Related Blogs

February 15, 2024 | Avalon Team

On Tuesday, a hotter-than-expected CPI report sent stocks and bonds reeling.

- All items excluding food and energy rose 0.4 percent vs an expected 0.3 percent.

- Year-over-year the CPI rose 3.1 percent vs an expected 3.0 percent.

- Year-over-year the CPI excluding food and energy rose 3.9 percent vs an expected 3.7 percent.

The one bright spot was energy, which declined 0.9%, making filling up your car a little less painful.

The recurring theme of rising rents and food prices was the primary driver of the higher-than-expected increase.

- The food and beverage index increased 2.6 percent over the last year, but food away from home was up 5.1 percent.

- Rent of primary residence was up 6.1 percent from a year ago outpacing wage increases.

The Fed watches core CPI, the CPI excluding food and beverages. What it would like to see is 2.0 percent inflation. The last three core readings were 4.0 percent, 3.9 percent, and 3.9 percent.

Progress has stalled.

This means the Fed may hold rates “higher for longer,” maybe a lot longer, than what investors were hoping for.

On the stronger-than-expected CPI data, the market has priced out rate cuts by the Fed for March and May. A full quarter-point cut for December was also priced out.

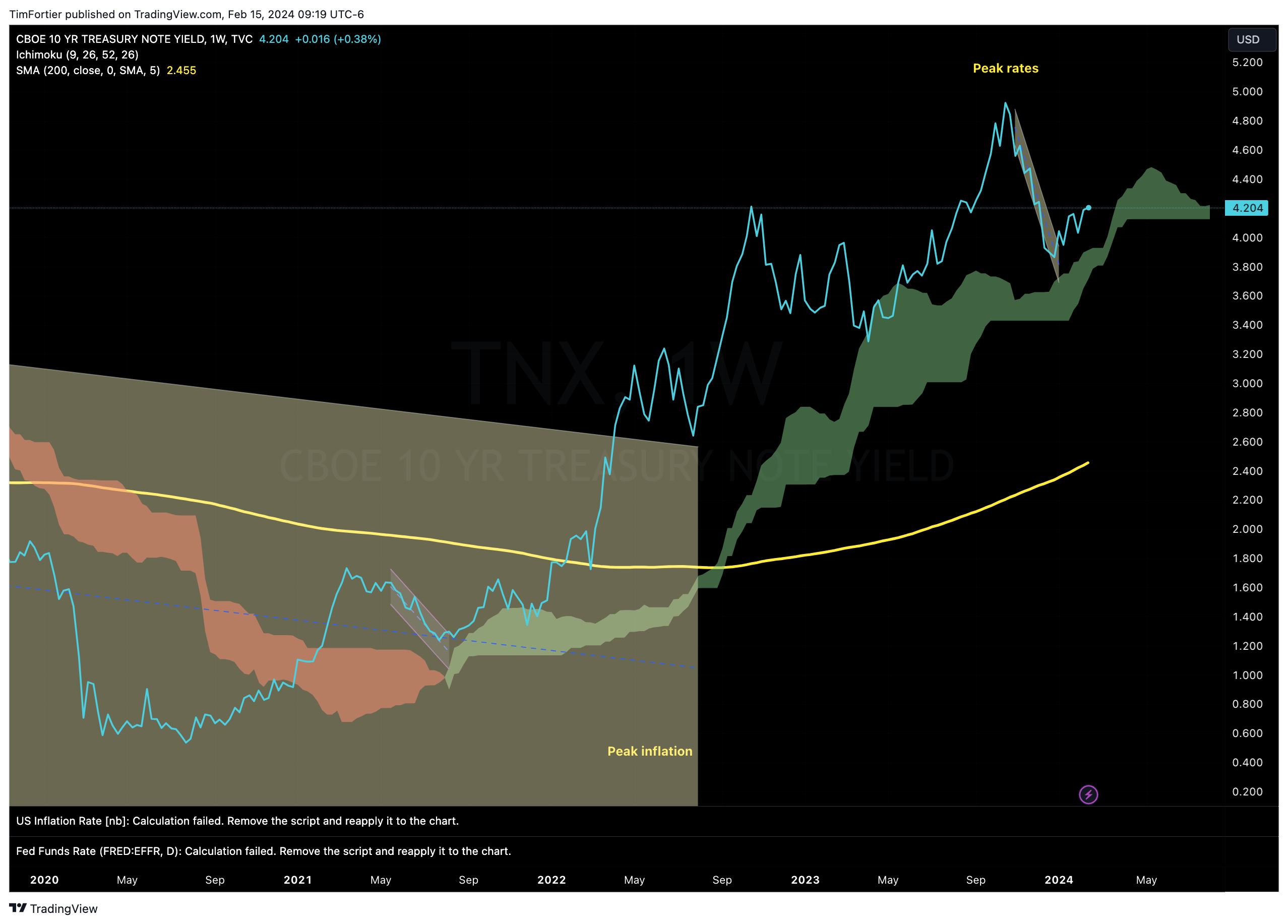

The yield on the Ten-Year U.S. Treasury Note remains in its uptrend and only a move under 3.85% would change the weekly trend from up to down.

If interest rates remain persistently higher, then it becomes all the more important that corporate earnings remain strong.

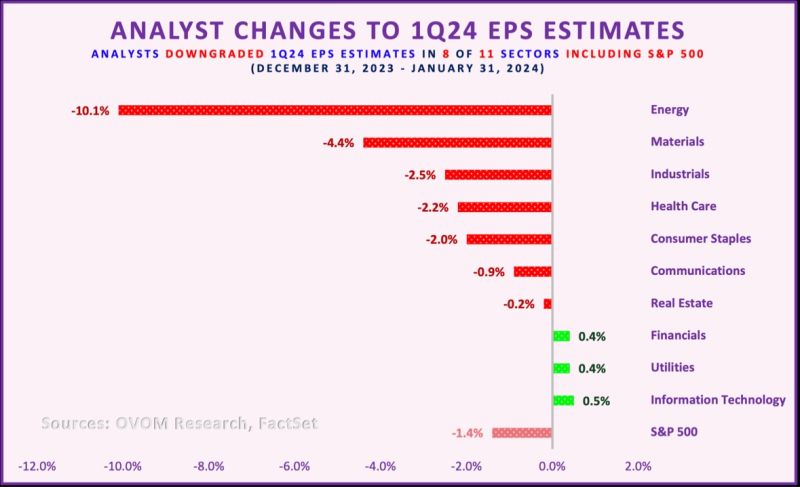

However, analysts appear to have the opposite opinion.

As the S&P 500 closed last week for the first time above 5,000 at 5,025, analysts have been busy downgrading EPS estimates for 1Q24.

The equity market is expensive today and price action seems like it’s trading as if we were in the growing stages of a business cycle.

The market is being led by semiconductors, notorious for historically having cyclical fundamentals. In secular bull markets, we typically see analysts upgrading earnings estimates more often than downgrading.

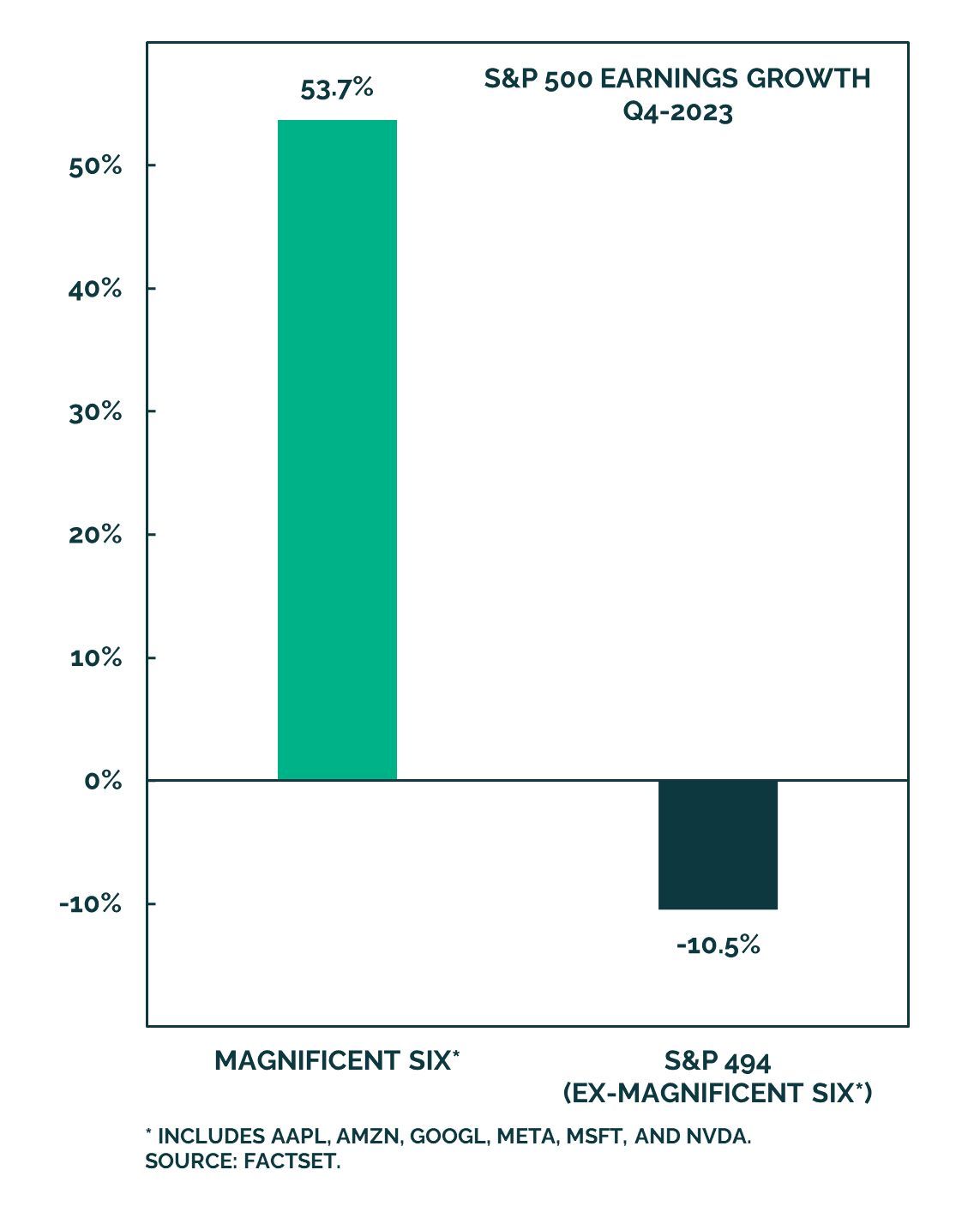

What many investors may not realize is that without the “Magnificent Six,” S&P 500 earnings growth in Q4 would be a lot lower.

According to Factset, without the “Magnificent Six,” which are projected to have grown 54%, earnings growth for the S&P 500 would have been -10%.

I suspect the equity market hasn’t been paying attention to broader earnings estimates either, as it clearly seems infatuated with high-growth tech. A pretty similar environment did not end all that well in the early 2000’s.

Underwhelming earnings growth for a large swath of the equity market explains the recent pickup in layoffs, as companies fight to defend their margins.

Internally, the market continues to weaken as the number of positive sectors continues to decline to where there are now only 17 positive sectors.

Despite this concern, the general trend of the S&P 500 remains higher… for now.

It would take a close below 4936 to change the trend from up to down on an intermediate trend basis. Meanwhile, the equal-weight S&P 500 continues to look constructive.

If you’re thinking about hiring a financial advisor to navigate the ever-changing markets, schedule a free consultation with one of our experienced team members. There’s no risk in exploring if we’re the right fit for your financial goals. Contact us today.

If you have any questions or have been considering hiring an advisor, then schedule a free consultation with one of our advisors today. There’s no risk or obligation—let's just talk.

Tags

Free Guide: How to Find the Best Advisor for You

Get our absolutely free guide that covers different types of advisory services you'll encounter, differences between RIAs and broker-dealers, questions you’ll want to ask when interviewing advisors, and data any good financial advisor should know about you and your portfolio.