Related Blogs

March 15, 2023 | Avalon Team

Two bank failures and a falling stock market. What is going on?

The events of the past week have caught many investors off guard, but for our regular readers and clients, you know that we have been warning about the growing risks in the markets for some time.

On March 1, I discussed how there were a diminishing number of attractive asset classes and how many of our primary “risk gauges” were flashing warnings.

As early as February 7, I showed how the percentage of stocks above their 50-day moving average was slipping and forming a negative divergence with the price of the S&P 500 Index.

And, back on December 29, I cited that one of my top concerns for 2023 was that “global liquidity would turn extremely negative.”

In today’s article, I will try to put some perspective on recent events and how this is all part of a bigger, systemic problem.

The first question that you may be wondering is “Is it 2008 all over again?”

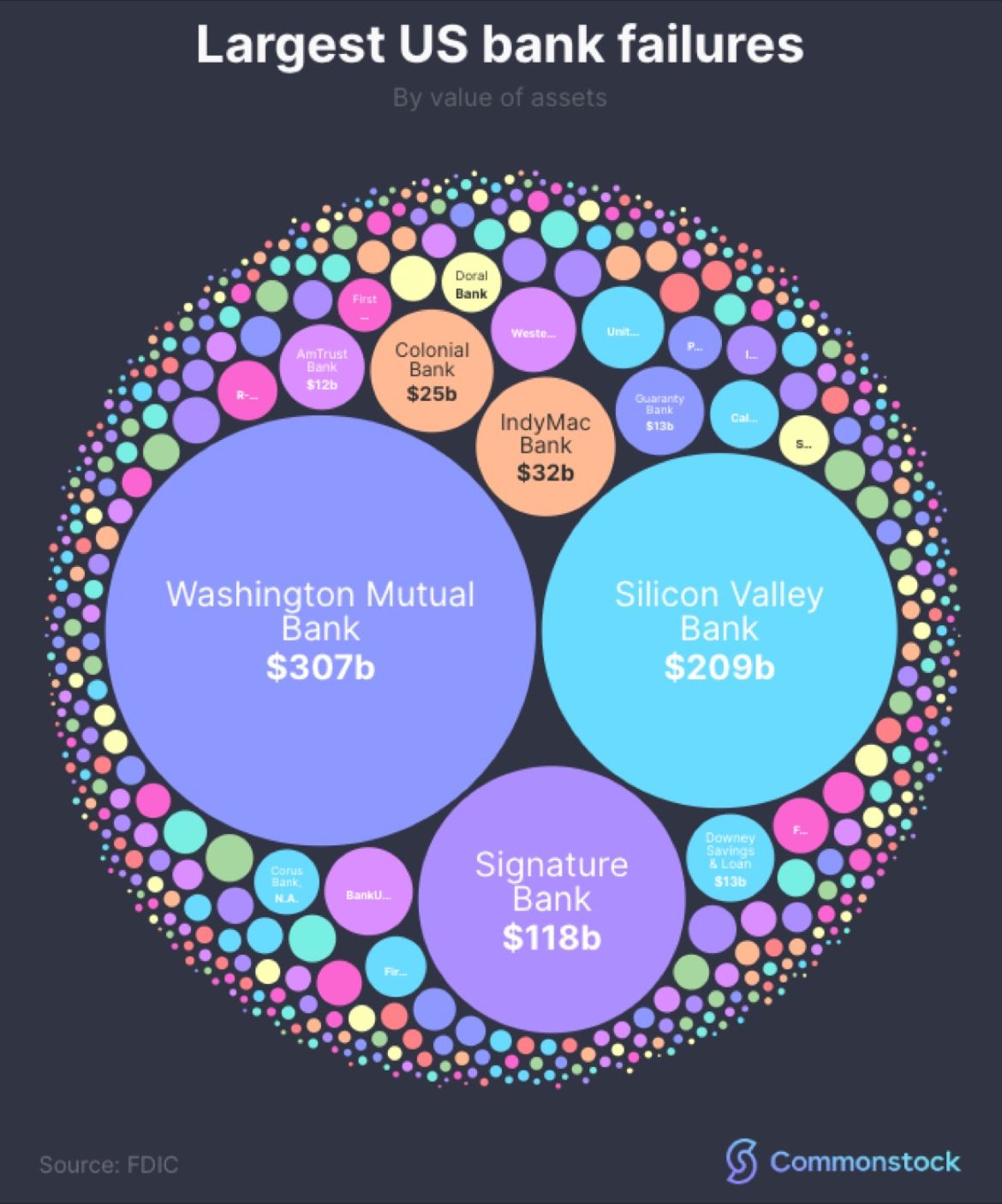

In 2008, the banking crisis was caused by subprime lending and toxic derivatives tied to the housing market. This led to the eventual collapse of Washington Mutual, which has been the largest bank failure in American history.

For the record, there have been 563 bank failures in the U.S. since 2001. The recent failures of Silicon Valley Bank (SVB) and Signature Bank would rank as the second and third largest, respectively.

The irony of the current failures is that the problems are arising from bank holdings of US Treasuries. Yes…the most senior security of all securities is where the problem lies.

Let me explain.

The Federal Reserve’s “too easy for far too long” monetary experiment has put everyone between the proverbial rock and a hard place.

The Fed is fighting a battle it cannot win.

By keeping rates too low, the Fed allowed the inflation genie to get out of the bottle. And there is no putting the genie back in the bottle without causing consequences that may be even worse than the problem they’re trying to fix.

If the Fed keeps rates too low, then inflation will continue to run rampant.

Tighten as they have, and well… things begin to break, as we’re seeing with SVB.

But inflation is far from tamed, so this is problematic.

Currently, the Fed Funds rate is under the inflation rate.

This would imply that the Fed, if they are serious about taming inflation, should continue to increase interest rates.

But high rates are unsustainable because government debt would spiral out of control due to the associated costs.

To maintain some credibility, the Fed has raised rates at an unprecedented speed. After all, they don’t want the mistake of repeating the 1970s.

And this is how the current crisis was born.

Now, before we conclude that this is an SVB problem because it was mismanaged (and it was!), here are a couple of troubling graphics.

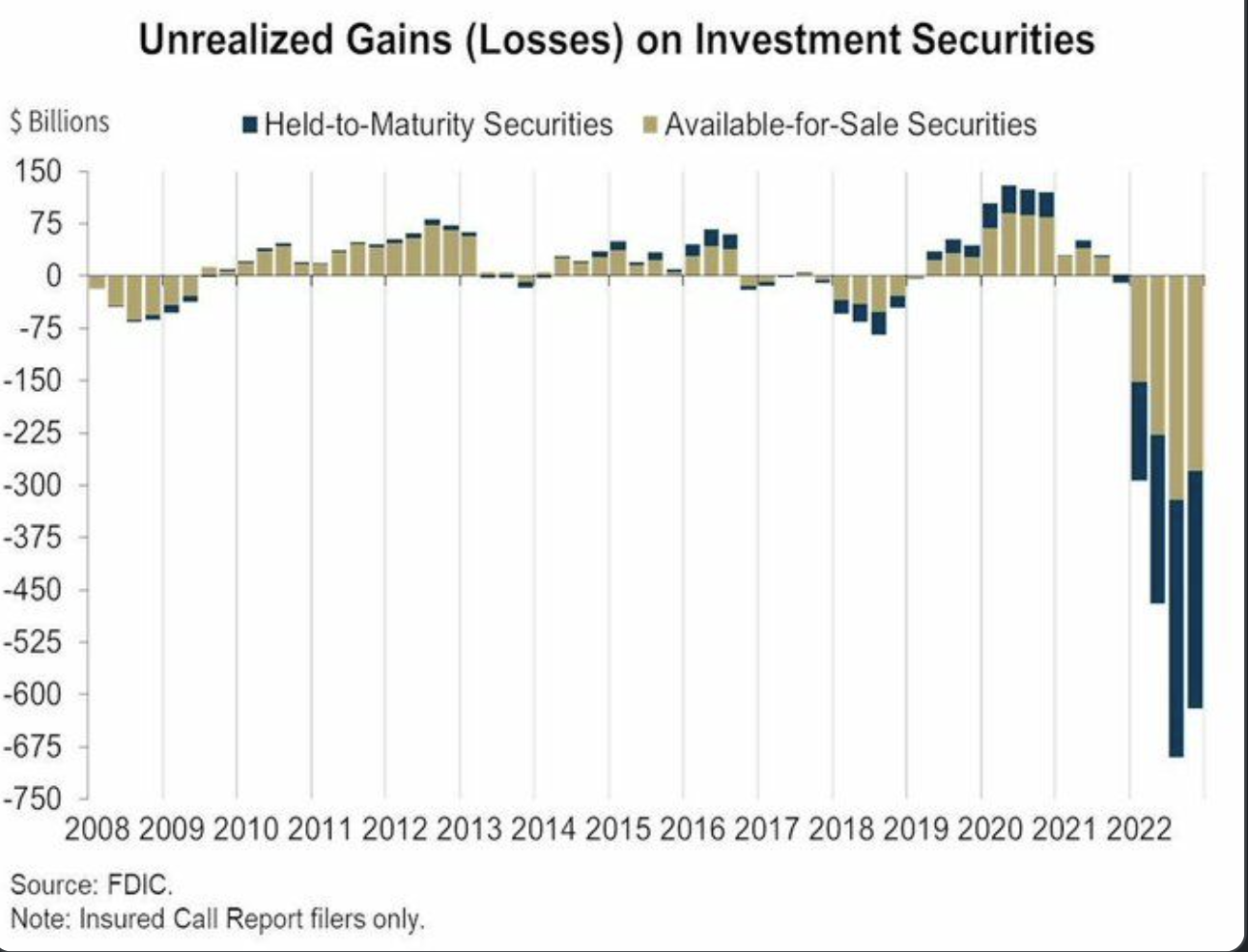

The top 4 banks currently are sitting with $210B in losses.

It is estimated that all banks are sitting with $640B in losses on longer-duration bond and debt portfolios.

When interest rates go up, bond prices go down. And it’s happening at banks everywhere.

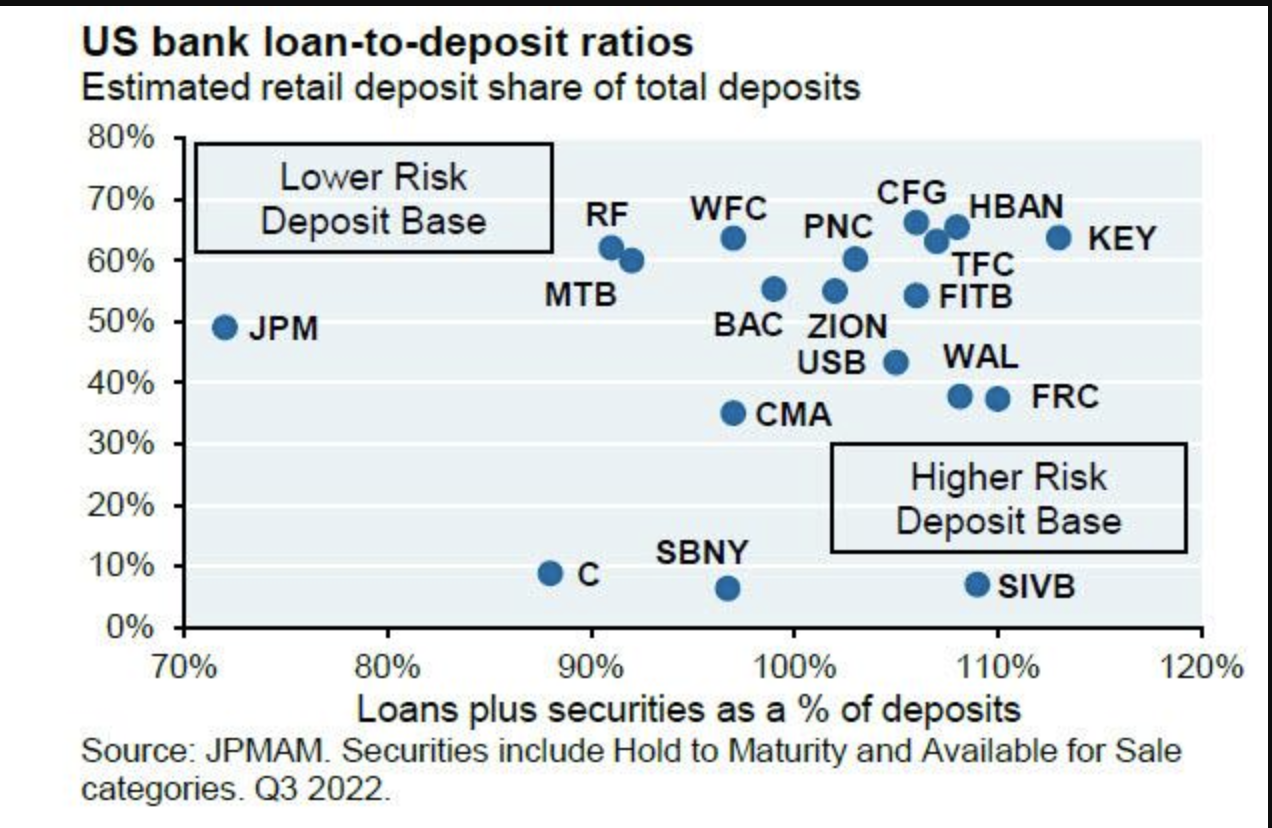

Not all banks were as leveraged and as un-hedged as SVB was, but the risk is not isolated to SVB as this next graphic shows.

Silicon Valley Bank Explained

Because banks don’t keep unlimited cash on hand, any bank can become the victim of a run on deposits. The crux is whether it’s an issue of liquidity or solvency.

If it’s merely a lack of liquidity (a healthy balance sheet, but simply not enough cash to meet withdrawals), then the Feds will step in and assist the bank, which, after all, is financially healthy.

A more serious problem arises when the lack of liquidity derives from inadequate solvency (losses on loans or investments embedded in the balance sheet).

SVB’s solvency issues don’t appear to be the result of billions in bad loans, but rather the U.S. government bonds they bought with the customers’ funds.

U.S. sovereign debt is generally considered highly liquid and very low risk.

Because the Fed forced interest rates to extremely low levels, banks that wanted to buy super-safe U.S. sovereign debt were essentially forced for years to buy bonds that offered extremely low yields.

When interest rates rise, as they recently have, the prices of the “safe” bonds the banks purchase drop (interest rates/yields and prices move in opposite directions).

This is typically not a problem because everyone still assumes that the bonds are low risk. If they’ve dropped in price, the bank just holds them until they mature and they get paid 100 cents on the dollar.

But what happens if large numbers of depositors suddenly demand their money back?

The safe, liquid U.S. government bonds they own can be sold, but (and here’s the key) because rising interest rates have forced the prices of those bonds down, selling today means they’re forced to lock in large losses on bonds that they would have in fact broken even on if they’d been able to hold them until maturity.

The run on SVB forced the bank to sell $21B in treasury bonds, incurring a $2B loss!

Now, many financial institutions will hedge their exposure using what are known as swaps, securities that will offset the losses of the bond exposure.

But SVB’s portfolio was unhedged.

The resulting loss put over $131B of depositor money at risk as over 97% of the accounts held at SVB had more than the FDIC guaranteed level of $250k.

As a result, over the weekend, the Fed announced a “Bank Term Funding Program” that will restore the accounts of the depositors.

Now, while it may be easy to conclude that the bank’s balance sheet was mismanaged, it is important to realize that accounting rules are such that hedging the interest rate risk on held-to-maturity (HTM) bonds is quite punitive.

As a result, U.S. banks end up not hedging their exposure to HTM bonds.

Please let that sink in.

The chances are very high that there are other banks that may be in a similar situation, but just have not been stressed with a run on deposits.

I will conclude with two more charts.

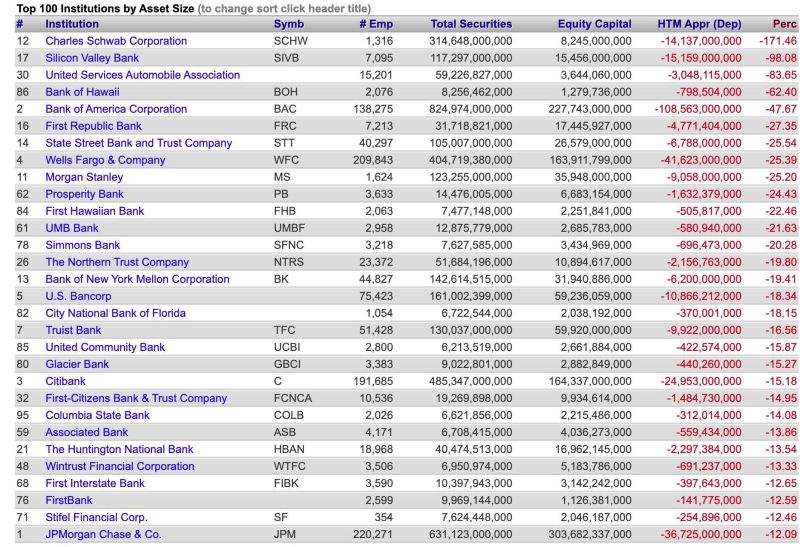

The first is of showing unrealized depreciation on Hold to Maturity Securities (HTM) for the top 100 banks versus equity. These unrealized losses are NOT reflected in profits or a deduction to equity via Other Comprehensive Income (OCI) – only in the footnotes!

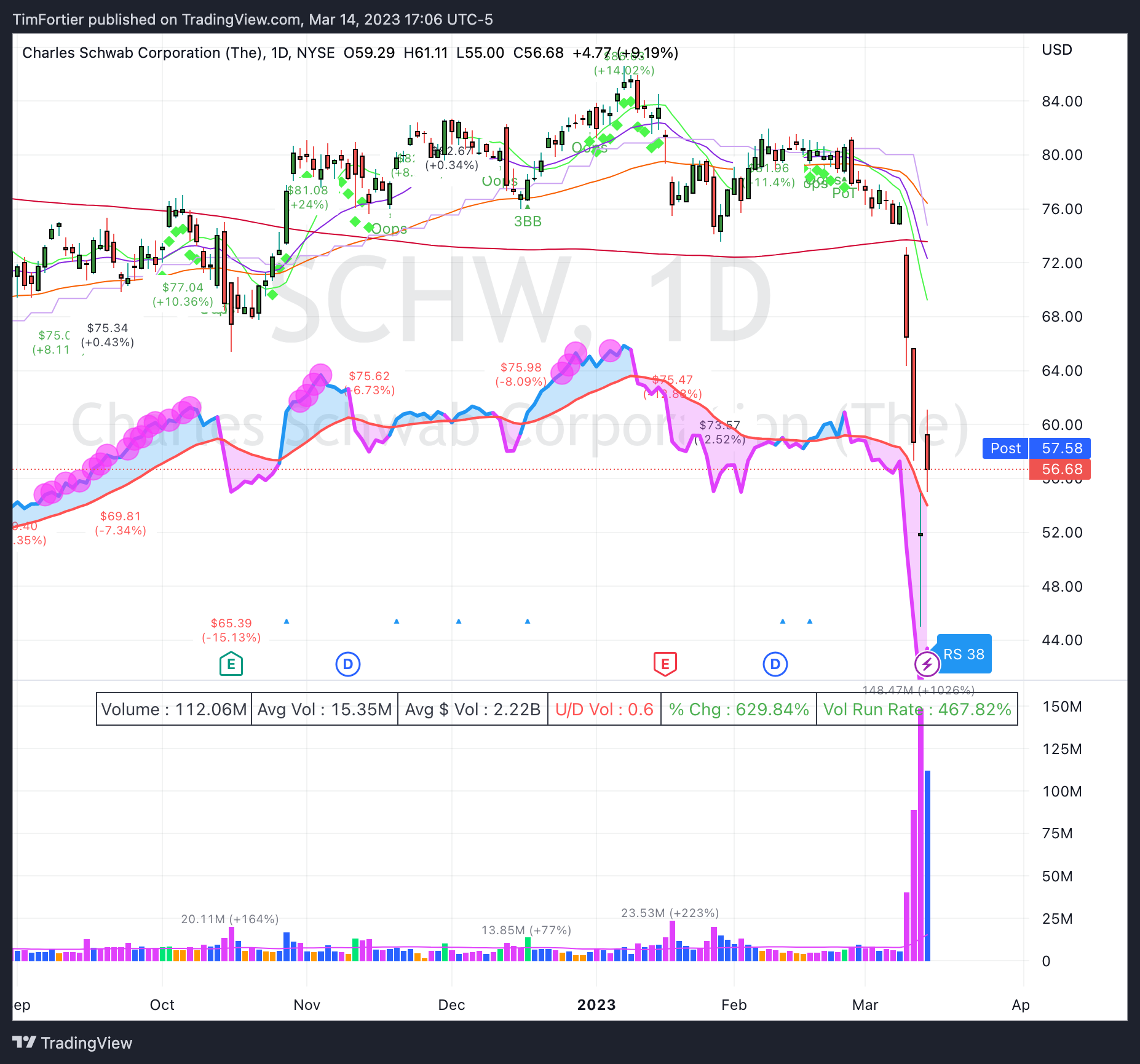

Note that Charles Schwab (SCH) has the distinguished honor of making the top of this list. And here is how the stock has traded.

Now if treasury bond holdings aren’t enough to be concerned with, Commercial Real Estate may be the next shoe to drop. Here is the list of regional banks with the WORST balance sheet exposure to Commercial Real Estate.

So, we may have just reached the “breaking point” where events begin to unravel as the embedded systemic risk looks to be more than an isolated event.

As I constantly talk about, effective portfolio management must begin and end with risk management.

The current dynamics will probably reveal a period of financial upheaval and uneven returns that will stress all but adaptive portfolios that are able to adjust to the new regime of embedded inflation and reactionary policy.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.