Related Blogs

February 2, 2021 | Michael Reilly

February Market Review

Welcome to our February 2021 Market update.

In this month’s market recap, we review the performance of various asset classes and the driving factors behind their performance.

Economy

The markets ended lower last week, in part due to weaker than expected 4th Quarter numbers that came in slightly under expectations. Economists expected growth of 4.2%, but the actual figure of 4.0% disappointed a hopeful market.

Despite this, it remains remarkable that the economy has managed to rebound from the -34.3% decline in Q2 2020. In other economic news, unemployment claims beat expectations along with core durable goods orders, highlighting the continued progress in the economy.

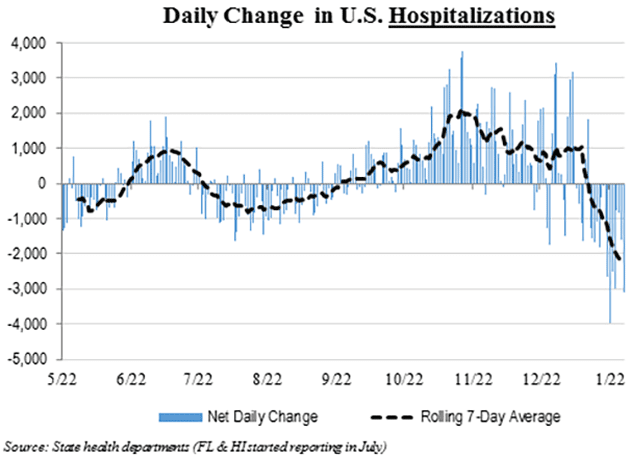

The wild card going forward is of course the pandemic. One cannot guess the forward trajectory of the economy until we see the extent of the virus this summer. The good news is that the third vaccine from Johnson and Johnson should soon be available and the Biden administration is making vaccination among its top priorities. At the same time, hospitalizations are actually beginning to decrease.

While the winter surge is reversing, the B117 and other more infectious variants could send case numbers and hospitalizations higher again, and possibly a lot higher. And even with recent improvement, the numbers are still worse than they were at last summer’s peak.

To date, globally, the vaccine rollouts have been a mess, and global economies, including the emerging economies, are at risk.

There remains a real possibility that at least the next two quarters may remain weaker than economist has originally hoped if concerns over the virus lead to further lockdowns.

The bad news is that the market has priced in a lot of “hope” and it is not likely that stocks have priced in a weaker economy going into summer. Given the amount of leverage in the stock market and low cash balances among managers, there remains a reasonable chance of a pullback before the uptrend in the stock market can resume.

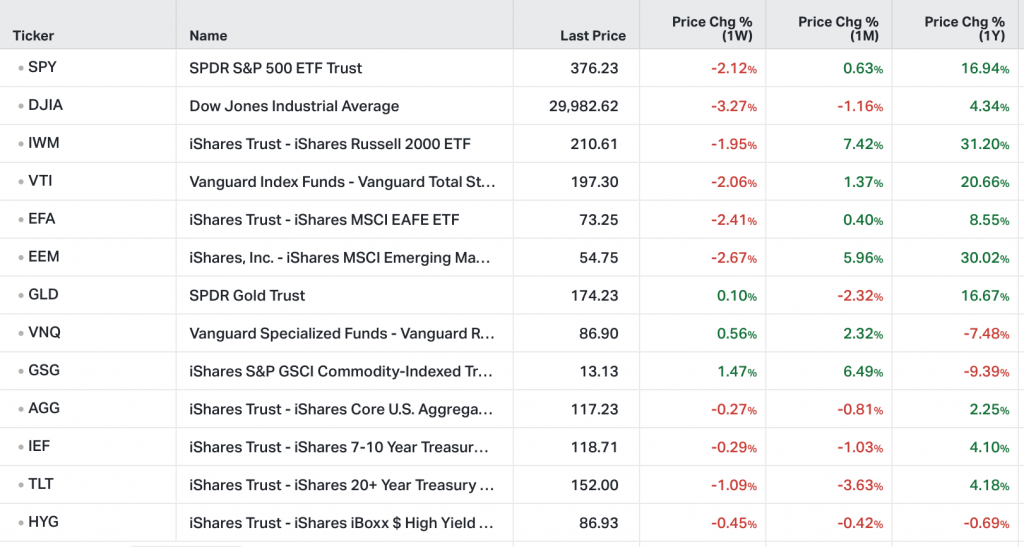

Stocks

Smallcaps and Emerging Markets dominated January’s performance. The S&P 500, finished flat as many of the FAANG stocks which dominate that index drifted sideways.

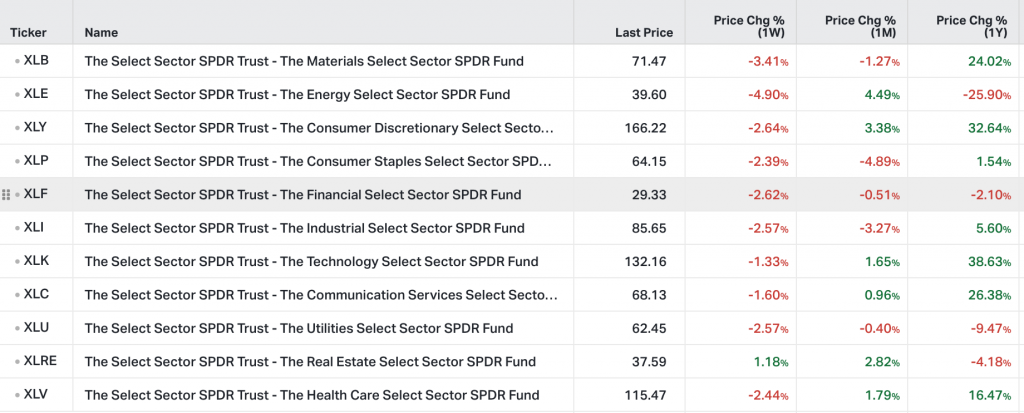

S&P sectors returned exclusively negative results last week with energy maintaining the lead so far in 2021 but remains the worst-performing sector over the past year.

Energy markets have been highly volatile, but it appears that further price support may be on the horizon given recent developments. Demand is still low, but as vaccinations proliferate, lockdown restrictions in Europe, as well as the U.S., should start to loosen, helping support recovery.

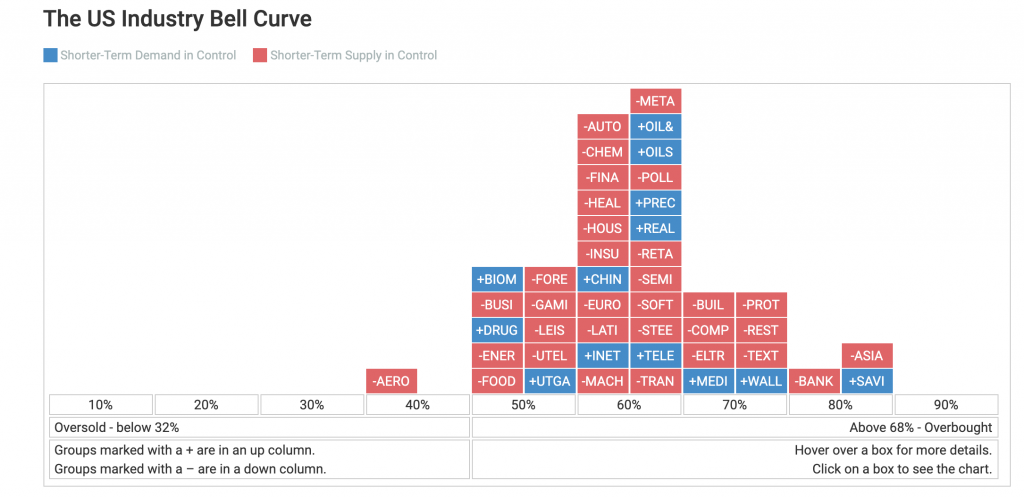

Now, when it comes to looking at the stock market, it’s important for us to look at it through the lens of our sector-centric framework.

The framework we use here at Rowe Wealth Management involves breaking the U.S. stock market into 41 sub-sectors (and 4 international groups). This is the best way to see the market clearly and generate profits.

Different sectors behave like lots of little stock markets within the general stock market and the stocks within the same sector sort of trade in unison. (I am sure you have heard the phrase “A rising tide lifts all boats”)

What we are seeing right now when we view the market through our special lens, is that most of the sectors have recently turned red. This means that more stocks are being sold in those sectors than being bought. And when you see this many sectors turn red at the same time, it generally coincides with the broader stock market at the beginning of a correction.

As you can see, most sectors are red. Just one week ago, most were blue and a week before that the vast majority were blue.

Usually what happens in a market like this is you get a sharp correction in January or February and then the market runs up through April or maybe even May.

Currently, the 5 strongest sectors (those showing the best relative performance when compared to each other) are:

- Electronics

- Textile & Apparel

- Internet

- Media

- Leisure

Commodities

One of the observations we have made is how a number of commodity-related sectors have been performing well. A recent Barron’s article points to how commodities are starting to revive after a 10-year bear market. Natural resources like energy, metals, and agriculture look set for an extended run.

Reasons to be bullish are ample. Global economies look poised to revive in the second half of 2021 as pandemic restrictions ease. And monetary conditions have rarely been so easy. The Federal Reserve may keep short interest rates near zero through 2023, while tolerating 2%-plus inflation.

Summary

Over the short term, we would not be surprised to see a correction unfold in the market. Our sector and market participation tools are showing us that there is currently some downside pressure on the market.

On Monday, tech stocks received a huge bid. It’s too early to say if that is enough to keep the market out of trouble. Over the longer term, we expect the Fed to have no choice but to keep interest rates low and will impart some form of yield control which will continue to make “risk assets” attractive.

Tags

Get Our FREE Guide

How to Find the Best Advisor for You

Learn how to choose an advisor that has your best interests in mind. You'll also be subscribed to ADAPT, Avalon’s free newsletter with updates on our strongest performing investment models and market insights from a responsible money management perspective.