Related Blogs

December 21, 2022 | Avalon Team

Investors woke up to a major macro surprise Tuesday morning when the Bank of Japan announced a de-facto rate hike by allowing the yield on their 10-Year Treasury to reach .50%.

Although the Bank of Japan (BOJ) didn’t actually raise rates, the net result is the same.

What the BOJ did was allow the 10-Year Japanese Government Bond (JGB) trading band to widen by 25 bps (from 25 to 50 bps).

For decades, the BOJ has employed a monetary policy of low rates to encourage economic growth. They did so by capping the yield on JGBs at 25 bps (.25%).

So yesterday’s news is a major policy shift for Japan.

And it’s a really big deal at a macro level.

As far back as the 1990s, Japanese investors have had to look beyond their own borders for higher-yielding investments as an alternative to low-yielding JGB.

They often turned to U.S. Treasuries as a safe haven that offered higher net yields. As of July 2022, Japanese investors were the largest holders of U.S. Treasuries in the world, accumulating over $1 trillion.

Up until now, it made sense for Japanese investors to convert yen to dollars and invest in higher-yielding U.S. Treasuries. However, yesterday’s policy shift by the BOJ is a game changer.

With the increase in yields at home, Japanese investors can now expect to be better rewarded by investing at home vs. looking to foreign markets.

The potential Intermarket implications are enormous.

The most obvious is the potential shift in demand away from U.S. Treasuries. If there’s less demand for Treasuries then bond prices fall… and when bond prices fall, yields rise.

Beyond that, I’m considering the impact from a currency perspective. Japan’s policy shift means a stronger Yen and a weaker U.S. Dollar (USD).

The USD is already well off its October peak, losing strength vs. other world currencies, so Japan’s policy change may just fuel a further exodus out of the USD.

In just the last three months, the British pound is up over 6.5% and the Euro has gained almost 6% vs. the USD, while the Yen has gained nearly 8%.

And while I’ve beat the drum all year that a falling dollar is historically a tailwind for stocks, there’s another beneficiary of a falling USD.

Precious metals… specifically that shiny metal – Gold!

Gold is another store of value and is often considered an alternative currency.

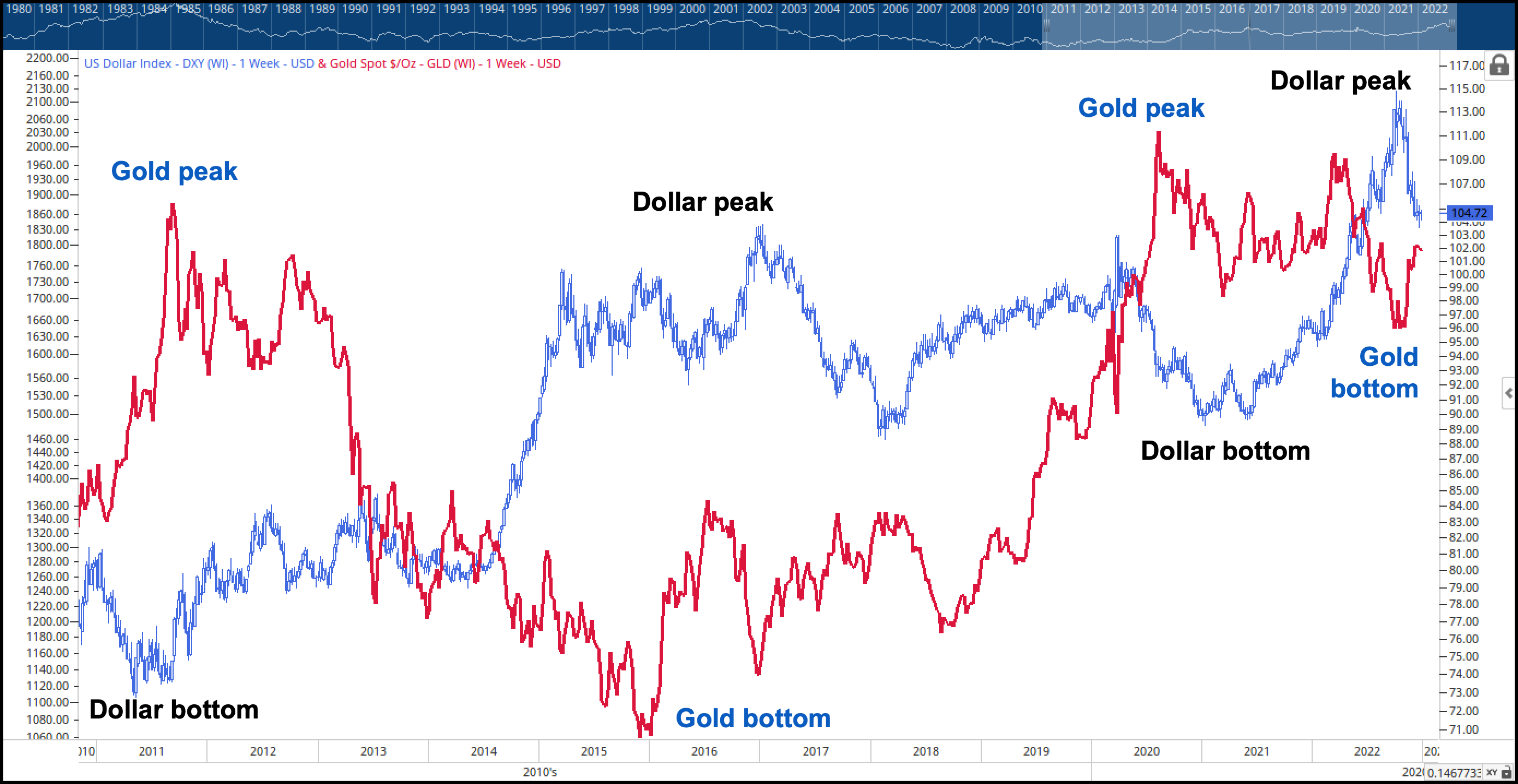

We can see the Intermarket relationship between the U.S Dollar and Gold here (HINT: It’s an inverse relationship).

The Formula is simple: Dollar rises = Gold falls. Dollar falls = Gold rises.

And in case you don’t track the USD as closely as we do, it peaked in October 2022.

As of this writing, USD sits at 103.97. What may be most interesting about that is it’s the same area that acted as resistance in 1999, 2016, and again in 2020.

Perhaps the most important question we should be asking is: Will prior resistance become new support (referred to as Polarity) or will the Dollar continue its descent?

If the USD can rebound, then Gold may have run its course. However, if the USD breaks down from here, Gold looks very interesting.

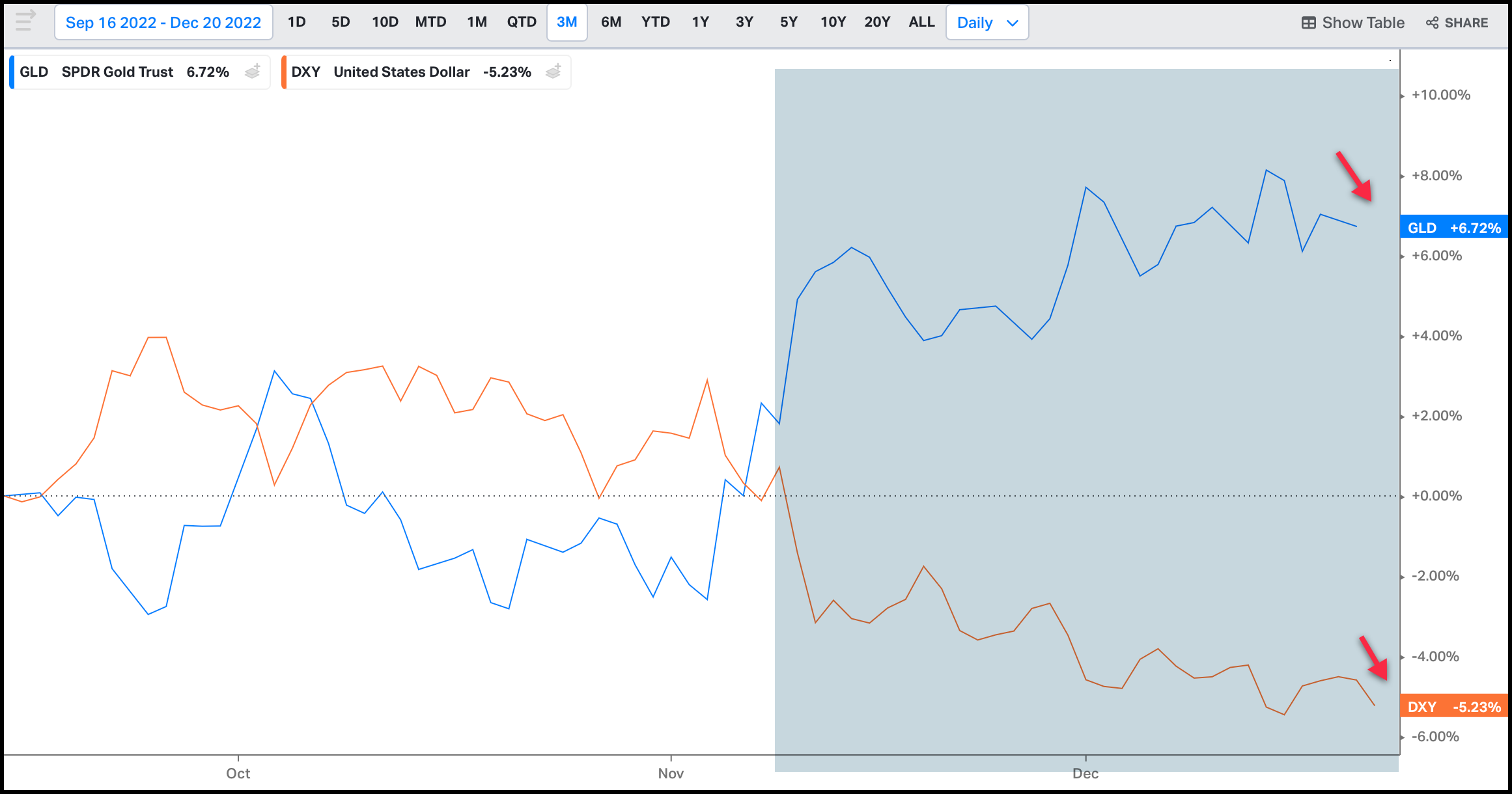

During the three-month slide in the USD (using DXY as our proxy) there is a nearly 12% performance differential with the advantage to Gold.

Gold is up +6.72%, while the Dollar is down -5.23%.

Hard to argue the reversal in the greenback since October has put a new charge in Gold.

Take a look at the performance of some of these Gold and Gold miner ETFs during the USD’s (DXY) recent slide.

DXY is down 5.23%, while the SPDR Gold ETF (GLD) has gained 6.72%, the VanEck Gold miners ETF (GDX) has jumped over 15% (15.25%) and Junior Gold Miners ETF (SGDJ) has gained 12.61%.

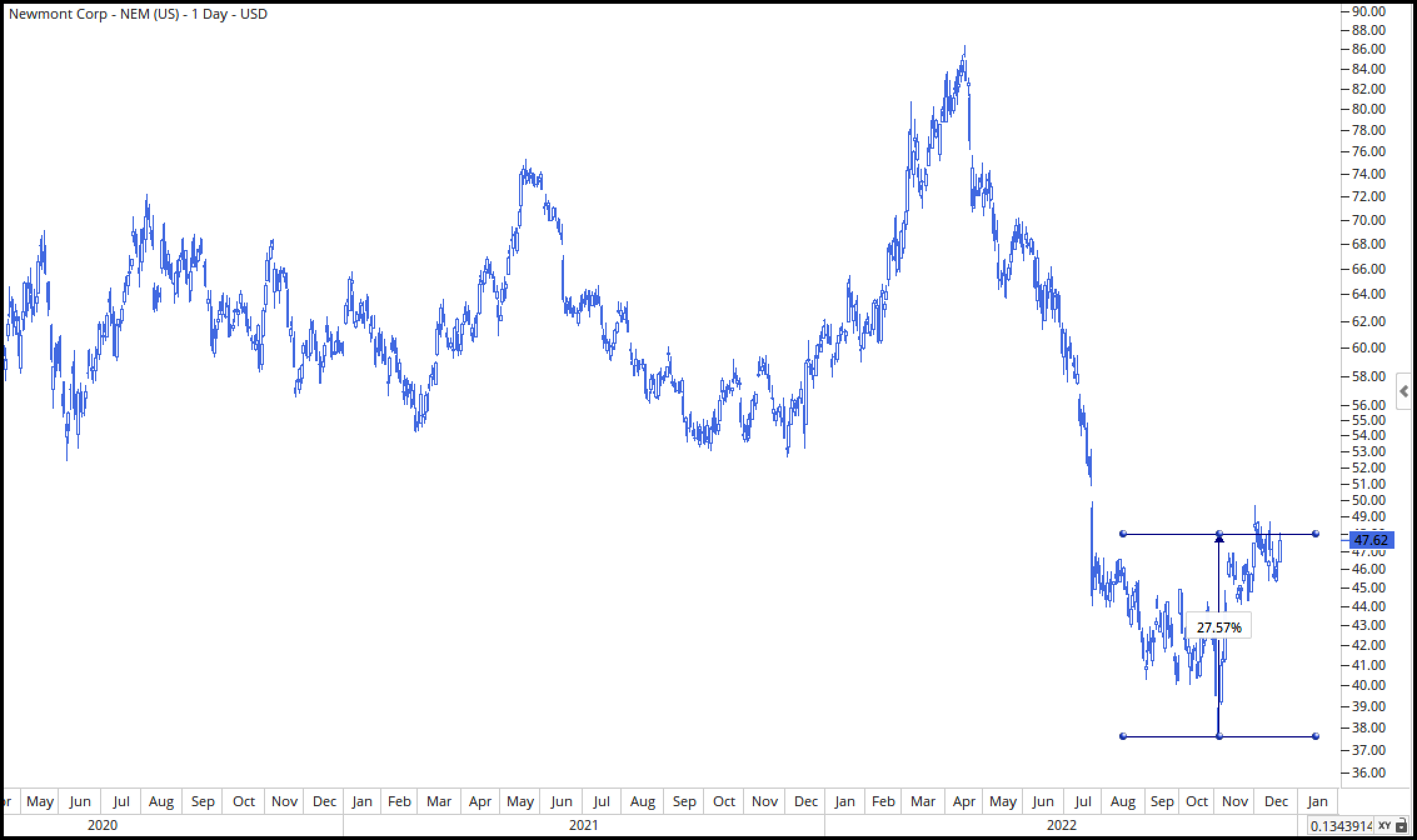

And here’s Newmont Mining (NEM) up over 27% off its recent lows.

I’m not making a buy recommendation on Newmont, I’m illustrating NUM’s recent gains to further emphasize the Intermarket relationship between the USD and Gold-related stocks and commodities.

Just to sum things up – here’s what investors want to remember…

The shift in Japanese monetary policy will have major impacts on both Government Bonds (price and yield) and the currencies markets.

If the USD feels further downward pressure as the result of Japan’s new monetary policy, its descent will create opportunities in precious metals – Gold being a major beneficiary.

So there you have it: Continue to do your homework and invest accordingly (and wisely).

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.