Related Blogs

March 21, 2024 | Avalon Team

On Wednesday, as universally expected, the Fed held its base interest rate at 5.25% to 5.50%. The Fed still expects cuts this year, yet cautioned about inflation.

As I recently have written, inflation does not look like it is going away anytime soon, so it is of no surprise to me that the Fed policy officials are keeping rates pat as they are.

Here is a clip from the Fed’s press release.

“Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals are moving into better balance. The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.”

Reviewing The Fed’s Summary of Economic Projections (SEP), the Fed has upped its central tendency of GDP expectations, core inflation, and the expected Fed Funds Rate as compared to December.

This then is actually hawkish. But the market is acting as though it’s dovish.

What gives?

The market has been projecting more rate cuts during 2024 than the Fed, fueling the recent optimism around asset prices.

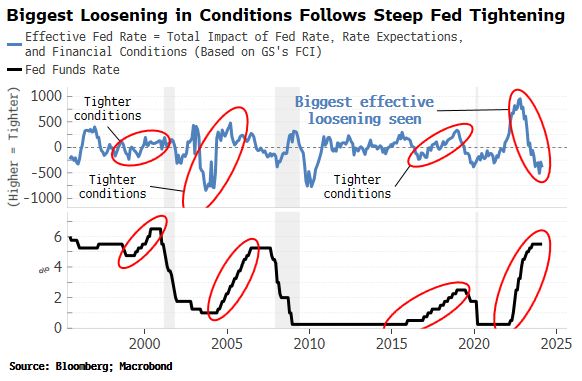

The Fed may have hiked over 500 bps, but the market’s persistent pricing of rate cuts, and markets – from stocks to bitcoin – that are going gangbusters, means net financial conditions have likely loosened, unlike in previous tightening cycles (see chart below).

That optimism comes despite stickier-than-expected inflation measures and an economy that’s held up better than most anticipated, which may lead to the Fed keeping rates higher for longer.

That said, Powell’s projections and commentary suggest that three rate cuts are still on the table for 2024.

Being “on the table” and “likely” are two different things. The cynic in me says this is Powell simply saying what the market wants to hear. Politics… nah! Can you say “election year?”

The market has become absolutely sure that the Fed can never raise rates above the true inflation rate.

But what will happen when the recent upticks in food, rents, and more recently, energy, cannot be ignored?

Food prices continue to increase. The Invesco DBA Agriculture ETF is again making new highs.

And gold is not backing off either.

The reality is that inflation expectations are actually increasing, not decreasing.

Yet, the market is pricing in a loosening of monetary policy.

Finally, we can see how the bond market is viewing this via the ratio between iShares TIPS Bond (TIP) and iShares 7-10 year Treasury Bond (IEF).

When the line is rising as it is now, the market TIPS Bonds are performing better than intermediate treasuries.

When do TIPS outperform Treasurys? Nominal Treasurys can lose real value when realized inflation exceeds inflation expectations at the time of a bond’s purchase. In such an environment, TIPS typically outperform nominal Treasurys.

So despite the stock market rally, it appears to be based on what could be a faulty assumption about the the future of inflation and interest rates.

Stay safe out there,

If you’ve been considering hiring an advisor to help guide you through the ever-changing financial landscape, take your first step today by scheduling a free consultation with one of our experienced team members. There’s no risk in exploring if we’re the right fit for your financial goals. Contact us now.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.