Related Blogs

August 9, 2023 | Avalon Team

What if stock market investors have it all wrong?

Since the beginning of time (ok, maybe not that long), investors have been told that the expected return on stocks is 10% give or take a little.

It is a mantra that investors hear often.

It is also essential to the Capital Asset Pricing Model, a method widely used throughout finance for pricing risky securities.

But never are investors informed on how that expected return comes about.

In fact, during the past 30 years, the compound annual growth rate of the stock market has been 10.7%.

But recently, I came across a white paper, written by an economist for the Federal Reserve Board that says that investors should expect the experience of the past 30-plus years to be different than what’s coming the future. The same rules may not apply.

The paper is called “End of an Era: The Coming Long-Run Slowdown in Corporate Profit Growth and Stock Returns.”

One of the most common investor errors is that of “recency bias,” which is the tendency for investors to overemphasize the importance of recent experiences or the latest information we possess when estimating future events.

As an example, at the end of the 1970s, after a decade-long bear market and record-high inflation, investors wanted nothing to do with stocks when the market offered one of the greatest buying opportunities of the past century.

The recency of the pain and frustration was too much to overcome.

Today, after four decades of falling interest rates, rising stock prices, and falling inflation, some investors may have difficulty recognizing the epochal change that is taking place before their eyes.

The paper has raised important insights for investors, shedding light on potential changes in the landscape of corporate profits and stock market returns.

This analysis has significant implications for investors who are keen on understanding how the interplay between interest rates, tax rates, and market dynamics might affect their investment strategies.

The paper highlights the remarkable growth in corporate earnings over the past three decades, outpacing previous growth patterns despite economic fluctuations.

The author asks this question:

“From 1989 to 2019, the S&P 500 index grew at an impressive real rate of 5.5 percent per year, excluding dividends. The rate of U.S. real GDP growth over the same period was 2.5 percent. What accounts for this enormous discrepancy? And is it sustainable?”

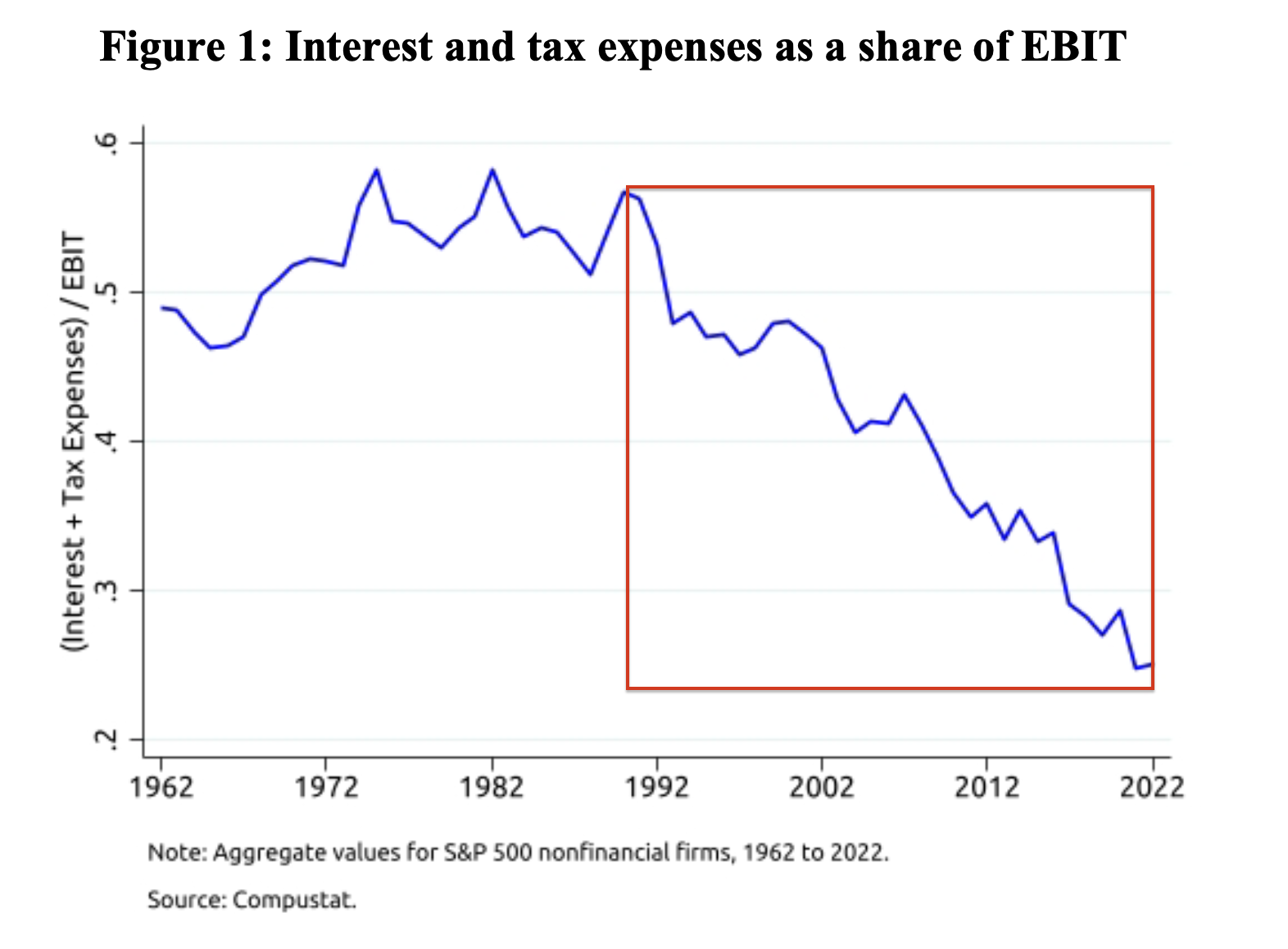

The author’s central finding is that in the 30 years prior to the pandemic, exceptional growth was notably influenced by two key factors: declining interest rate expenses and lower corporate tax rates.

The lower interest rates have acted as a favorable tailwind for corporate profits, as well as the reduction in corporate tax rates.

In fact, the paper suggests that over 40% of the profit growth of S&P 500 non-financial firms can be attributed to these factors.

Between 1989 and 2019, the amount of corporate earnings paid out to debt holders and tax authorities declined from 54% to 27%. This left an ever-increasing share available to stockholders.

Additionally, the author found that the decline in risk-free rates over this period explains the entirety of the expansion of price-to-earings (P/E) multiples.

Collectively, these factors account for the majority of this period’s exceptional stock market performance.

These favorable conditions that have driven profit growth are now changing, marking a potential shift in the investment landscape.

There’s an expectation of significantly lower profit growth and stock returns in the coming years due to the diminishing impact of declining interest rates and lower tax rates.

This implies that the previous era of robust profit growth and stock market performance may come to an end.

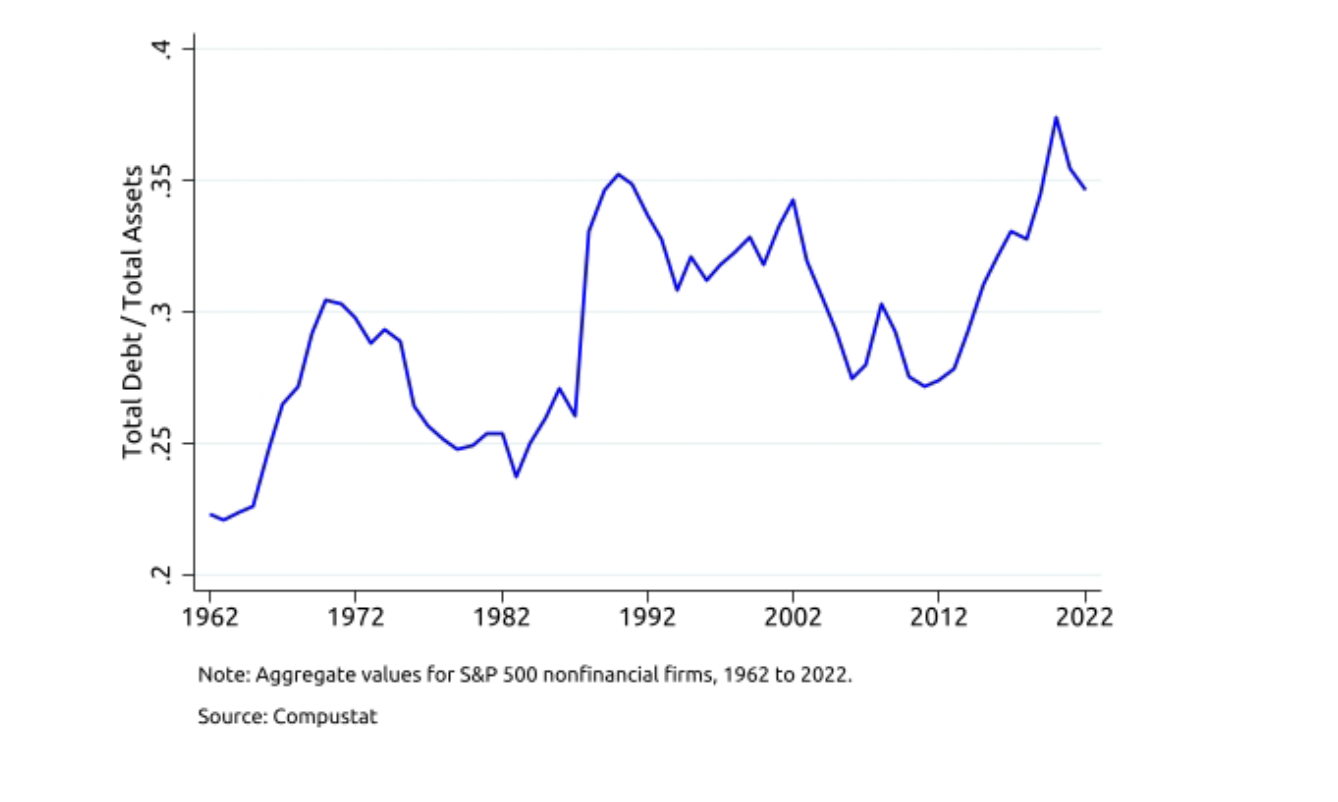

Additionally, corporate leverage has increased in the last decade as corporations borrowed more money to take advantage of lower interest rates.

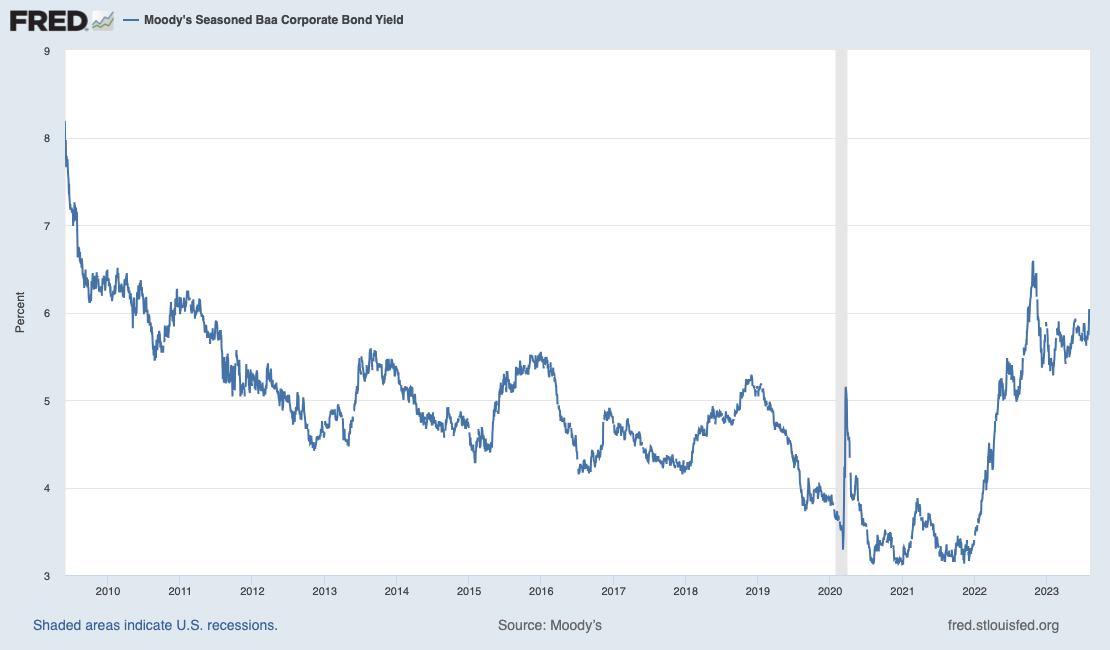

But now, companies will need to either pay down this debt or face refinancing at significantly higher rates.

As this graph clearly shows, corporate bond borrowing costs are on the rise.

The paper raises a pertinent question:

How will the changing economic environment impact investment strategies moving forward?

With the diminishing tailwinds of declining interest rates and corporate tax rates, investors need to reevaluate their assumptions about profit growth and stock market returns.

They might consider diversifying their portfolios and exploring alternative investment approaches that can help navigate potential challenges in the investment landscape.

In conclusion, the “End of an Era” paper is a valuable resource for investors seeking to understand the evolving dynamics of corporate profits and stock market returns.

It highlights the substantial impact that declining interest rates and lower corporate tax rates have had on profit growth and stock performance.

As these factors change, investors should reassess their investment strategies and consider new approaches to adapt to the evolving investment landscape.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.