Related Blogs

November 21, 2023 | Avalon Team

It’s Thanksgiving, one of my favorite holidays, and with a very short week in trading, I’m going to take a departure from the usual commentary on current economic themes and the markets to focus on the behavioral side of investing.

It is well-documented that investor behavior is a common reason for poor investment performance.

Since 1984, independent investment research firm Dalbar, Inc. has published its annual Quantitative Analysis of Investor Behavior report or QAIB.

This research series studies investor performance in mutual funds.

Its goal is to shed light on how investors can improve portfolio performances by managing behaviors that cause them to act imprudently.

Over the years, one consistent theme keeps cropping up.

Namely, the set of longer-term data analyzed in these QAIB reports clearly shows that people are, more often than not, their own worst enemies when it comes to investing.

Often succumbing to emotional selling and performance chasing, many investors lack knowledge and/or the ability to exercise the necessary discipline to capture the benefits markets can provide over longer time horizons.

In short, they too frequently wind up reacting to market maturations and lowering their longer-term returns.

In the 2023 edition of the study, Dalbar reaffirms past research findings that fund investors who remained patient and didn’t focus on short-term market gyrations were significantly more successful than those who let their emotions override a longer-term strategy to build wealth.

It’s really no one’s fault, as it is simply how we are all wired… which traces back to our most primitive survival mechanisms.

Investors get overconfident when their investments perform well and become panicky and pessimistic when returns are poor.

But the good news is that this is easy to fix – it’s all about focus. Let me explain.

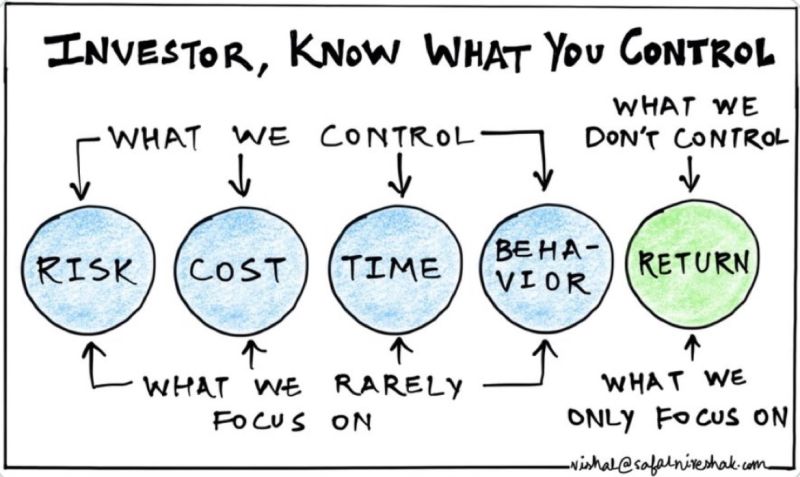

To be a successful investor, we must learn to shift our focus to what we can control versus what we don’t control.

And as the graphic below shows, most investors focus on the one thing they can’t control while paying less attention to what they do control.

Let’s change that, shall we?

What’s interesting is that the more investors focus on the things they DO control, the better their returns become.

Let’s start with what I think is THE most important one on the list – RISK.

By becoming focused on risk management, returns take care of themselves.

What gets investors into trouble is not having clearly defined exits. Investors often fail to cut losses but are quick to take profits.

This is because there is a pain in recognizing losses (loss aversion) while we gain pleasure from taking profits.

Thus, over time, investors often experience small gains with outsized losses, which mathematically creates a path to near-certain failure.

Only by keeping losses small can investors benefit from “the magic of compound growth,” in which the ending value of period “n” becomes the starting value for the period “n+1”.

An investor with large losses must make outsized (and thus less likely) gains to overcome previous losses.

And if an investor is fortunate enough to gain back their capital, what they never get back is the time wasted waiting to recover.

Losses are asymmetric because it requires a gain larger than the loss to recover back to the original value.

A portfolio losing 10% in value only requires an 11% gain to get back to even, whereas a 50% loss requires a 100% gain to recover from as this graphic shows.

It is better to keep losses small, which requires lower future returns and less time to recover.

Next on the list for where investors should focus their time and attention is “Cost.”

It is important for investors to understand all the costs associated with their investment portfolio.

The good news for investors is that the costs associated with trading are now virtually zero, and the internal costs of financial products such as ETFs are now, overall, quite low.

Where I find costs have come down little is inside of insurance products like annuities and variable contracts.

Though some low-cost products exist, they are more the exception than the norm.

By taking the time to understand and reduce investment expenses, investors can immediately increase their bottom line.

One Solution that Does it All

The good news for investors is that there is a proven approach that can reduce risk, save costs and time, help eliminate bad investor behavior, AND improve investor returns.

Systematic, rules-based investing does all of this which is why I have used this approach for over two decades.

First, rules-based investing can help eliminate harmful human behavior, as all buy and sell decisions are predetermined by a proven formula.

Also, oftentimes, the rules include active, downside risk management designed to prevent large losses from occurring.

By keeping losses small, when they do occur, it becomes much easier to recover and achieve new equity highs.

When using low-cost index funds within a rules-based framework, it is easy to keep costs low while benefiting from risk management and the expected higher returns obtained by a good, proven system.

Finally, since rules-based systems are pre-programmed, it can literally take only a few minutes each month to manage a portfolio.

One only needs to check the current output and make any minor changes that may be called for.

The time saved can be used for more important things such as family time, walking the dog, or recreation. After all, a portfolio is a means to an end but not the end itself.

So if you are an investor who is struggling for consistent returns or find yourself self-sabotaging your own success, I urge you to consider the benefits of using a rules-based approach.

Now if there were such an easy way as to not eat so much during the holidays.

Have a Happy Thanksgiving!

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.