Related Blogs

January 17, 2024 | Avalon Team

The markets spent most of the 4th quarter of 2023 rallying on the idea that the disinflationary trend would continue making progress and the Fed would finally be able to loosen monetary policy again.

Cyclicals and small-caps rallied, which would be the logical response to an economic recovery trade, but 2024 has seen a complete about-face.

For better or worse, big tech has become a safe haven in this market, but it would almost certainly be a bad sign if 2024’s early leaders, consumer staples and healthcare, start making an extended run here.

A factor to consider is that some of the recent economic data points we’ve gotten haven’t just been bad…

They’ve been historically bad.

Most investors are focusing solely on GDP running at +3% and unemployment at less than 4%.

The first big warning was the ISM services employment report, which hit its 3rd lowest reading in the past 25 years, showing that the labor market in the most important segment of the U.S. economy is cracking.

This week, the U.S. Empire State manufacturing index hit its 2nd lowest level in the past 25 years behind only the COVID recession. We’ve known that the manufacturing sector has been in bad shape, but it might actually be in really bad shape.

If services employment is indicative of activity in the sector broadly, we could be entering a period of sharp slowdown right at the time when investor sentiment and positioning are at peak bullishness.

In today’s issue, we’ll take a look at some sector analysis to determine if any new trends may be emerging.

On a YTD basis, we can see that Healthcare, Communication, and Consumer Staples are positive with all other sectors negative.

Energy continues to struggle, with negative performance across all time frames as crude oil prices continue to slump.

To discern if new trends are emerging, I’m using ratio charts that compare the performance of a sector versus the general market.

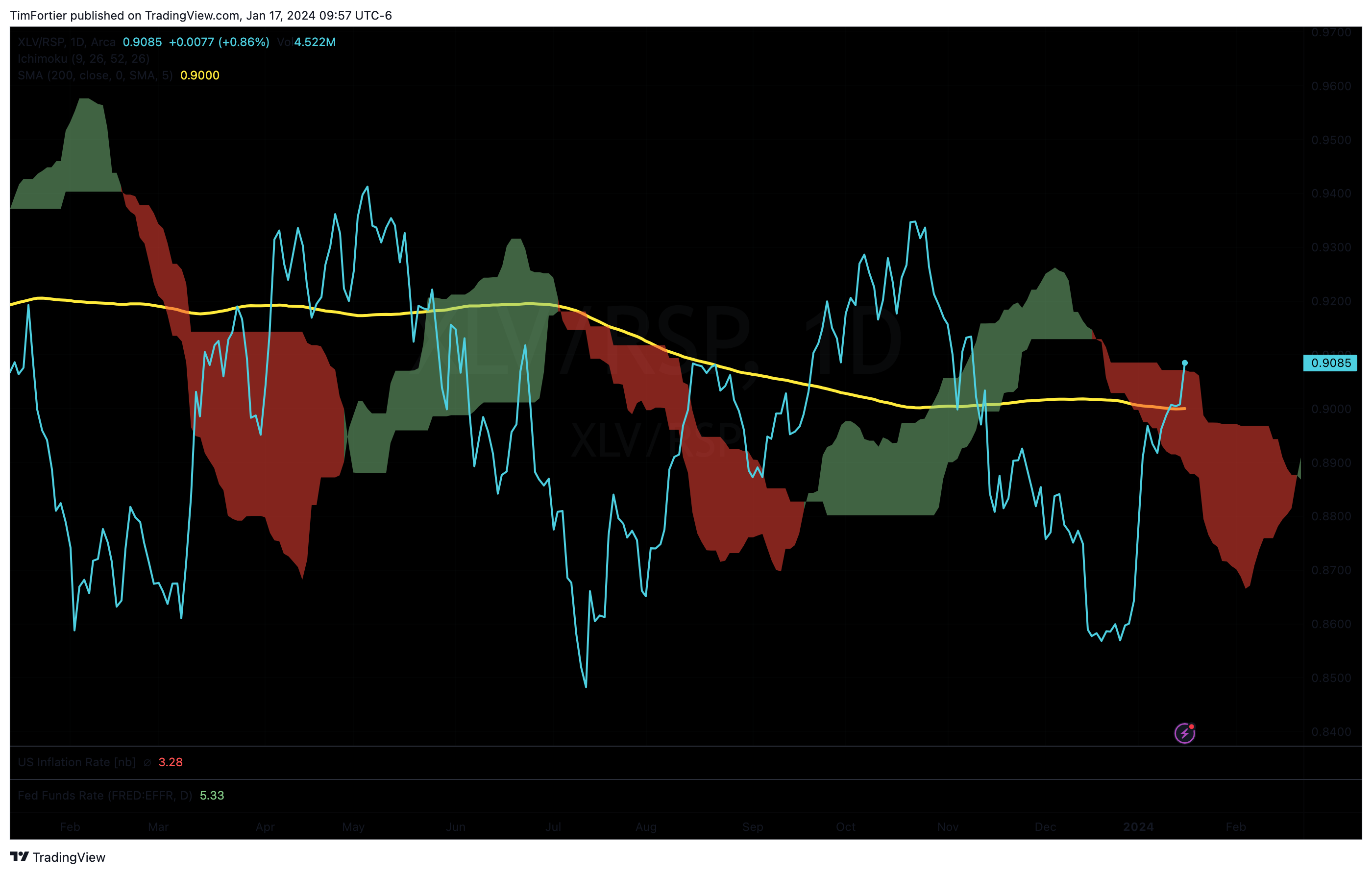

Healthcare

In the chart below we can see that the XLV Healthcare Select Sector SPDR has moved above both its moving average and the cloud. With the best YTD performance, this trend looks likely to continue.

Communication

The XLC Communication SPDR, a big winner from last year, is beginning to show signs of an exhausted trend. While still above its long-term moving average, the ratio has made a lower low and is now below the cloud.

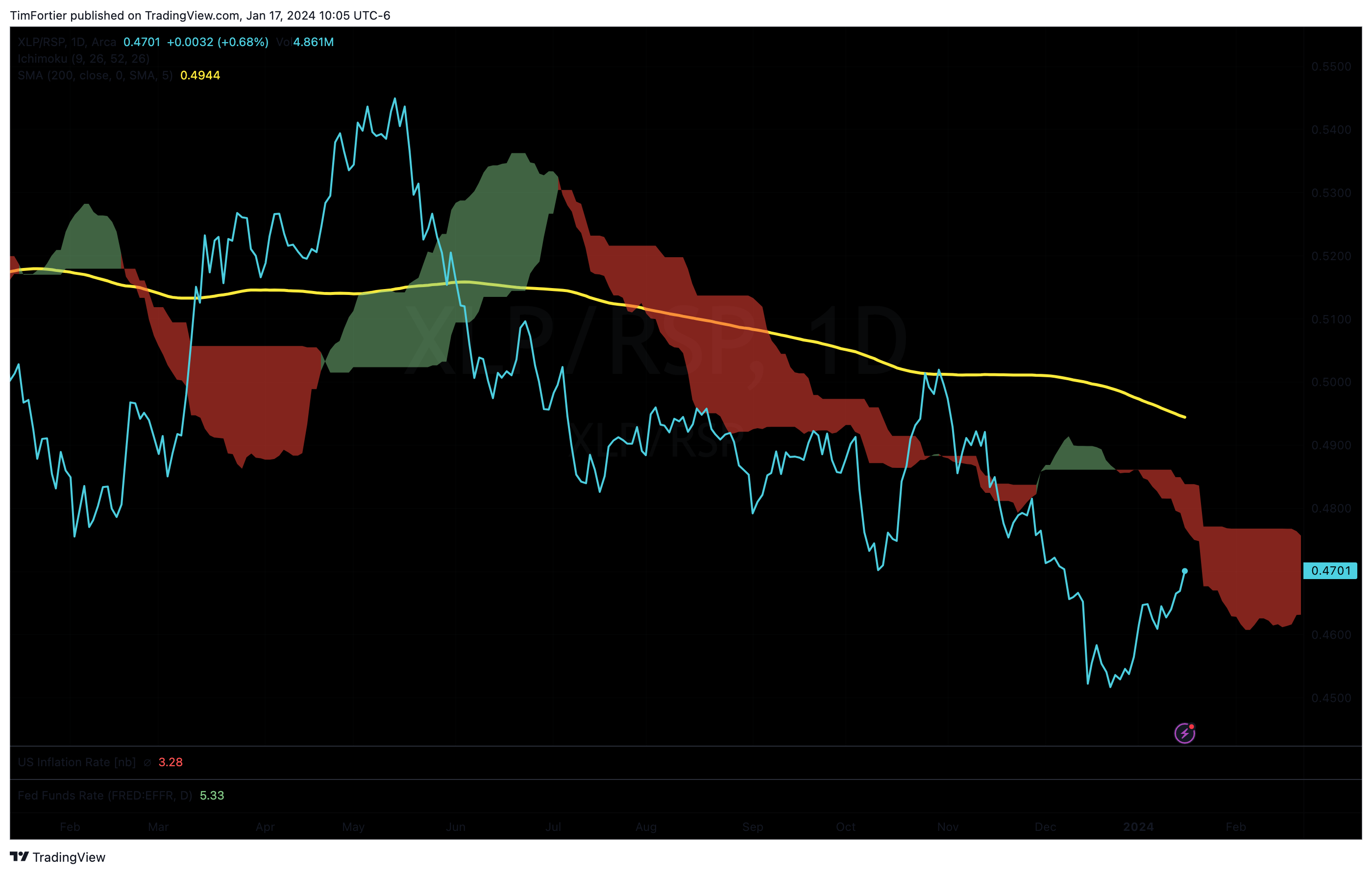

Consumer Staples

After lagging the general market for the latter half of 2023, the Consumer Staples Select SPDR Fund (XLP) remains below both its long-term moving average and the cloud. For now, this sector should be avoided.

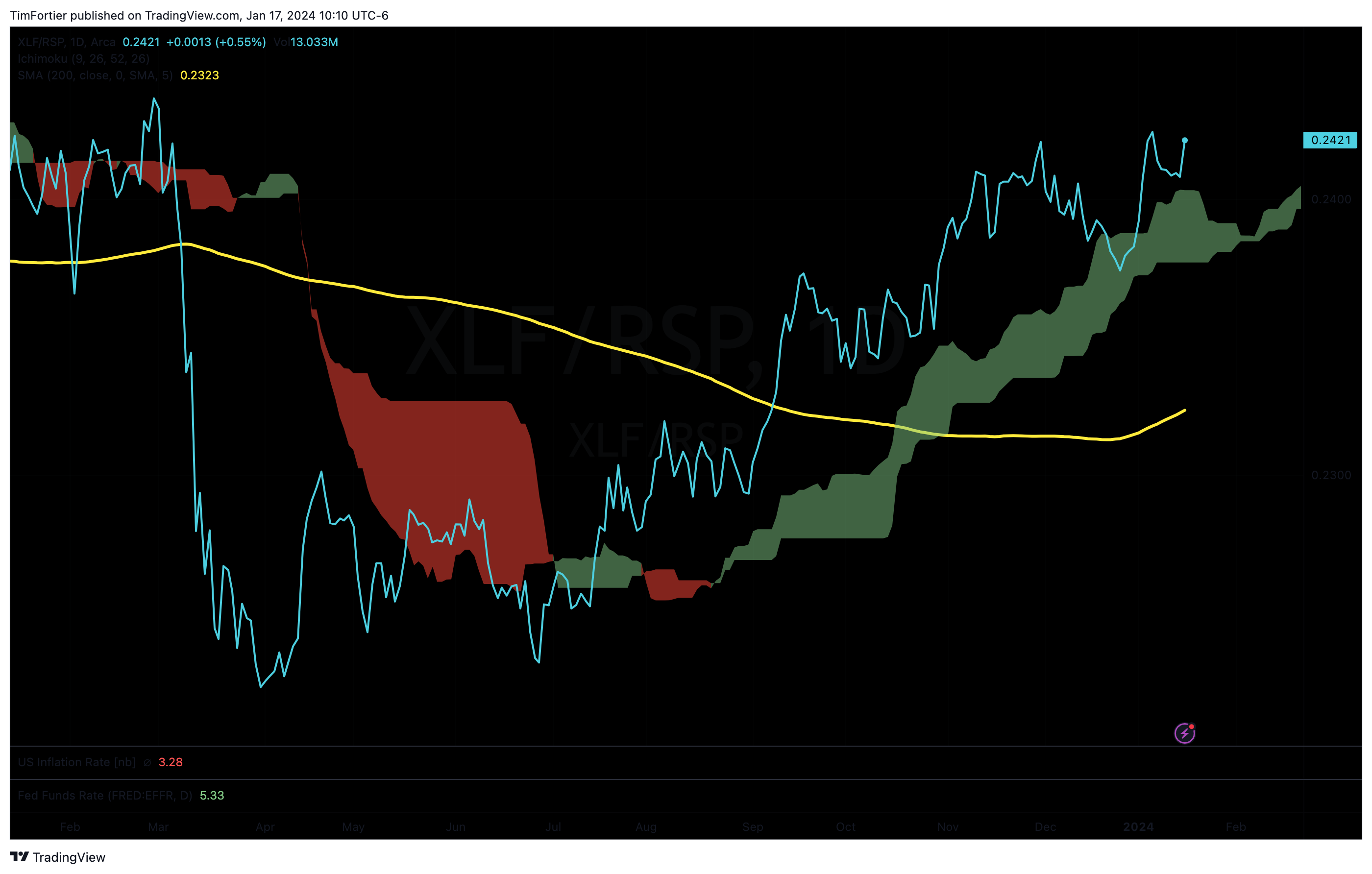

Financials

2023 was a tumultuous year for the financial sector as the year recorded five bank failures. However, the sector emerged strong and continues to look positive.

The Financial Sector SPDR Fund (XLF) is above its long-term moving averages, above the cloud, and the ratio is close to making a new trend high. Overall, this looks strong.

Utilities

The Utility Select SPDR Fund (XLU) remains weak and is in a downtrend. Avoid it for now.

Technology

After briefly dipping below the cloud, the Technology Select Sector SPDR (XLK) has rebounded above but remains below its November peak.

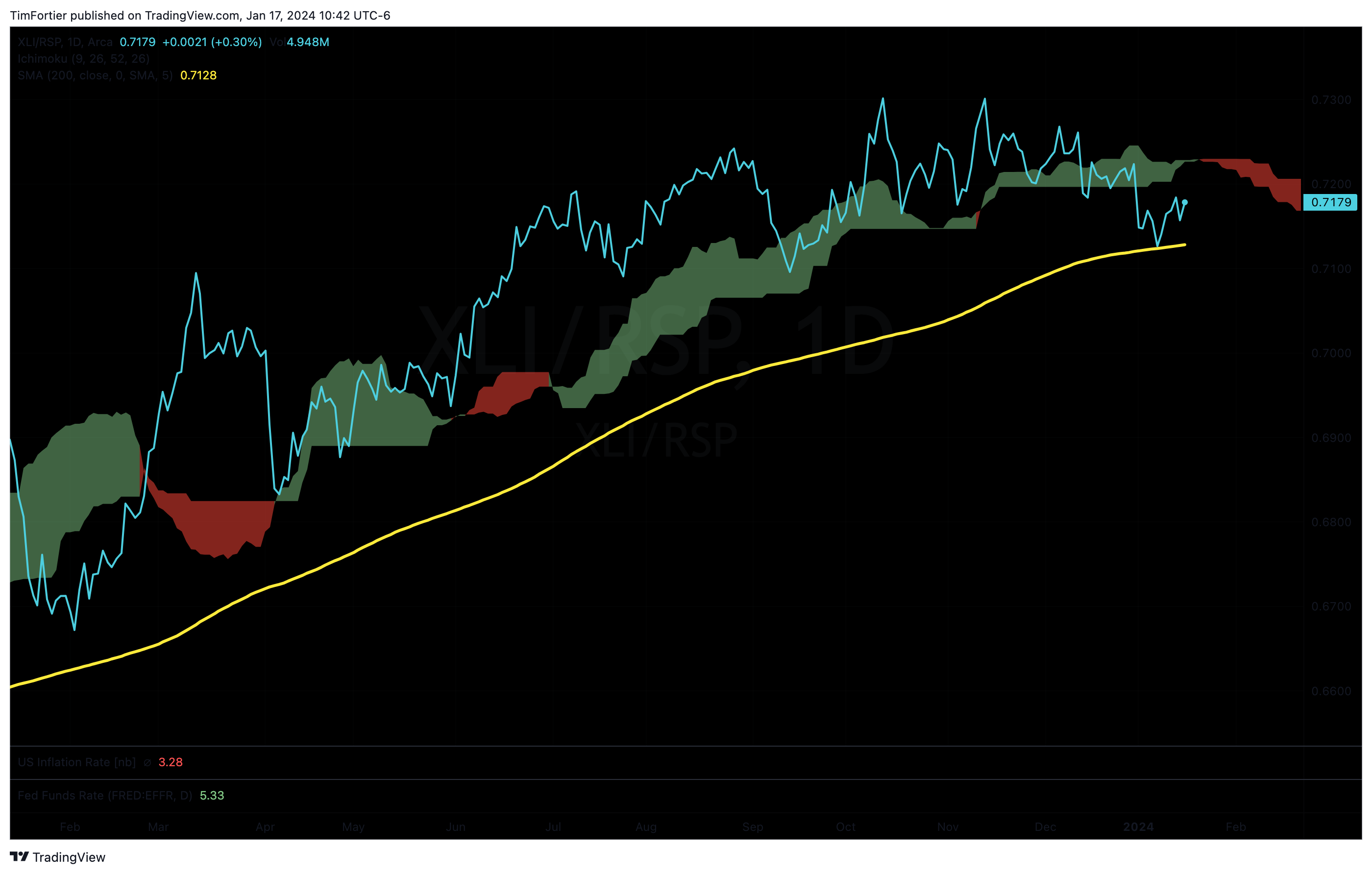

Industrials

The Industrial Select SPDR Fund (XLI) has slipped below the cloud but does remain above its long-term moving average. That said, it is also making lower lows. Avoid it for now.

Consumer Discretionary

The Consumer Discretionary Select SPDR (XLY) is close to reversing lower. After spending the last several months in a sideway range, this ratio is close to moving below its long-term moving average.

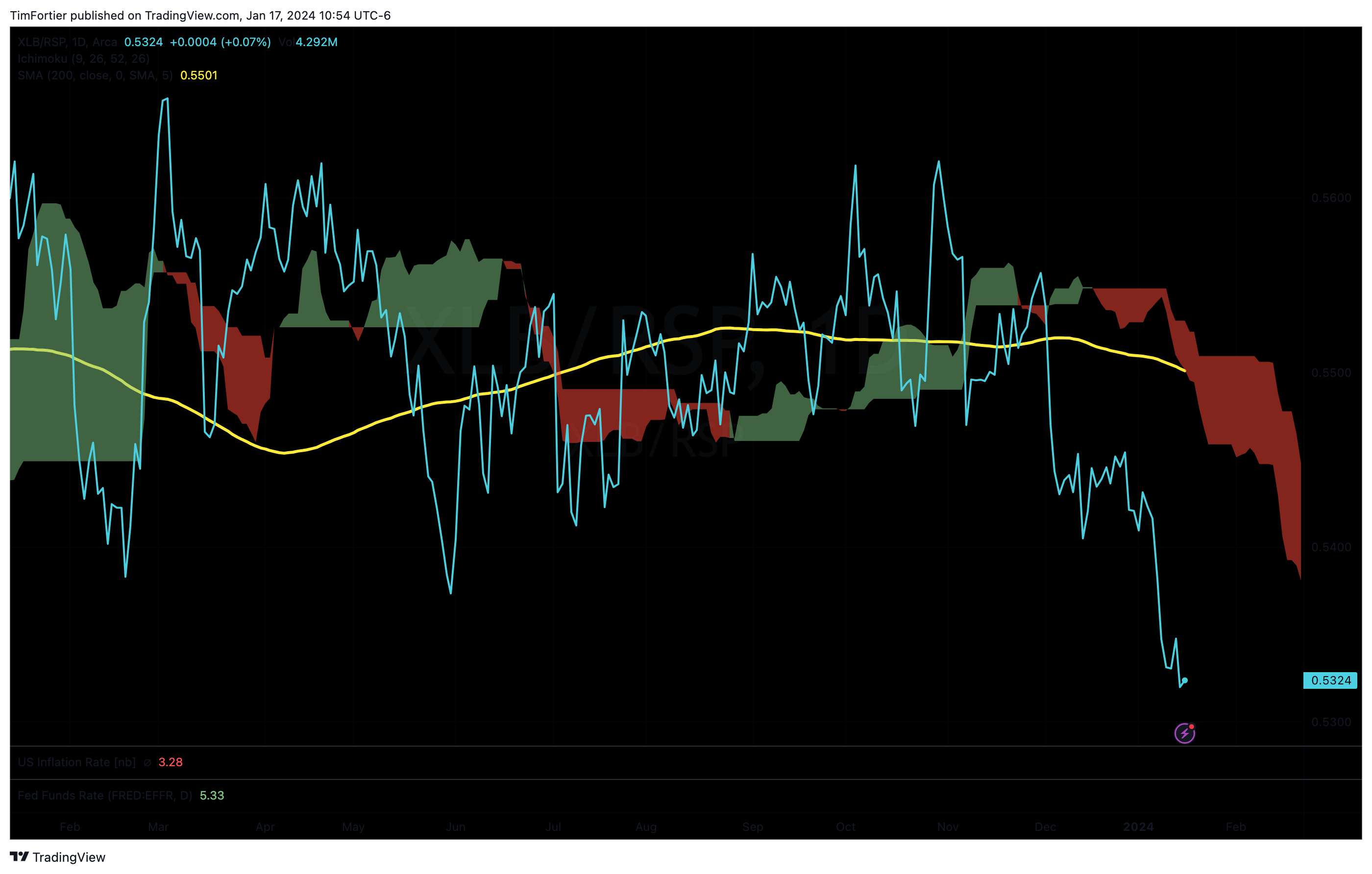

Materials

Perhaps reflecting the weakness in manufacturing, the Materials Sector Select SPDR Fund (XLB) is currently one of the weakest sectors displaying a clear downtrend. Avoid.

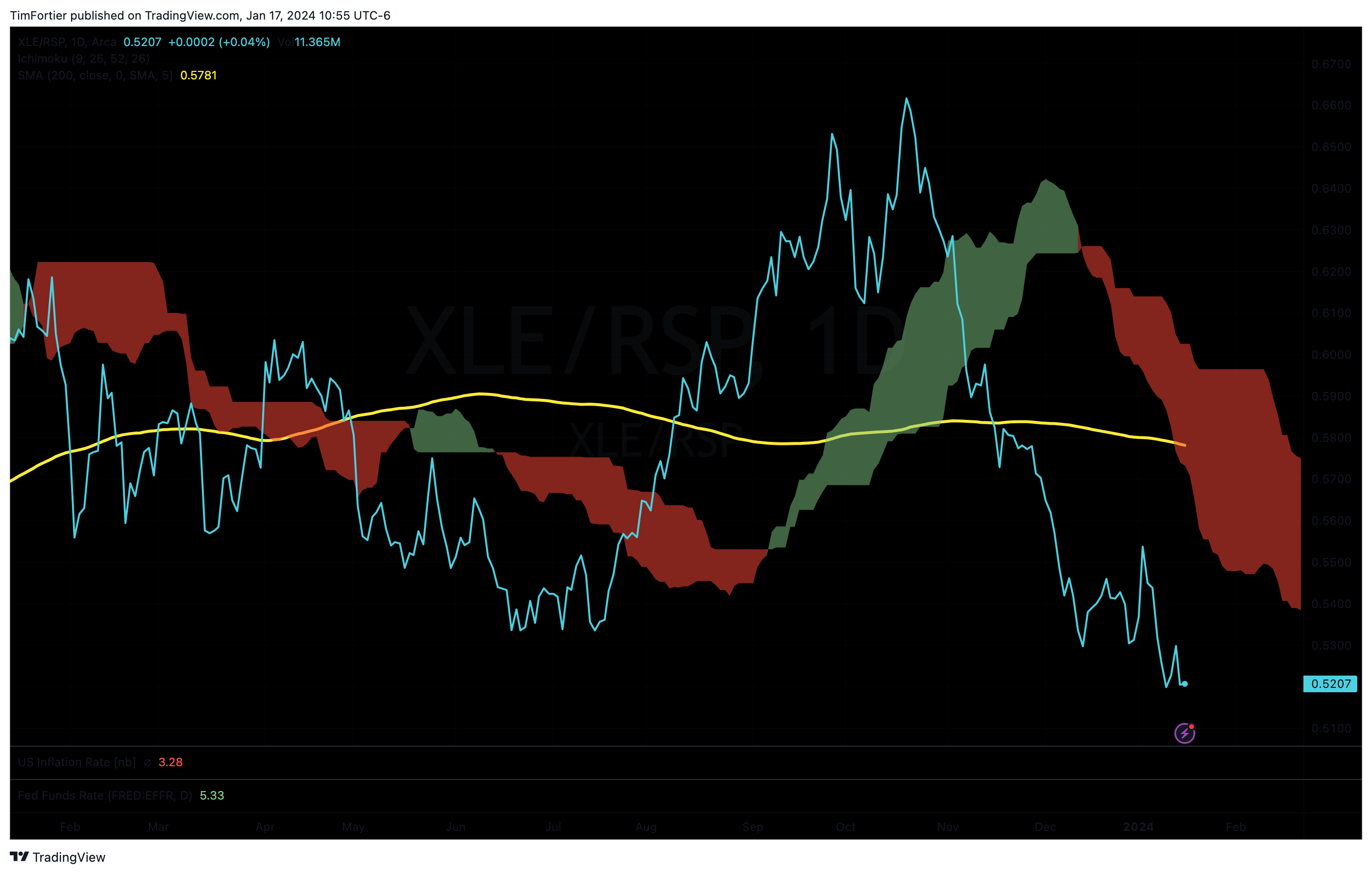

Energy

With crude oil trading just slightly above last year’s low of $67, it’s not too surprising that the energy stocks are weak. Similar to the Industrials, the Energy Select Sector SPDR (XLE) is trending lower and is among the weakest sectors.

In close, last year’s winners, including Communications and Technology, appear to be weakening. Sectors sensitive to manufacturing and the consumer are also weak. Currently, defensive sectors such as utilities and consumer staples are not leading on a relative basis.

Financials are currently the strongest sector and Healthcare is displaying signs that its more recent trend reversal high may continue longer.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.