank lending, even though bank lending wasn’t the cause of inflation in this cycle.

As this chart shows, money supply growth precedes an increase in inflation.

This would suggest that high rates alone will not be sufficient to quell inflation. It also adds the complication that rising interest costs become an increasingly important factor as the debt level swells.

In summary, no matter the Fed’s decision on Wednesday, inflation is not going away anytime soon.

Better save some candy for next year.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.